Global| May 13 2010

Global| May 13 2010UK Trade Deficit Worsens As Exports Lag Imports

Summary

The UK trade picture deteriorated in March With exports up by 1% on the month as imports screamed higher by 5.2%. This put exports in a severe shortfall position for March and ballooned the deficit. Of course in March the situation [...]

The UK trade picture deteriorated in March With exports up by 1% on the month as imports screamed higher by 5.2%. This put exports in a severe shortfall position for March and ballooned the deficit. Of course in March the situation had been completely reversed and the deficit was much smaller. Over the various intervals in the table, 3-mo, 6-mo and 12-mo, export and import growth rate pairs are very similar in each period (with both growth rates steadily rising). But imports are stronger over three months compared to exports which, in turn, are stronger over six- and twelve-months. But since the UK trade balance is in deficit to start, those periods in which exports did grow faster did not did not do much good, as the deficit widened in each of them (three months compared to six months and six months compared to twelve-months).

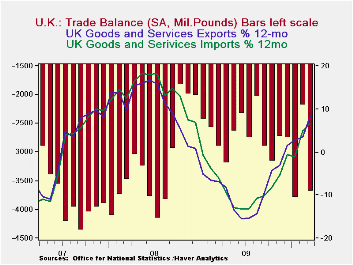

The trade balance is a tough to talk about in the recession-to-recovery periods since its impact on the economy and its meaning are conflicted. Obviously a wider trade deficit weakens GDP as the trade balance is a subtraction from GDP. But paradoxically strong imports which contribute to a widening of the deficit (all other things equal) are a sign of revived domestic demand and of STRONGER GDP growth.

So the signal from trade about the UK economy is somewhat muddled. In the chart above the trend for the deficit shows that amid some volatility the deficit is getting larger indicating that imports are outpacing exports or at least more of less tracking with them. More importantly, the growth rate for imports is steadily rising (as is the trend for exports). That suggests a revival in demand in the UK economy. So while the trade gap is widening and that is siphoning off some of the impact of this rising domestic demand, reducing its spur to domestic growth, the evidence from trade is that the UK economy is still in the improving mode as domestic demand is underpinning imports and rising strongly.

| UK Trade trends for goods | |||||

|---|---|---|---|---|---|

| m/m% | % Saar | ||||

| Mar-10 | Feb-10 | 3M | 6M | 12M | |

| Balance* | -£ 52 | -£ 6.31 | -£ 7.26 | -£ 7.14 | -£ 6.87 |

| Exports | |||||

| All Exp | 1.0% | 8.0% | 10.9% | 23.6% | 15.7% |

| Capital gds | 0.8% | 1.3% | 2.4% | 13.1% | -0.4% |

| Road Vehicles | -2.1% | 4.0% | -29.4% | 28.6% | 45.1% |

| Basic Materials | 13.1% | 46.9% | 174.7% | 84.6% | 57.9% |

| Food Feed Bev & Tbco | 0.6% | 8.0% | -0.6% | 15.6% | 10.7% |

| Other Exports | 0.9% | 8.6% | 15.6% | 23.7% | 15.2% |

| IMPORTS | |||||

| All IMP | 5.2% | -0.3% | 16.1% | 21.4% | 14.0% |

| Capital gds | 2.4% | -0.4% | 0.0% | 23.1% | 9.0% |

| Road Vehicles | 8.2% | -1.0% | 5.6% | 30.7% | 60.9% |

| Basic Materials | 10.8% | -3.2% | 73.6% | 22.8% | 24.6% |

| Food Feed Bev & Tbco | 1.8% | 1.9% | -5.0% | 8.6% | 1.7% |

| Other Imports | 5.5% | -0.3% | 22.8% | 21.7% | 11.5% |

| *Stg Blns; mo or period average | |||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief