Global| Dec 15 2014

Global| Dec 15 2014UK Overall Orders Look Solid Even As Export Orders Fade

Summary

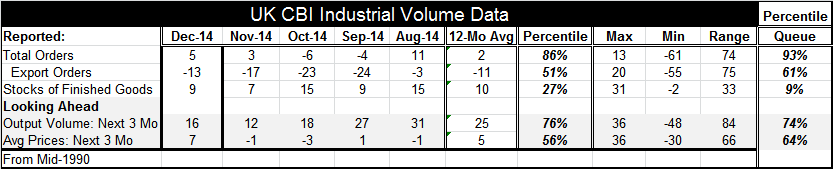

U.K. industrial orders moved up to a diffusion reading of 5 in December from 3 in November in the CBI survey of the U.K. industrial sector. While a small-seeming positive number, this reading stands in the 93rd percentile of its [...]

U.K. industrial orders moved up to a diffusion reading of 5 in December from 3 in November in the CBI survey of the U.K. industrial sector. While a small-seeming positive number, this reading stands in the 93rd percentile of its historic queue; it is higher only 7% of the time. Exports orders continue their string of improvements, increasing to a level of -13 in December from -17 in November. But the export reading is relatively modest as it only stands in the 61st percentile of its historic queue. Clearly the U.K. economy is doing well, but its export prospects are not a driving force for its economy. The difference between total orders and export orders is an indication of how weak Europe compared to the U.K. since the U.K. does the bulk of its trading with the continent.

U.K. industrial orders moved up to a diffusion reading of 5 in December from 3 in November in the CBI survey of the U.K. industrial sector. While a small-seeming positive number, this reading stands in the 93rd percentile of its historic queue; it is higher only 7% of the time. Exports orders continue their string of improvements, increasing to a level of -13 in December from -17 in November. But the export reading is relatively modest as it only stands in the 61st percentile of its historic queue. Clearly the U.K. economy is doing well, but its export prospects are not a driving force for its economy. The difference between total orders and export orders is an indication of how weak Europe compared to the U.K. since the U.K. does the bulk of its trading with the continent.

The outlook for the next three months shows a reading of 16, a step up from November. That metric has crept up, but it is still well below its September value of 27 and August vale of 31. Still, the outlook reading sits in the 74th percentile of its historic queue, a reasonably firm reading.

Output prices for the next three months jumped to a reading of 7 from -1. The 7 reading is the strongest since April 2014 but still has only the 64th percentile standing. It is interesting that the prices-expected metric has been able to rise in a period when oil and commodity prices are falling and global inflation is generally tempered or falling.

On balance, the U.K. industrial survey paints a firm picture of the U.K. industrial sector. The chart shows that the overall industrial orders reading is generally improving and stands at a relatively strong historic reading. The overall orders reading continues to push higher even in the face of considerably weaker foreign orders. And despite weak foreign orders, the outlook has perked up further as of December. One view of this is that the U.K. is surging against the tide of euro-weakness and will be forced back to a weaker growth posture by the overwhelming weakness in Europe. At the moment, that is my preferred understanding of the situation because I doubt that the U.K. has enough strength to help pull Europe up into a higher growth orbit. And because I think Europe's weakness is going to linger for some time.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief