Global| Jun 10 2009

Global| Jun 10 2009U.S. Trade Deficit Edged Higher As Revision Impact On Data Is Minor

Summary

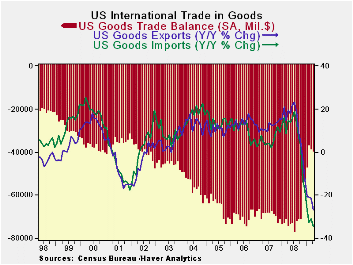

The ‘what’ of trade in April: The U.S. trade deficit widened modestly in April as exports declined and imports moved lower despite a bump up from oil imports. The U.S. deficit in international trade of goods and services increased to [...]

The ‘what’ of trade in April: The U.S. trade deficit widened

modestly in April as exports declined and imports moved lower despite a

bump up from oil imports. The U.S. deficit in international trade of

goods and services increased to $29.16 billion from a revised $28.53

billion in March. The March trade gap was originally reported as $27.58

billion. There is not much in the report that is significantly

different from market expectations this month. But the shifting in

trends is important.

Perspective: The June deficit was in line with Wall Street

expectations for a $29 billion shortfall. U.S. exports in April fell

2.3% to $121.11 billion: that is the lowest level since July 2006.

Imports decreased to their lowest level since September 2004, as they

fell 1.4% to $150.28 billion.

The Oil factor: The U.S. bill for crude oil imports in April

rose to $13.63 billion from $11.98 billion the month before as oil

prices rebounded. The average price per barrel climbed to $46.60 from

$41.36 the previous month. Crude import volumes rose to 292.60 million

barrels from 289.69 million further boosting the oil import total.

Trade, an unintended engine of growth: Trade has been one of

the most powerful buffering factors to declining US GDP. It is one of

the so-called automatic stabilizers. Imports are linked to GDP through

a high import responsive relationship (called an ‘elasticity’) that

implies that imports fall nearly twice as fast as GDP when it drops.

Since imports subtract from GDP a decline in imports boosts GDP.

Through this channel trade has buffered the GDP decline. Some of that

buffering was eaten up by exports which respond, but with less

sensitivity, to foreign GDP growth as foreign GDP and exports have

dropped too.

Trade arithmetic meets economic impact - a paradox: Trade is a

complicating factor in understanding GDP since when imports drop they

boost GDP but - at the same time - weak imports imply a weak underlying

GDP. Basically dropping imports are not a good sign for US growth even

though they will boost it. Since so many consumer goods are imported,

falling imports also are often associated with weak inventories and

when inventories drop GDP is made weaker. These relationships play out

in the GDP accounts and you can see them playing out in this cycle.

When we cut through the arithmetic of the trade account and its myriad

relationships the economic import is clear. The deficit stabilized

around $60 billion per month in the second and third quarter of last

year. By December the monthly red ink had declined to -$41.6 bil and by

Feb it reached its deficit low point at -$26.08 bil. Over the past two

months it is edging higher. That is bad news for the deficit but good

news for growth. US exports are stirring (in the sense of falling more

slowly), but imports are diminishing their rate of decline faster hence

the deficit expands. Some of that is oil. Rising oil prices remind us

of the inflation risk as the world economy reflates. The bottom line is

that trade arithmetic is often at odds with GDP fundamentals. The

incipient rise in the US deficit is good news. At some point the US

will have to find a way to blunt its appetite for imports. Putting

domestic automakers out of business is not the way to do that. The

survival and beefing up of US industry, changing consumer habits, and

finding an energy work-around will be part of the solution. And it will

be a slow process.

| US Merchandise And Services Trade | |||||

|---|---|---|---|---|---|

| Category | Current | Previous | $SA % SAAR/Average | ||

| % M/M: Current & Previous | |||||

| Apr.09 | M: $blns/% | M: $blns/% | 3-MO | 6-MO | Yr/Yr |

| Gds&Services Balance | -$29.16 | -$28.53 | -$27.92 | -$34.24 | -$47.62 |

| Goods Balance | -$40.09 | -$39.22 | -$38.84 | -$45.26 | -$59.25 |

| Exports (G&S) | -2.3% | -2.0% | -11.7% | -34.6% | -21.8% |

| Merchandise | -3.1% | -2.1% | -11.4% | -40.7% | -26.6% |

| Services | -0.5% | -1.7% | -12.3% | -19.6% | -10.3% |

| Imports (G&S) | -1.4% | 0.0% | -25.1% | -48.3% | -30.7% |

| Merchandise | -1.4% | 0.2% | -27.3% | -53.0% | -34.6% |

| Nonpetroleum Products | -2.0% | -1.2% | -30.5% | -43.9% | -28.3% |

| Petroleum & Product | 2.1% | 8.7% | -6.3% | -78.3% | -54.9% |

| Services | -1.5% | -0.9% | -15.3% | -20.5% | -9.7% |

| Technology Trade | |||||

| Tech Exports | -9.9% | 9.5% | -1.0% | -29.4% | -18.3% |

| Tech Imports | 0.1% | 14.7% | 63.5% | -38.1% | -18.3% |

| Crude Oil | |||||

| MBD (Volume):Mb/d | 9.75 | 9.35 | 9.40 | 9.49 | 9.68 |

| $/BBL | $46.60 | $41.36 | $42.39 | $47.27 | $79.25 |

| Non Petroleum trade | |||||

| Exports | -3.5% | -2.0% | -10.0% | -39.5% | -25.9% |

| Imports | -2.0% | -1.2% | -30.5% | -43.9% | -28.3% |

| Balance | -$23.93 | -$23.19 | -$23.32 | -$27.86 | -$31.75 |

| Real Exports and Imports: Non-Petroleum trade | |||||

| Real Nonoil Exports | -3.9% | 8.1% | 30.5% | -34.0% | -21.7% |

| Real Nonoil Imports | -1.7% | 2.6% | -15.4% | -38.5% | -24.8% |

| Balances are In Blns averages for period: Others % annualized except monthly | |||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.