Global| Jul 26 2006

Global| Jul 26 2006UK CBI Industrial Trends Survey Yields Mixed Picture

Summary

Yesterday, Louise Curley wrote about improving business confidence in three European nations, France, Italy and the Netherlands. In the UK the situation is somewhat ambiguous, according to the July survey of the Confederation of [...]

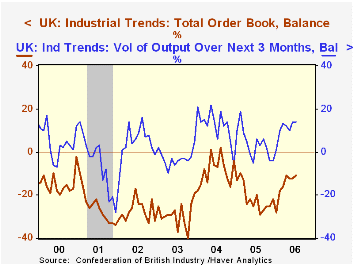

Yesterday, Louise Curley wrote about improving business confidence in three European nations, France, Italy and the Netherlands. In the UK the situation is somewhat ambiguous, according to the July survey of the Confederation of British Industries (CBI). The key monthly series, the total order book in volume terms, improved modestly, as it moved to -11 for July from -12 in June and May. At the same time these are obviously still negative, but they are all better readings than prevailed during much of 2005, which averaged -20. Export orders faltered this month. They reached 0 in May, the first non-negative reading since February 1996, but have drifted off in the two succeeding months to -6 for July. This appears to reverse the situation that had seemed to be in place in which domestic demand was fading while the export sector improved.

The CBI also published their quarterly data, which query companies' general sentiment and strategic plans. The measure on overall business sentiment deteriorated to -6 for Q3 from -2 in Q2. Even so, conditions are viewed less negatively than most of the time over the last five years. Sentiment about exports actually turned positive during last quarter and this, suggesting the downturn in orders reported above may be temporary.

Another favorable turn comes in the area of plant capacity. The proportion of companies that believe their capacity is adequate for their production plans in the coming year fell to 83%, the lowest reading since Q4 1997. In the interim, this share has run as high as 94% and that as recently as Q3 2003. When that many companies believe they have enough capacity, it's hard to anticipate there would be much capital expenditure. Now, as the adequacy ratio has fallen, the outlook for plant and equipment outlays has improved to a -9% balance in Q2 and -10% in Q3 from -23% back in 2003 when the adequacy ratio was near its recent peak. (The all-time high adequacy ratio was 99% during the 1980 recession.)

Thus, British industry managers see their outlook in fairly murky terms. Orders are improved but still falling. Export markets look stronger, but then they fade. Capital spending plans look better, but they are still declining at more companies than rising. In the Q2 GDP report last week, we saw the manufacturing sector with its first year-on-year increase since late 2004. But there are still numerous questions about demand prospects, energy prices and other uncertainties to presume this outcome will improve further or even be sustained.

| UK: % Balance | July 2006 | June 2006 | May 2006 | Year Ago | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|---|

| CBI Total Orders | -11 | -12 | -12 | -20 | -21 | -9 | -29 |

| Export Orders | -6 | -3 | 0 | -17 | -20 | -13 | -33 |

| Q3 2006 | Q2 2006 | Q1 2006 | -- | -- | -- | -- | |

| Overall Business Optimism | -6 | -2 | -14 | -16 | -19 | 7 | -17 |

| Optimism re Exports | 5 | 3 | -5 | -8 | -6 | 7 | -15 |

| Adequate Capacity | 83 | 86 | 90 | 88 | 90 | 89 | 93 |

| Plant & Machinery Expenditures next 12 months | -10 | -9 | -14 | -15 | -17 | -3 | -21 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief