Global| Apr 28 2006

Global| Apr 28 2006US GDP Growth Back on Track in 1Q

by:Tom Moeller

|in:Economy in Brief

Summary

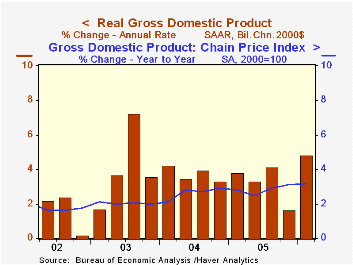

US real growth during 1Q06 rebounded smartly to 4.8% (AR) from a lull the prior quarter at 1.7%, but the two quarter average of growth at 3.2% was somewhat depressed from the 3.9% quarterly average of 2004 & 2005. The 1Q increase [...]

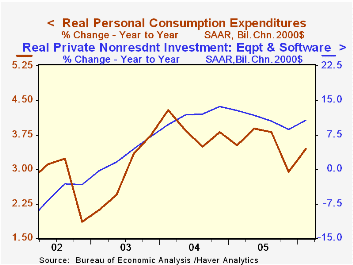

Personal consumption expenditures bounced back to a 5.5% (3.4% y/y) rate of growth from the 0.9% 4Q pause. Motor vehicles & parts consumption grew 19.8% (-4.5% y/y) but that only recovered half of the prior period's slump. Furniture & household equipment spending continued strong with a 23.3% (13.3% y/y) rate of growthand apparel spending also advanced a firm 7.8% (7.1% y/y).

Defense spending recovered all of its 4Q slump with a 10.3% (3.5% y/y) advance and that contributed 0.5% percentage points to 1Q GDP growth.

Growth in business fixed investment nearly doubled the already strong 4Q rate of growth with a 17.9% (12.1% y/y) advance. Much of the acceleration owed to a 10.8% (8.1% y/y) rise in information processing equipment & software which more than doubled the prior quarter's rate of advance. Industrial equipment, however, again was strong with a 12.2% (6.9% y/y) increase and investment in transportation equipment jumped 45.0% (15.0% y/y). That more than recouped a 4Q decline. Structures spending again was quite firm and registered 22.3% (19.5% y/y) growth.

Business Capital Spending, a speech by Federal Reserve Board Governor Donald L. Kohn yesterday to the Forecasters Club of New York, can be found here.

A wider foreign trade deficit subtracted another 0.8 percentage points from GDP growth last quarter as a 12.1% (7.5% y/y) advance in exports was outpaced by 13.0% (6.6% y/y) growth in imports.Inventories reversed a piece of the prior quarter's positive contribution to GDP growth with a 0.5% subtraction.

The GDP chain price index remained firm and grew 3.3%. Strength again owed much to the price index for the government sector which advanced 5.0% (5.2% y/y). The PCE chain price index rose a moderate 2.0% (3.0% y/y) and the price index for business equipment & software was unchanged (-0.9% y/y) following several quarters of decline.

The latest Beige Book from The Federal Reserve Board covering economic activity in the twelve Federal Reserve Districts can be found here.

| Chained 2000$, % AR | 1Q '06 | 4Q '05 | Y/Y | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|

| GDP | 4.8% | 1.7% | 3.5% | 3.5% | 4.2% | 2.7% |

| Inventory Effect | -0.5% | 1.9% | -0.3% | -0.3% | 0.3% | 0.0% |

| Final Sales | 5.4% | -0.2% | 3.8% | 3.8% | 3.9% | 2.7% |

| Foreign Trade Effect | -0.8% | -1.4% | 0.1% | -0.1% | -0.5% | -0.3% |

| Domestic Final Demand | 5.9% | 1.1% | 3.9% | 3.9% | 4.4% | 3.0% |

| Chained GDP Price Index | 3.3% | 3.5% | 3.2% | 2.8% | 2.6% | 2.0% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief