Global| Oct 09 2015

Global| Oct 09 2015UK Trade Trends Show Deterioration

Summary

In August U.K trade data are relatively upbeat as exports rise 3.5% overall and imports fall by 0.7%. But the broader picture is still disconcerting. Over three months exports are falling at a 24% annual rate as imports advance at a [...]

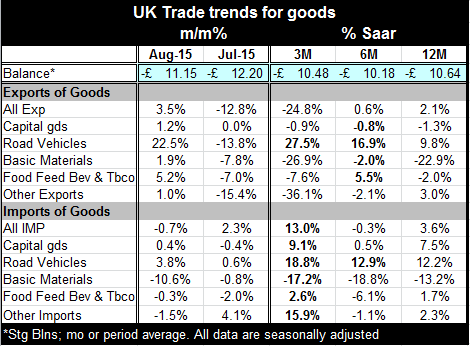

In August U.K trade data are relatively upbeat as exports rise 3.5% overall and imports fall by 0.7%. But the broader picture is still disconcerting. Over three months exports are falling at a 24% annual rate as imports advance at a 13% annual rate. Over six months exports are up by less than 1% while imports are down by less than 1%. Over 12-months exports eke out a gain of 2.1% while imports are up by 3.6%.

In August U.K trade data are relatively upbeat as exports rise 3.5% overall and imports fall by 0.7%. But the broader picture is still disconcerting. Over three months exports are falling at a 24% annual rate as imports advance at a 13% annual rate. Over six months exports are up by less than 1% while imports are down by less than 1%. Over 12-months exports eke out a gain of 2.1% while imports are up by 3.6%.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.