Global| Jul 09 2009

Global| Jul 09 2009UK Trade Picture: Better In Month But In Flux

Summary

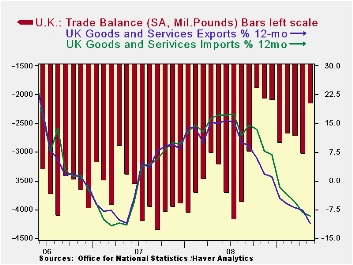

The UK trade balance shrank to 6.26bln sterling in May from 7.14bln in April. Exports edged lower, while imports fell by 4% in May. Export and import trends do not show very dramatic signs of change. Exports are declining by a bit [...]

The UK trade balance shrank to 6.26bln sterling in May from

7.14bln in April. Exports edged lower, while imports fell by 4% in May.

Export and import trends do not show very dramatic signs of change.

Exports are declining by a bit less than imports and their rate of

decline is more persistently losing that negative edge, but that

remains a very gradual process. For imports the declines over various

horizons are still large. The pace of decline over three months is less

than for six months; the drop over six months shows acceleration in the

drop compared to 12 months. Import trends are still a chaotic.

Exports and imports of road vehicles have picked up, perhaps

in response to various vehicle purchase plans in effect in the UK and

around Europe. Vehicle sales have picked up because of such incentives.

Trends for capital goods shipments are worsening for exports

and for imports over 12- 6- and 3-months.

For other groups of exports and imports the patterns are still

too varying to categorize.

German trade reported a bounce in exports with imports still

falling in May. German orders (especially foreign orders) and

industrial output have been on the mend in other recent reports. Still,

it is too soon to throw the UK figures in with that lot and call them

positive. The UK trade accounts still have divergent trends and the

improvement in trade has given way to deterioration and then to more

improvement. It is too much in flux to be sure of. Both export and

import trends are still under clear downward pressure Yr/Yr. There is

no solid sign of trade flows returning to an expansion path any time

soon for the UK.

| UK Trade trends for goods | |||||

|---|---|---|---|---|---|

| m/m% | % Saar | ||||

| May-09 | Apr-09 | 3M | 6M | 12M | |

| Balance* | - £ £6.26 | - £ £ 7.14 | - £ £6.62 | - £ £ 6.89 | - £ £ 7.34 |

| Exports | |||||

| All Exp | -0.8% | -1.5% | -12.3% | -13.7% | -14.1% |

| Capital gds | -2.8% | -8.0% | -34.3% | -28.1% | -16.1% |

| Road Vehicles | 14.5% | -8.3% | -10.6% | -39.8% | -35.0% |

| Basic Materials | -22.2% | 11.6% | -33.3% | -3.6% | -44.4% |

| Food Feed Bev & Tbco | -0.6% | 4.2% | 11.9% | 17.5% | 9.2% |

| IMPORTS | |||||

| All IMP | -4.0% | 1.5% | -16.1% | -20.1% | -15.3% |

| Capital gds | -7.5% | -0.7% | -42.6% | -37.1% | -19.9% |

| Road Vehicles | 5.5% | -5.6% | -9.4% | -22.5% | -38.4% |

| Basic Materials | -2.0% | -2.0% | -16.5% | -39.8% | -36.2% |

| Food Feed Bev & Tbco | -2.1% | 5.5% | 8.2% | 5.7% | 9.3% |

| *Stg Blns; mo or period average | |||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief