Global| Jul 25 2016

Global| Jul 25 2016UK CBI Survey for Q3 Deteriorates

Summary

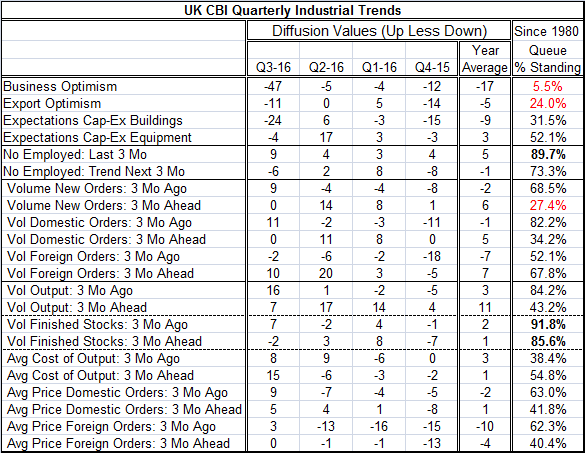

U.K. optimism fell sharply in the Q3 CBI industrial trends survey by the Confederation of British Industry. The better-minus-worse (or up-minus-down) index of expectations fell to -47, a figure that has been this low or lower only 5% [...]

U.K. optimism fell sharply in the Q3 CBI industrial trends survey by the Confederation of British Industry. The better-minus-worse (or up-minus-down) index of expectations fell to -47, a figure that has been this low or lower only 5% of the time since 1980. This is the largest one-month deterioration in the survey's history back to 1980.

U.K. optimism fell sharply in the Q3 CBI industrial trends survey by the Confederation of British Industry. The better-minus-worse (or up-minus-down) index of expectations fell to -47, a figure that has been this low or lower only 5% of the time since 1980. This is the largest one-month deterioration in the survey's history back to 1980.

Export optimism fell sharply in Q3 to a -11 net rating from zero in Q2, dropping it to a 24th percentile standing in its queue of historic values. Expectations for capital spending on buildings also fell sharply to a diffusion reading of -24 in Q3 from 6 in Q2 as British firms as well as foreign firms that were locating in the U.K. as a platform to trade within the EU now have uncertain prospects. Expectations for adding equipment fell to -4 in Q3 from 17 in Q2. Expectations for capital spending on buildings now is in the lower one-third of its historic range while expectations for equipment spending is at a mid-mark 52nd percentile.

Employment prospects were set back in Q3 but not as dramatically. The outlook for the number employed fell to a diffusion value of -6 from plus-two in Q2 but that only dropped it back to a 73rd percentile queue standing, still a pretty firm number. The level of the employment expectation index stands at a firm reading, in marked contrast to overall optimism and looks more like denial.

The volume of new orders response slipped from a 68th percentile standing over the past three months to a 27th percentile standing for the next three months as the outlook index fell from 14 to zero. Both the domestic and the foreign three-month outlook net diffusion readings fell by about 10 points from the last month's readings. Domestic orders for three-month ahead have a 34th percentile standing while foreign orders have a firmer 67th percentile standing. While the outlook for trade within the EU may have faded with the Brexit vote the pound sterling has fallen, enhancing U.K. competitiveness both there and elsewhere.

The volume output for three months ahead saw its net diffusion reading fall by 10 points to a 43rd percentile standing. The average cost of unit output saw a net increase in its diffusion value to 15 from -6 to a 54th percentile standing. That was probably related to rising global oil prices and the Brexit induced drop in the value of the pound sterling. The average prices received for orders both domestically and in foreign markets remained firm on the quarter.

In assessing potential bottleneck factors for output three months ahead, firms cited the availability of skilled labor as an issue along with credit and finance costs and materials and component availability. Factors likely to limit export orders cited finance costs but weighed much more heavily on concerns about political economic conditions, a clear signal that new relations in the wake of the Brexit vote were a worry.

On balance, U.K. firms seem very concerned about the near term. While a cheaper currency may help to ameliorate things for a short while, longer term concerns about business relationships in traditional EU markets are now a big concern. There are also a number of foreign firms that located in the U.K. to use it as a base of operations to penetrate Europe. Those operations may be at risk depending on the new trade arrangements that are agreed to. Europe will not want to treat the U.K. too badly in these negotiations since any hard line will hurt Europe too (cut off your nose to spite your face). But neither will they want to treat the U.K. too well and send the message that leaving the EU has small consequences. These two objectives will make negotiating with the U.K. a difficult market for hardline and softer-line voices in the EU. While everyone is focused on not letting this whole thing drag out and burden the region with uncertainty, too hasty a process could cripple the entire region permanently. Expecting these negotiations to be wrapped up quickly seems an unreasonable position.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.