Global| Oct 08 2009

Global| Oct 08 2009U.S. Weekly Jobless InsuranceClaims Fall To Lowest Since January

by:Tom Moeller

|in:Economy in Brief

Summary

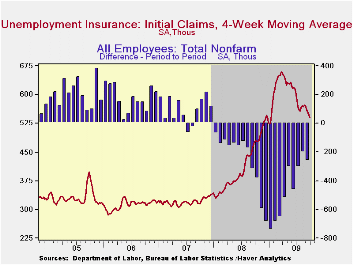

The labor market signaled improvement again. Initial claims for unemployment insurance fell last week to the lowest level since early-January. The Labor Department indicated that claims fell to 521,000 from an upwardly revised 554,000 [...]

The labor

market signaled improvement again. Initial claims for unemployment

insurance fell last week to the lowest level since early-January. The

Labor Department indicated that claims fell to 521,000 from an upwardly

revised 554,000 during the prior week. Both figures are down sharply

from the peak reached in March of 674,000 claims. The latest decline

contrasted with Consensus expectations for a smaller decline to 540,000

claims.· The largest decreases in initial claims during the week ending

September 26 were in New York (-2,253, 14.1% y/y), North Carolina

(-1,609, 26.0% y/y), South Carolina (-1,159, -7.8% y/y), Arkansas

(-818, 39.6% y/y), and Florida (-734, 37.0% y/y). while the largest

increases were in California (+4,467, 36.7% y/y), Ohio (+3,421, 30.2%

y/y), Illinois (+1,815, 51.2% y/y), Missouri (+1,049, 43.0% y/y), and

Tennessee (+1,048, 68.3% y/y).

The labor

market signaled improvement again. Initial claims for unemployment

insurance fell last week to the lowest level since early-January. The

Labor Department indicated that claims fell to 521,000 from an upwardly

revised 554,000 during the prior week. Both figures are down sharply

from the peak reached in March of 674,000 claims. The latest decline

contrasted with Consensus expectations for a smaller decline to 540,000

claims.· The largest decreases in initial claims during the week ending

September 26 were in New York (-2,253, 14.1% y/y), North Carolina

(-1,609, 26.0% y/y), South Carolina (-1,159, -7.8% y/y), Arkansas

(-818, 39.6% y/y), and Florida (-734, 37.0% y/y). while the largest

increases were in California (+4,467, 36.7% y/y), Ohio (+3,421, 30.2%

y/y), Illinois (+1,815, 51.2% y/y), Missouri (+1,049, 43.0% y/y), and

Tennessee (+1,048, 68.3% y/y).

Continuing

claims for unemployment

insurance during the latest week fell 72,000 to their lowest level

since late-March. The decline continues to owe partially to the

exhaustion of benefits. Continuing claims provide an indication of

workers' ability to find employment. The four-week average of

continuing claims fell modestly to 6,144,250. This series dates back to

1966.

Continuing

claims for unemployment

insurance during the latest week fell 72,000 to their lowest level

since late-March. The decline continues to owe partially to the

exhaustion of benefits. Continuing claims provide an indication of

workers' ability to find employment. The four-week average of

continuing claims fell modestly to 6,144,250. This series dates back to

1966.

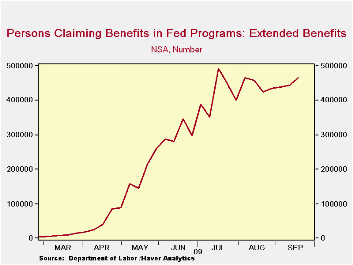

Extended benefits for unemployment insurance rose sharply for the fourth consecutive week. Through mid-September extended benefits averaged 465,295. Congress is now debating who should qualify for another benefits extension. The House passed a bill last month lengthening benefits by 13 weeks for individuals in high-unemployment states.

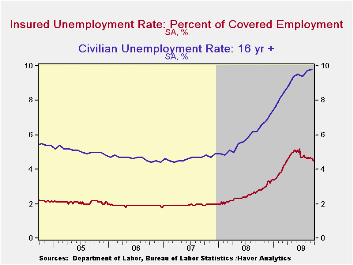

The insured rate of unemployment slipped to

4.5% and matched its lowest since early-April The rate reached a high

of 5.2% during late-June. During the last ten years, there has been a

93% correlation between the level of the insured unemployment rate and

the overall rate of unemployment published by the Bureau of Labor

Statistics.

The rate reached a high

of 5.2% during late-June. During the last ten years, there has been a

93% correlation between the level of the insured unemployment rate and

the overall rate of unemployment published by the Bureau of Labor

Statistics.

The highest insured unemployment rates in the week ending September 19 were in Puerto Rico (6.1 percent), Oregon (5.3), Nevada (5.2), Pennsylvania (5.0), California (4.9), Michigan (4.8), Wisconsin (4.7), Arkansas (4.6), North Carolina (4.6), and South Carolina (4.5). The lowest rates were in North Dakota (1.0%), South Dakota (1.1), Virginia (2.1), Wyoming (2.5), Maine (2.5), Texas (2.6), Colorado (3.0), Minnesota (3.1), Maryland (3.1), Mississippi (3.5), New York (3.5), Florida (3.9), and Georgia (3.9).· The unemployment insurance claims data is available in Haver's WEEKLY database and the state data is in the REGIONW database.

Was Monetary Policy Optimal During Past

Deflation Scares? from the Federal Reserve Bank of

Kansas City is available here.

| Unemployment Insurance (000s) | 10/02/09 | 09/26/09 | 09/19/09 | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|---|

| Initial Claims | 521 | 554 | 534 | 9.0% | 420 | 321 | 313 |

| Continuing Claims | -- | 6,040 | 6,112 | 63.2% | 3,342 | 2,552 | 2,459 |

| Insured Unemployment Rate (%) | -- | 4.5 | 4.6 | 2.8 (09/2008) | 2.5 | 1.9 | 1.9 |

by Robert Brusca October 8, 2009

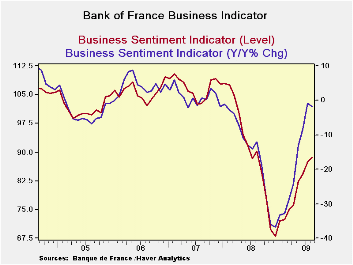

The Bank of France monthly business survey continues to show a

strong uptrend. The overall industry sentiment index (in red at the

bottom of the table) scored a reading of 92 up from 89 in August, a

standing of 30% in its range of values and above its average of 90

since October 1988. This is very good news, although the range standing

is till quite low. There is along way to go to get to ‘normal’.

The production index has been flirting with positive values in

three of the last five months so the move up to 0.59 from -0.77 is not

so special this month. That reading compares with a 12-month average of

minus 10 and a long term averages of +6. It stands in the 38th

percentile of its range.

The production outlook index is up for the second time in

three months rebounding from a reading of minus 1.36 in August to +1.23

in September. This reading, too, is better than its 12-month average of

minus 7 and below its long terms average of +6. It stands in the 30th

percentile of its range.

Demand is still quite negative and is assessed at a reading of

-32. That is above the 12-month value of -37 but below the long term

average of +1. Still it sits at a weak 16th percentile of its range.

Foreign demand (orders) is barely better standing in the in the 19th

percentile of its range.

New orders are faring better than the accumulated stock of

orders (demand). The new order index fell by 2.62 points after two

months of gains. Still the index stands in the 29th percentile of its

range.

Job losses stepped up in the current month but the survey is

on a definite improving trend. The jobs component for current hiring is

in the 59th percentile of its range. For future hiring the index is the

52 percentile of its range and that indicator improved in the month.

In short French industry is still assessed at poor levels. But

the improvement of the overall index is quite dramatic and the momentum

for continued improvement is still in place. Optimism about France is

not about being there but about getting there.

| Bank of France Monthly INDUSTRY Survey: SUMMARY | ||||||

|---|---|---|---|---|---|---|

| 12 MO | Since Oct-88 | Percentile | ||||

| Sep-09 | Aug-09 | Jul-09 | AVERAGE | Average | rank/range | |

| Production-latest mo | ||||||

| Total Industry | 0.59 | -0.77 | 0.16 | -10 | 6 | 38.0% |

| Production Outlook | ||||||

| Total Industry | 1.23 | -1.36 | 3.47 | -7 | 6 | 31.2% |

| Demand | ||||||

| Overall order books | -32.7 | -37.41 | -40.73 | -42 | 1 | 16.3% |

| Foreign Orders | 1.08 | -0.46 | -2.01 | -14 | 6 | 19.8% |

| New Orders | ||||||

| Total Industry | -2.61 | 4.35 | 2.89 | -12 | 7 | 29.0% |

| Stocks: Finished Gds | ||||||

| Total Industry | -6.21 | -8.13 | -5.44 | -5 | -2 | 19.4% |

| Capacity Utilization | 71.73 | 70.76 | 70.8 | 71 | 77 | 7.1% |

| Hiring | ||||||

| Latest Mo | -1.9 | -0.57 | -7.05 | -9 | -5 | 59.8% |

| Outlook | -7.6 | -9.98 | -8.13 | -14 | -8 | 52.2% |

| Industry Sentiment Index | 92.14 | 89.09 | 87.59 | 79 | 90 | 30.0% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief