Global| Jun 30 2006

Global| Jun 30 2006U.S. Personal Income Firm, Prices Tame

by:Tom Moeller

|in:Economy in Brief

Summary

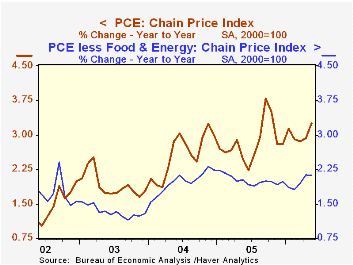

Personal income rose 0.4% last month following an upwardly revised 0.5% gain during April. The May increase doubled Consensus expectations for a 0.2% rise. The PCE chain price index rose an expected 0.4% and reflected a 4.6% (30.5% [...]

Personal income rose 0.4% last month following an upwardly revised 0.5% gain during April. The May increase doubled Consensus expectations for a 0.2% rise.

The PCE chain price index rose an expected 0.4% and reflected a 4.6% (30.5% y/y) jump in gasoline & oil prices. Less food & energy the 0.2% (2.1% y/y) rise in the chain price index also was expected. Prices for clothing & shoes fell 0.1% (-0.6% y/y) and furniture & household equipment prices continued their long standing decline (-5.0% y/y).

A strong 1.2% (7.4% y/y) gain in personal interest income and a 0.9% (11.1% y/y) increase in dividend income paced last month's rise in income.

Wage & salary disbursements were unchanged (4.8% y/y) after a downwardly revised 0.8% spike during April. Private sector wages were unchanged (5.1% y/y) as factory sector wages fell 0.1% (+2.4% y/y). Service producing industries wages also fell 0.1% (+5.4% y/y) after a 1.1% April jump.

Government transfer payments for health insurance & disability surged 1.0% (12.1% y/y) reflecting Medicare drug coverage.

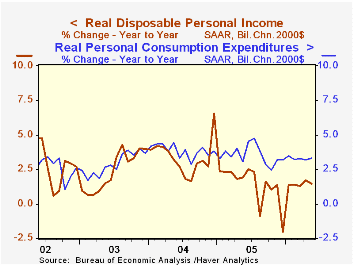

Disposable personal income rose 0.3% (4.7% y/y) after an upwardly revised 0.6% April jump. Personal taxes rose 0.5% (10.6% y/y).

Adjusted for price inflation, disposable personal income fell slightly (+1.4% y/y) marking the third m/m decline this year. A 0.1% decline in real disposable income per capita (+0.5% y/y) left the measure down 0.4% year to date.Personal consumption matched Consensus expectations for a 0.4% rise but adjusted for price inflation spending rose just 0.1% (3.3% y/y). Real spending on durables dropped 0.6% (+4.7% y/y) reflecting lower sales of motor vehicle & parts (-1.9% y/y) while real spending on furniture & household equipment rose 0.3% (12.7% y/y).

The personal savings rate was again negative.

The Trend Growth Rate of Employment: Past, Present and Future from the Federal Reserve Bank of Kansas City is available here.

| Disposition of Personal Income | May | April | Y/Y | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|

| Personal Income | 0.4% | 0.7% | 5.4% | 5.4% | 5.9% | 3.2% |

| Personal Consumption | 0.4% | 0.7% | 6.7% | 6.5% | 6.5% | 4.9% |

| Savings Rate | -1.7% | -1.6% | 0.0% (May '05) | -0.5% | 1.7% | 2.1% |

| PCE Chain Price Index | 0.4% | 0.5% | 3.3% | 2.8% | 2.6% | 1.9% |

| Less food & energy | 0.2% | 0.2% | 2.1% | 2.0% | 2.0% | 1.3% |

by Tom Moeller June 30, 2006

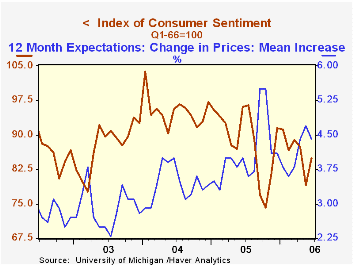

Consumer sentiment during all of June improved 7.3% from the prior month to 84.9 according to the University of Michigan. The increase recovered most of a 9.5% slump during May, built on the rise that was reported earlier and exceeded Consensus expectations for a reading of 82.5.

During the last ten years there has been a 77% correlation between the level of consumer sentiment and the y/y change in real consumer spending.

The reading of current economic conditions rose 9.3% as the index of current personal finances rose 10.8% (-7.4% y/y). Buying conditions for large household goods were judged to be 8.2% better (-7.6% y/y) than during May.

Expectations for the economy rose for just the second month this year. The 5.6% June gain reflected an 8.6% rise in business conditions expected during the next year. But long term (5 year) expectations for business conditions fell for the fourth month in the last five (-23.3% y/y). Consumers' opinion about gov't economic policy fell 3.9% m/m (-20.4% y/y).

Expected inflation during the next year slipped modestly to 4.4% and the five to ten year expected rate of inflation also fell to 3.5%.

The University of Michigan survey is not seasonally adjusted.The mid-month survey is based on telephone interviews with 250 households nationwide on personal finances and business and buying conditions. The survey is expanded to a total of 500 interviews at month end.

| University of Michigan | June (Final) | June (Prelim.) | May | Y/Y | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|---|

| Consumer Sentiment | 84.9 | 82.4 | 79.1 | -11.6% | 88.6 | 95.2 | 87.6 |

| Current Conditions | 105.0 | 103.1 | 96.1 | -7.2% | 105.9 | 105.6 | 97.2 |

| Expectations | 72.0 | 69.2 | 68.2 | -15.3% | 77.4 | 88.5 | 81.4 |

by Carol Stone June 30, 2006

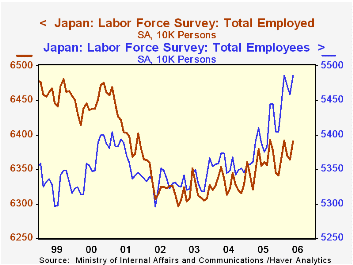

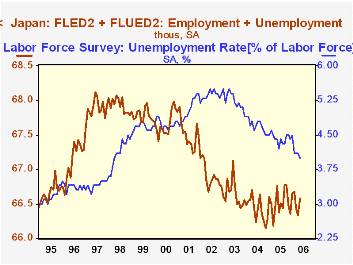

For Japan, as was the case yesterday with Germany, the last time we wrote about the labor market was three months ago. Back then, we were all excited about rising employment in Japan and falling unemployment, particularly for February. In the intervening months, however, Japanese labor conditions have hesitated somewhat, although employment has been basically stable with February's strong performance.

In May, employment gained 270,000 after a cumulative loss of 280,000 in March and April. The total amount in May, 63.91 million workers, remains above the levels of all but two months in the last 4 1/2 years. The highest was 63.93 million in September 2005, followed by February's 63.92 million. Other months, as evident from the graph and the table below, have been noticeably weaker.

The news headlines today highlighted May's low unemployment rate, 4.0%, which, as seen in the second graph, is the lowest since early 1998. However, our own enthusiasm was tempered by a look at labor force data. Japan's Ministry of Internal Affairs and Communications doesn't publish the labor force series on a seasonally adjusted basis, but we can calculate it by adding employment and unemployment. Last time we assessed these data, we were pleased to describe growth in the labor force, which meant that the decline in unemployment was coming from the strength of employment. This time, though, as we describe above, employment has been flat for three months and the second graph shows that the labor force has also stopped growing. Thus, May's dip in unemployment is not a sign of further strength, but of hesitation by workers, who likely remain skittish about the prospects for continuing growth.

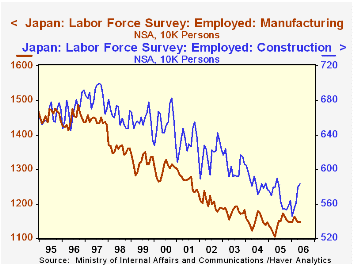

At the same time, we don't want to downplay the employment performance. Two key sectors, manufacturing and construction are looking better. The third graph indicates that these have both stabilized after declines that began in about 1997. These industry data are not seasonally adjusted either, so they're a bit erratic. But manufacturing is notable for not experiencing the jobs decline that has characterized the spring months in several recent years; instead, gains from last summer have largely held, a situation we see as impressive with the competition Japan manufacturing faces from its neighbors. Construction job gains are a good sign that investment is picking up, a quite tangible expression of confidence.

| Disposition of Personal Income | May | April | Y/Y | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|

| Personal Income | 0.4% | 0.7% | 5.4% | 5.4% | 5.9% | 3.2% |

| Personal Consumption | 0.4% | 0.7% | 6.7% | 6.5% | 6.5% | 4.9% |

| Savings Rate | -1.7% | -1.6% | 0.0% (May '05) | -0.5% | 1.7% | 2.1% |

| PCE Chain Price Index | 0.4% | 0.5% | 3.3% | 2.8% | 2.6% | 1.9% |

| Less food & energy | 0.2% | 0.2% | 2.1% | 2.0% | 2.0% | 1.3% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief