Global| May 12 2004

Global| May 12 2004U.S. Trade Deficit Another Record in March

by:Tom Moeller

|in:Economy in Brief

Summary

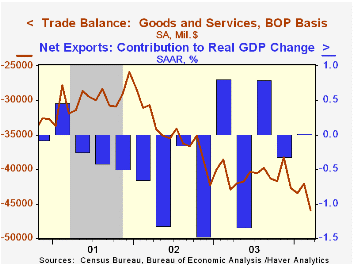

The U.S. foreign trade deficit deepened to a record $45.96B in March from the unrevised $42.12B deficit of a month earlier. Consensus expectations had been for a deficit of $43.0B. The 1Q04 average deficit of $43.8 also set a new [...]

The U.S. foreign trade deficit deepened to a record $45.96B in March from the unrevised $42.12B deficit of a month earlier. Consensus expectations had been for a deficit of $43.0B.

The 1Q04 average deficit of $43.8 also set a new record.

Total imports jumped 4.6% in March. Higher oil prices (+5.0% m/m, 1.2% y/y) and higher oil import volumes (7.8% m/m, 10.3% y/y) caused the value of petroleum imports to rise 7.8% (11.3% y/y). Imports of non-petroleum goods, however, also rose a quite strong 4.2% (11.2% y/y).

Capital goods imports recouped all of the February decline with a 3.4% (15.9% y/y) gain. Imports of non-auto consumer goods jumped 9.0% (+11.7% y/y) and auto imports gained 3.1% (9.7% y/y).

Exports rose 2.6% on top of a strong 3.9% February gain. Exports of capital goods added 1.7% (+17.5% y/y) to the 5.7% gain in February. Non-auto consumer goods exports jumped another 6.8% (18.1% y/y) and auto exports were firm (8.7% y/y).

By country, the US trade deficit with China deepened sharply m/m to $10.4B ($123.9B in 2003) but a surge in exports (11.2% m/m, 39.1% y/y) kept the deficit with China well below the November '03 record of $13.6B. The US trade deficit with Japan deepened to $6.7B ($66.0B in 2003) and the deficit with the European Union deepened to $9.3B ($94.3B in 2003).

| Foreign Trade | Mar | Feb | Y/Y | 2003 | 2002 | 2001 |

|---|---|---|---|---|---|---|

| Trade Deficit | $46.0B | $42.1B | $43.0B(3/03) | $489.9 | $418.0B | $357.8B |

| Exports - Goods & Services | 2.6% | 3.9% | 14.6% | 4.6% | -3.3% | -5.8% |

| Imports - Goods & Services | 4.6% | 1.6% | 12.0% | 8.4% | 2.0% | -5.5% |

by Tom Moeller May 12, 2004

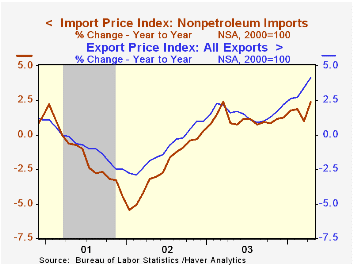

Non-petroleum import prices rose 0.3% in April, up from the 0.2% March gain. The 2.4% y/y gain in non-oil import prices is near the high of the last nine years.

Higher food prices lifted the index for non-oil import prices with a 1.2% (4.6% y/y) gain. Meat prices have been notably strong (11.8% y/y). Capital goods import prices tumbled 0.5% (-1.2% y/y) as computer & peripheral prices fell 1.3% (-5.4% y/y). Excluding computers, capital gods prices fell 0.1% (+1.2% y/y). Non-auto consumer goods prices were unchanged (0.7% y/y).

Imported petroleum prices fell 0.8% in April but in early May the price of Brent Crude Oil topped $37.00 /bbl, up more than 10% from the April average of $33.15/bbl.

Export prices again were strong with a 0.6% gain (4.1% y/y). Agricultural export prices continued strong with a 2.6% rise (23.3% y/y). Nonagricultural export prices rose a moderate 0.4% (2.4% y/y). Capital goods export prices rose 0.1% (-0.2% y/y) and non-auto consumer goods prices ticked 0.1% (0.9% y/y) higher.

| Import/Export Prices (NSA) | April | Mar | Y/Y | 2003 | 2002 | 2001 |

|---|---|---|---|---|---|---|

| Import - All Commodities | 0.2% | 0.8% | 4.6% | 2.9% | -2.5% | -3.5% |

| Petroleum | -0.8% | 5.2% | 23.7% | 21.0% | 3.0% | -17.2% |

| Non-petroleum | 0.3% | 0.2% | 2.4% | 1.1% | -2.4% | -1.5% |

| Export - All Commodities | 0.6% | 0.9% | 4.1% | 1.6% | -1.0% | -0.8% |

by Tom Moeller May 12, 2004

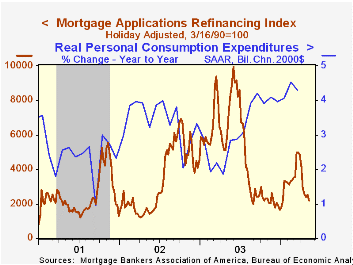

The index of mortgage applications compiled by the Mortgage Bankers Association fell 5.0% (-47.7% y/y) last week as applications to refinance tumbled 13.2% (-69.9% y/y), the sixth drop in seven weeks.

The effective interest rate on a conventional 30-Year mortgage rose to 6.61% from 6.38% the week prior. The average for April was 6.16% versus 5.65% averaged in March. The effective rate on a 15-year mortgage rose to 6.03% from 5.75% the week prior. The average for April was 5.54% versus 5.00% in March.

Purchase applications continued higher with a 2.4% w/w gain (+19.1% y/y) and began May 7.9% above the April average. Purchase applications for the month of April rose 3.3% versus March.

During the last ten years there has been a 56% correlation between the y/y change in purchase applications and the change in new plus existing home sales.

The Mortgage Bankers Association surveys between 20 to 35 of the top lenders in the U.S. housing industry to derive its refinance, purchase and market indexes. The weekly survey accounts for more than 40% of all applications processed each week by mortgage lenders. Visit the Mortgage Bankers Association site here.

| MBA Mortgage Applications (3/16/90=100) | 05/07/04 | 04/30/04 | 2003 | 2002 | 2001 |

|---|---|---|---|---|---|

| Total Market Index | 742.2 | 780.9 | 1,067.9 | 799.7 | 625.6 |

| Purchase | 494.3 | 482.5 | 395.1 | 354.7 | 304.9 |

| Refinancing | 2,184.6 | 2,516.0 | 4,981.8 | 3,388.0 | 2,491.0 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief