Global| Jan 27 2006

Global| Jan 27 2006US 4Q GDP Weak Due To Lower Autos & Lower Defense

by:Tom Moeller

|in:Economy in Brief

Summary

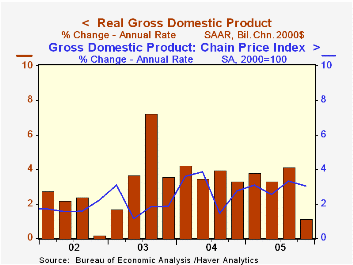

US real GDP growth last quarter weakened to the slowest in over four years. Even when the 1.1% advance is combined with 3Q, the 2.6% average gain was the weakest since early 2003 and fell short of Consensus expectations for a 2.8% [...]

Domestic demand growth suffered due to a collapse in the demand for autos. Sales incentives had pumped up 3Q vehicle & parts demand by 12.6% (AR) but the 44.9% decline last quarter pulled the demand level to its lowest since 2001. As a result, real PCE grew just 1.1% (3.0% y/y) during 4Q05.

Outside of autos, real consumer demand was firm last quarter as suggested by a 12.5% (10.6% y/y) advance in furniture & household appliances, a 10.8% (6.6% y/y) rise in apparel and a 3.2% (2.9% y/y) increase in services spending.

Business fixed investment also eased due to a shortfall in spending on transportation equipment, off 17.6% (+1.5% y/y). Investment in industrial equipment rose 10.6% (5.6% y/y) and spending on information processing equipment & software rose 9.1% (13.7% y/y).

Lower defense spending, which reversed all of the 3Q gain with a 13.1% (+0.5% y/y) decline, lowered government spending by 2.4% (+1.2% y/y). The decline in defense subtracted 0.7% percentage points from 4Q GDP growth.

Growth in residential investment eased to 3.5% (7.7% y/y), the slowest quarterly advance in a year.

The drag on GDP growth from a wider foreign trade deficit ballooned to 1.2 percentage points as imports grew 9.1% (4.6% y/y), the fastest rate of growth in a year. Exports rose 2.4% (5.7% y/y), steady with the 3Q rate of growth.Countering the drag from foreign trade, inventories contributed a large 1.5 percentage points to GDP growth, the most since early 2002.

The chain price index grew 3.0% versus a Consensus expectation for a 2.5% rise. The upside surprise during 4Q was due to a 4.9% (3.5% y/y) increase in the price index for private fixed investment which raised the price index for domestic final sales by 3.4% (3.5% y/y).

Global Economic Expansion Rolls On Into 2006 from the Federal Reserve Bank of Atlanta can be found here.

| Chained 2000$, % AR | 4Q '05 (Advance) | 3Q '05 | Y/Y | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|

| GDP | 1.1% | 4.1% | 3.1% | 3.5% | 4.2% | 2.7% |

| Inventory Effect | 1.5% | -0.4% | -0.2% | -0.3% | 0.3% | 0.0% |

| Final Sales | -0.3% | 4.6% | 3.3% | 3.8% | 3.9% | 2.7% |

| Foreign Trade Effect | -1.2% | -0.1% | 0.0% | -0.1% | -0.5% | -0.3% |

| Domestic Final Demand | 0.8% | 4.5% | 3.3% | 3.9% | 4.4% | 3.0% |

| Chained GDP Price Index | 3.0% | 3.3% | 3.0% | 2.8% | 2.6% | 2.0% |

by Tom Moeller January 27, 2006

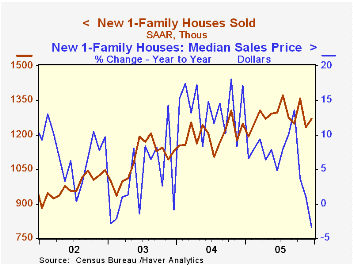

December new single-family home sales increased 2.9% to 1.269M after a 9.2% November decline that was less than initially estimated. Consensus expectations had been for a decline to 1.225M. For the year, new home sales set a new record of 1.280M, up 6.7% from 2004.

Sales gains out West, up 11.1% (12.9% y/y), and in the Midwest, up 22.7% (-8.0% y/y), offset declines in the Northeast (0.0% y/y) and in the South (4.0% y/y).

The median price of a new single family home fell 2.2% (-3.4% y/y) to $221,800. For the year, prices rose to an average $231,350 (6.2% Y/Y).

The figures from the Census Department reflect home sales counted at the time of sales contract or deposit.

| Homes Sales (000s, AR) | Dec | Nov | Y/Y | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|

| New Single-Family | 1,269 | 1,233 | 1.8% | 1,280 | 1,200 | 1,091 |

by Carol Stone January 27, 2006

Japan business and government leaders today were excited to report a second straight month of positive consumer price performance. The most widely followed CPI series is the total excluding fresh food, and it rose 0.1% year-on-year in December, following an equal move in November. The index was flat in October. So, by this gauge, the nation has not experienced deflation since early autumn. This development is already sparking talk of monetary policy changes as it perhaps signals that the long era of deflation has finally concluded. There was further encouragement from the local Tokyo area index, which moved into positive territory for January.

The upward price movements in the national index came in several sectors: housing costs, clothing, transportation and fuel. There was also less deflation in communications charges and in furniture and appliance prices. A separate "core" rate which, similar those in other countries, excludes energy as well as food, rose to +0.1% in December, its first positive reading. There is only slightly more than a year's history for this measure in Japan, however, so this move is less meaningful.

While the "increases" in the aggregate CPI series are minimal, they are the first since mid-1998, that is, more than seven years ago. The trend at that time was headed clearly downward, in the wake of the Asian currency crisis and in the face of general weakness of the Japanese economy. Now, finally, prices are firming, and this on the back of better demand. Retail sales in December, also reported today, rose 0.8% month-to-month in December, making 2005 the first year of positive growth in these sales since 1996. So perhaps there is in fact room for encouragement about the state of the Japanese economy.

| Japan CPI: Yr/Yr % Changes, NSA | Jan 2006 | Dec 2005 | Nov 2005 | Oct 2005 | December/December|||

|---|---|---|---|---|---|---|---|

| 2004 | 2003 | 2002 | |||||

| CPI Headline* | -- | +0.1 | +0.1 | 0.0 | -0.2 | 0.0 | -0.7 |

| Total CPI | -- | -0.1 | -0.8 | -0.7 | +0.2 | -0.4 | -0.3 |

| Commodities ex Fresh Food | -- | +0.2 | 0.0 | +0.1 | -0.1 | -0.3 | -1.5 |

| Fresh Food | -- | -7.5 | -16.8 | -14.2 | +9.3 | -6.6 | +9.6 |

| Services ex Imputed Rent | -- | 0.0 | 0.0 | -0.4 | -0.5 | +0.3 | +0.2 |

| Total CPI, Ku-area of Tokyo | +0.1 | -0.2 | -0.3 | -0.3 | -0.4 | -0.1 | -0.7 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief