Global| May 21 2013

Global| May 21 2013UK and EMU Inflation Drop

Summary

UK inflation broke sharply lower in April, falling by 0.5% after rising 0.4% in March. The twelve-month growth rate for the harmonized consumer price index in the UK is at 2.3% down from a pace of 3% one year ago. Inflation is closing [...]

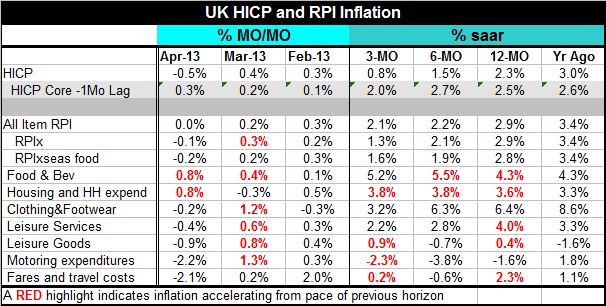

UK inflation broke sharply lower in April, falling by 0.5% after rising 0.4% in March. The twelve-month growth rate for the harmonized consumer price index in the UK is at 2.3% down from a pace of 3% one year ago. Inflation is closing in- finally- on the 2% rate that the Bank of England tries to maintain is a ceiling- A CEILING. UK inflation on this measure was last at 2% in November 2009; in October 2009 it was up by 1.6% year-over-year. Since that time inflation has gone on a wild high roller coaster ride and is only now beginning to get down within a stone's throw of the Bank of England's target. Since December 2009 the HICP has averaged inflation of 3.2%; more than one full percentage point above the ostensible top of the BOE range for a period of 41months. That has to be hard on BOE credibility. Even with an aggressive program of QE, the austerity pursued by fiscal policy kept the economy dipping into recession during this period, accompanied by the inflation overshoot.

UK inflation broke sharply lower in April, falling by 0.5% after rising 0.4% in March. The twelve-month growth rate for the harmonized consumer price index in the UK is at 2.3% down from a pace of 3% one year ago. Inflation is closing in- finally- on the 2% rate that the Bank of England tries to maintain is a ceiling- A CEILING. UK inflation on this measure was last at 2% in November 2009; in October 2009 it was up by 1.6% year-over-year. Since that time inflation has gone on a wild high roller coaster ride and is only now beginning to get down within a stone's throw of the Bank of England's target. Since December 2009 the HICP has averaged inflation of 3.2%; more than one full percentage point above the ostensible top of the BOE range for a period of 41months. That has to be hard on BOE credibility. Even with an aggressive program of QE, the austerity pursued by fiscal policy kept the economy dipping into recession during this period, accompanied by the inflation overshoot.

Core inflation that lags a month was rising by 2.5% year-over-year in March; that's about the same as it was one year ago. Core inflation over this period of the extended headline overshoot has average 2.7%.

The all-item RPI was flat on the month and it is still up by 2.9% over 12 months. Among the various RPI categories, only food and beverages, housing and housing expenses accelerated in April compared to March. Inflation not only decelerated month-to-month but the price level actually fell for the RPI as well as for the RPI excluding seasonal food. Among RPI categories clothing and footwear prices fell, leisure services prices fell, and leisure goods prices fell. The price of motoring expenditures as well as fares and travel costs also fell. The deceleration of inflation in the UK is broad-based.

While the HICP is very close to the BOE's inflation limit, in the RPI is up by 2.9% Year-over-year and the RPI x is up at the same rate. Only motoring expenses (-1.6%) and leisure goods (0.4%) show year-over-year momentum below the BOE ceiling of 2%. Among the rogue categories are clothing and footwear (6.4%), food and beverages (4.3%), Leisure services (4%), and Housing and Household expenses (3.6%).

Still, the UK seems to be making progress on the inflation front and on growth at the same time.

Compare to EMU trends through April: We can also look at these UK trends in tandem with the trends we see in the European Monetary Union. There we are focusing on the trends in the original EMU members. We see that over three months the HICP inflation measure is falling in eight of 11 countries. The exceptions are Finland with a monthly rise of 2% Belgium with the monthly gain of 1% and Portugal with a monthly gain of 0.8%: these monthly rates are annualized. In addition, inflation is decelerating in over 70% of the countries in both April and March.

Over three months the HICP is falling or is flat in five of 11 countries. The unweighted median for the group is a gain of 0.3% in its annualized 3-Mo rate. Over six-months inflation is negative in six of the 11 countries. The Netherlands has the highest annualized inflation rate at 1.8% Greece has the lowest at -2.4%. Over 12-months inflation is negative only and Greece with a 0.6% drop over 12 months. The highest inflation over 12 months is the Netherlands at 2.8% followed by Finland at 2.5% all the other countries are below the 2% ceiling that the ECB seeks in its inflation objective for the overall zone.

In addition to that inflation is decelerating over 12-months in about 91% of the countries. Over six-months it's decelerating in 100% of the countries. Over three months it's decelerating in over 45% of the countries.

Inflation simply doesn't seem to have a purchase anyplace. The challenge for the euro-Zone, for the UK and for the US is clearly shifting to growth. Despite any central bank's objectives it is becoming increasingly clear that growth is what is lacking and inflation is under control.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief