Global| Dec 09 2009

Global| Dec 09 2009UK Trade Deficit Widens....On Rising Exports And Imports

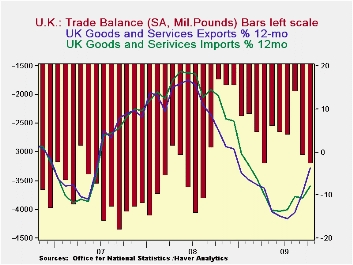

Summary

Despite faster export than import growth in October, the UK trade deficit widened in October as the larger sterling size of imports translated a smaller percentage gain in imports into a larger gain in sterling terms than for exports. [...]

Despite faster export than import growth in October, the UK trade deficit widened in October as the larger sterling size of imports translated a smaller percentage gain in imports into a larger gain in sterling terms than for exports. The UK trade position has deteriorated for two months in a row following a brief drop in the deficit three months ago.

But in terms of trends, exports and imports are on substantially the same sort of trends using growth rates over three months, six-months and 12-mponths as benchmarks (see table). Yr/Yr trends peg exports as just a bit stronger (see chart).

Various incentive programs across Europe have given a sharp prod to exports and imports of vehicles in the UK. Three-month annualized growth rates are over 120% for both exports and imports of vehicles. Rising oil prices have boosted the value of basic materials. Foods and capital goods values are rising strongly for both exports and imports.

The strength in imports bodes well for the belief that UK domestic demand is recovering. Some of the improvement is on special factors such as rising oil prices or a reaction to vehicle sales incentives. But the strength in capital goods and in foods, feeds, beverages and tobacco seems to be an authentic signal. It is present in both UK exports and in imports. This tends to affirm the notion that both the UK and its export markets are in recovery. German exports were reported stronger today as well. In the German case, import values fell. Germany’s domestic demand is a well-known sore spot of weakness in EMU. Still the German export rise is a somewhat reassuring figure after seeing weakness in German IP and in industrial orders especially for foreign orders that were tilted to weakness for EMU members.

Obviously there still are some mixed signals out there. But for now the actual export data are still hitting a positive note. We continue to recommend looking at all signals for evidence of ongoing growth. The global economy has had a nice strong lift from its weakest levels. But the run of growth needs to continue to pull the global economy into a real sustainable expansion. As of this moment the evidence is still too mixed to be reliable.

| M/M% | % Saar | |||||||

| Oct-09 | Sep-09 | 3M | 6M | 12M | ||||

| Balance* | -£ 7.11 | -£ 6.94 | -£ 6.74 | -£ 6.59 | -£ 6.86 | |||

| Exports | ||||||||

| All Exp | 4.7% | 4.4% | 36.8% | 19.7% | -3.2% | |||

| Capital gds | 6.6% | 8.0% | 48.1% | 12.8% | -7.0% | |||

| Road Vehicles | 19.5% | 2.0% | 123.6% | 164.8% | 8.0% | |||

| Basic Materials | 7.5% | 16.3% | 171.2% | 20.9% | 3.3% | |||

| Food Feed Bev & Tbco | 0.9% | 3.5% | 36.1% | 6.0% | 7.4% | |||

| IMPORTS | ||||||||

| All IMP | 4.1% | 6.4% | 37.1% | 15.0% | -3.5% | |||

| Capital gds | 4.6% | 0.5% | 26.1% | 3.0% | -5.3% | |||

| Road Vehicles | 4.0% | 16.7% | 123.0% | 129.7% | 10.4% | |||

| Basic Materials | -8.3% | 28.3% | 59.1% | 11.0% | -20.0% | |||

| Food Feed Bev & Tbco | 5.9% | 0.2% | 33.1% | -0.4% | 5.3% | |||

| *Stg Blns; mo or period average | ||||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief