Global| Jun 06 2018

Global| Jun 06 2018Volatile Spanish Industrial Output Declines in April

Summary

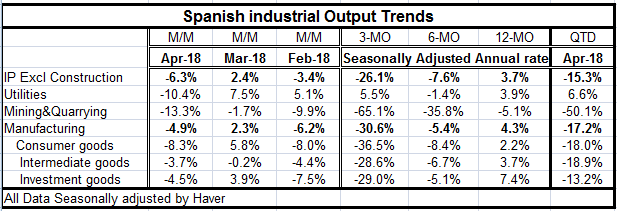

The trend for Spain’s industrial output shows ongoing increases since 2014. The headline index for industrial production, the mining sector and the index for all manufacturing show secular deterioration in their respective growth [...]

The trend for Spain’s industrial output shows ongoing increases since 2014. The headline index for industrial production, the mining sector and the index for all manufacturing show secular deterioration in their respective growth rates. But that is an unreliable signal for Spain where large monthly changes can dominate even a three month growth rate. Still, Spain shows sequential declines in growth rates of output for consumer goods intermediate goods and for investment goods. On a monthly basis there are declines in at least two and in most cases three of the three most recent three months by sector. So while volatility plays a role in Spain, weakness recently is also the result of a more protracted soft spot in the data. That explains why the monthly annualized growth rates by sector are all in the neighborhood of -30%.

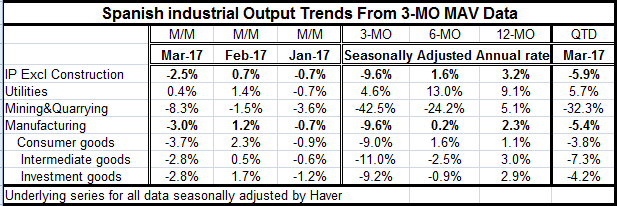

However, both Spain’s manufacturing index and the Markit manufacturing PMI index for Spain are showing deteriorating trends over 12-months. Moreover, recalculating the data in the table from three-month averages does not change the pattern of weakness nor reverse the sequential deterioration in all three industrial production manufacturing sectors. Spain appears to have an authentic manufacturing slowdown in place not just one that is the artifact of one month’s severe weakness. The growth rates are damped by the averaging of the data but the progression to weakness is still very readily apparent.

Spain is having its own political problems. Long-serving Prime Minister Mariano Rajoy has just been forced out of office. A minority Socialist government has taken control. But even this new government needs a lot of help from its friends. Spain, for the time being, is next to rudderless. The socialists are minding their Ps and Qs and promising to stay in the Great European experiment and in EMU; they are making none of the noises we had previously heard from the new Italian governing arrangement. Still, the Right no longer rules; it has been replaced by the Left and that has to put Spain at greater risk to events, come what may.

Separately ECB Executive Board Member Peter Praet today said that the EMU was making progress toward its goal of just under 2% inflation. Maybe that’s true and maybe it’s wishful thinking. But that is the message that the ECB wants to convey. With political instability spreading in Europe and with the economic expansion losing steam central bank watching takes on a new and more important dimension. For now every central bank claims to be holding the course. We’ll see how long that can last.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief