Global| Dec 21 2006

Global| Dec 21 2006US 3Q GDP Growth Revised Lower

by:Tom Moeller

|in:Economy in Brief

Summary

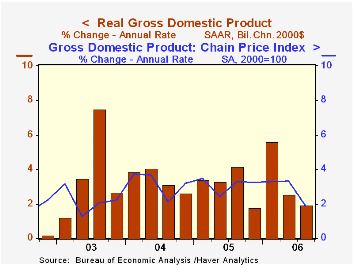

U.S. real GDP growth last quarter was revised down to 2.0% (AR). The estimate had started at 1.6% then was raised to 2.2% last month and compared to Consensus expectations for no change at 2.2%. The rise in GDP last quarter was the [...]

U.S. real GDP growth last quarter was revised down to 2.0% (AR). The estimate had started at 1.6% then was raised to 2.2% last month and compared to Consensus expectations for no change at 2.2%. The rise in GDP last quarter was the second slowest quarterly growth rate since 1Q 2003.

Expectations for growth this quarter call for further slowdown then improvement to 3.0% GDP growth next year. Economic forecasts from Macroeconomic Advisors are available in the Haver DLX database MA4CAST.

Growth in corporate profitability was revised slightly lower to still-firm 3.9% (30.6% y/y) from the 4.2% gain estimated initially. (The comparison versus last year is exaggerated by the losses suffered due to Hurricane Katrina.) The downward revision was due to a lowered figure for profits earned by US financial corporations which fell 1.9% (+60.4% y/y) and a deepened decline in profits earned by foreign entities which fell 2.2% (+5.0% y/y). U.S. nonfinancial corporate profitability was revised up slightly to 8.7% (26.4% y/y).

Less inventory accumulation contributed to the downward GDP revision for 3Q and it added 0.1 percentage points to GDP rather than the 0.2 point add estimated last month.

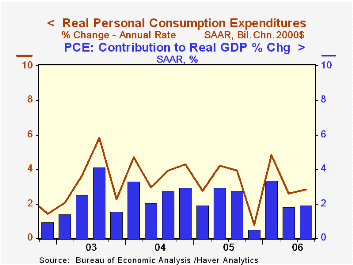

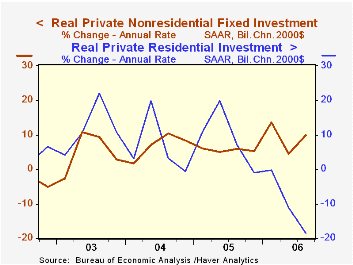

Overall growth in final sales to domestic purchasers was reduced slightly to 2.0%. Growth in personal consumption was reduced slightly to 2.8% (2.7% y/y) and nonresidential fixed investment growth was held steady at 10.0% (8.3% y/y).

Residential investment was even weaker than indicated earlier and the 3Q estimate was revised slightly down to -18.6% (AR, -8.1% y/y). It was the fourth consecutive decline, the largest since 1991 and pulled 1.2 percentage points from 3Q GDP growth. That subtraction was the largest by housing since 1981.

Deterioration in the net export deficit was left unchanged at a 0.2 percentage point subtraction from GDP growth. Export growth was upwardly revised slightly to 6.8% (9.1% y/y) and import growth also was revised up slightly to 5.6% (7.2% y/y).

The GDP chain price index was revised up slightly to 1.9%, its weakest quarterly advance in over three years. The PCE chain price index grew an unrevised 2.4% (2.8% y/y). Less food & energy the PCE chain price index grew 2.3% (2.4% y/y).

Milton Freidman on Inflation from the Federal Reserve Bank of St. Louis is available here.

| Chained 2000$, % AR | 3Q '06 (Final) | 3Q '06 (Prelim.) | 2Q '06 | Y/Y | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|---|

| GDP | 2.0% | 2.2% | 2.6% | 3.0% | 3.2% | 3.9% | 2.5% |

| Inventory Effect | 0.1% | 0.2% | 0.4% | 0.7% | -0.3% | 0.4% | 0.0% |

| Final Sales | 1.9% | 2.1% | 2.1% | 2.3% | 3.5% | 3.5% | 2.5% |

| Foreign Trade Effect | -0.2% | -0.2% | 0.4% | -0.1% | -0.1% | -0.5% | -0.3% |

| Domestic Final Demand | 2.0% | 2.1% | 1.6% | 2.4% | 3.6% | 4.0% | 2.8% |

| Chained GDP Price Index | 1.9% | 1.8% | 3.3% | 2.9% | 3.0% | 2.8% | 2.1% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief