Global| Aug 20 2014

Global| Aug 20 2014UK Orders Jump

Summary

Industrial orders in the U.K. saw the net order gauge rise to 11 in August, back to its June level. This is not just the strongest reading since June; it's a reading that has been surpassed historically only 1% of the time. The [...]

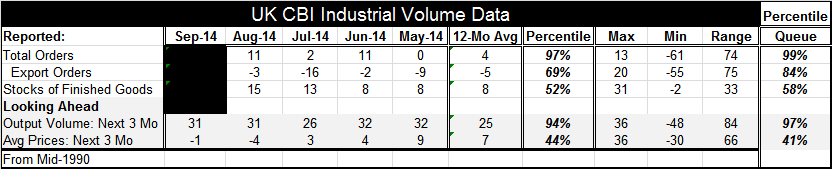

Industrial orders in the U.K. saw the net order gauge rise to 11 in August, back to its June level. This is not just the strongest reading since June; it's a reading that has been surpassed historically only 1% of the time. The highest net balance reading for orders is 13. The 11 value soars above the 12-month average of 4.

Industrial orders in the U.K. saw the net order gauge rise to 11 in August, back to its June level. This is not just the strongest reading since June; it's a reading that has been surpassed historically only 1% of the time. The highest net balance reading for orders is 13. The 11 value soars above the 12-month average of 4.

While overall orders are quite strong, export orders are not doing quite as well. The strong sterling has been an issue. The export order reading rose sharply in August to -3 from -16 in July. Still, the -3 reading stands in the 84th percentile of its historic queue and has been higher only 16% of the time. Despite its negative value, historically it is quite solid.

Looking ahead to September, output volume holds at the 31 reading posted in August. This is also a very strong reading, it has been higher historically only 3% of the time. It has continued to creep higher as its 12-month average is still solid at 25. The reading for average prices is expected to increase to -1 in September from -4 in August. That is weaker than its 12-month average value of 7. The -1 reading stands in the 41st percentile of its historic queue, leaving it well below its historic median.

Markets were rocked today by the release of the minutes from the previous Bank of England meeting. In the minutes, we find the first split decision of the committee in more than three years as two members, Ian McCafferty and Martin Weale, wanted to start to hike interest rates right away. The improving economy will be putting pressure on the BOE to act, especially with the sort of strength we are seeing in industrial orders.

The Bank of England and the U.S. Federal Reserve are in the same position of their respective monetary cycles, having been very easy for a very long time and trying to pick the right time to head back toward more normal monetary conditions. Each central bank is trying to sort out when the economy will be strong enough to make the shift. In the U.S., there is the additional agenda of trying to get more improvement out of the labor market first.

We will be hearing more about these issues later in the week as Fed Chair Janet Yellen has the keynote speech at the Jackson Hole program sponsored by the Kansas City Fed. ECB President Mario Draghi will be speaking as well. We will get a good dose of talking about the role of monetary policy when the economy just won't respond. Then there is the Fed/U.K. case of when to respond when the economy does start to grow again. The theme of the Fed conference is on the labor market dynamics, but the focus will still be on what a central bank should do.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief