Global| Apr 09 2010

Global| Apr 09 2010UK PPI Surges – Not What The Doctor Ordered

Summary

UK MFG inflation trends are still running hot with the release of the PPI for March. Commodity prices are still rising, adding to the pressure with Brent prices up by 7% in the March and other commodity prices rising as well. Coupled [...]

UK MFG inflation trends are still running hot with the release of the PPI for March. Commodity prices are still rising, adding to the pressure with Brent prices up by 7% in the March and other commodity prices rising as well. Coupled with weakness in sterling, inflation has a real foothold in the UK. The BOE has an inflation ceiling but that applies to its Consumer price measure, not the PPI. Still, with this kind of pressure on producer prices it is hard to conclude that the CPI will be out of the woods anytime soon.

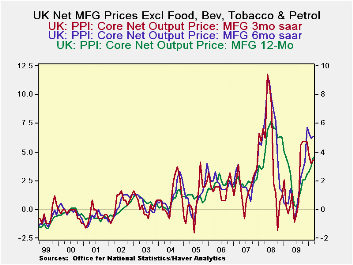

In terms trends in the PPI, The various sequential rates of growth all are elevating but the three month rate is below the six month rate for both the core and the headline rates indicating that it is not a pure acceleration for inflation But the Core rate is still slightly above its Yr/Yr pace and that is not a good sign. Inflation trends in the UK could be worse but they could be a lot better too. There is not much in this report that is reassuring if you are at the Bank of England trying to decide on policy.

On top of these poor trends there is also pressure from input prices that were up exceptionally strongly in March. While the UK has posted some better growth numbers recently the BOE is still helping the markets with securities purchases. The last thing it needs is for inflation to become more unstable. Inflation is already pushing the limits of BOE tolerance for the CPI. Any further pressure would really put the BOE between a rock and hard place.

| UK PPI MFG net output prices | |||||||

|---|---|---|---|---|---|---|---|

| %M/M | %SAAR | ||||||

| Mar-10 | Feb-10 | Jan-10 | 3-mo | 6-mo | 12-mo | 12-moY-Ago | |

| MFG | 0.6% | 0.4% | 0.2% | 4.9% | 6.7% | 5.0% | 2.0% |

| Core | 0.6% | 0.3% | 0.2% | 4.3% | 5.1% | 3.6% | 3.2% |

| Core: ex food beverages, tobacco & Petroleum | |||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief