Global| Oct 30 2006

Global| Oct 30 2006U.S. Personal Income Firm, Core Price Increases Stable-to-Lower

by:Tom Moeller

|in:Economy in Brief

Summary

Personal income beat expectations last month and rose 0.5% after an upwardly revised 0.4% August increase. Despite these firm gains, the three month income rise at 5.5% (AR) is down from near 10% growth early this year. Disposable [...]

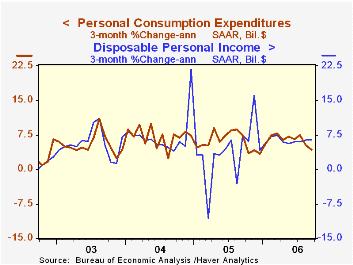

Personal income beat expectations last month and rose 0.5% after an upwardly revised 0.4% August increase. Despite these firm gains, the three month income rise at 5.5% (AR) is down from near 10% growth early this year.

Disposable personal income increased 0.5% (5.9% y/y) after an upwardly revised 0.5% August increase. In contrast to the slowdown in total income, the three month growth in take home pay has been stable at 6.4% (AR), helped by very recent weakness in personal taxes (+13.3% y/y).

Adjusted for recently lower prices, disposable personal income increased 0.8% (3.9% y/y) after two months of 0.2% gain. Real disposable income grew 3.7% (AR) last quarter after a 1.7% 2Q increase. Real disposable income per capita jumped 0.7% (3.0% y/y).

Personal consumption rose 0.1%. Expectations had been for a 0.3% increase. When adjusted for the 0.3% decline in prices, real consumer spending rose 0.4% after a 0.1% August decline. Unit vehicle sales in September recovered half of the prior month's decline with a 3.5% increase. Real PCE in 3Q grew 3.1% (AR), better than the 2.6% gain during 2Q.

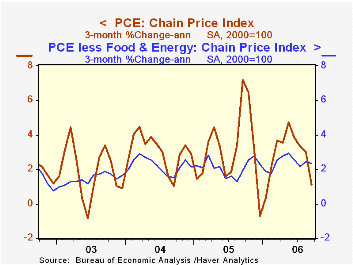

The PCE chain price index fell 0.3% due to last month's 13.4% decline in retail gasoline prices. Gasoline prices in October are down another 11.9% m/m. Less food & energy prices rose an expected 0.2% but the August gain was revised higher to 0.3%. The three month change in core prices is flat-to-lower since March at 2.3% (AR), helped by falling durable and nondurable goods prices.

Wage & salary disbursements surged 0.5% (7.6% y/y) after the meager 0.2% August increase. Wages in the private service-producing industries surged 0.8% (8.4% y/y) but factory sector wages fell 0.1% (+6.7% y/y) for the second decline in the last three months.

Interest income rose 0.1% (8.7% y/y) for the third straight month while dividend income jumped another 1.1% (11.5% y/y).

The personal savings rate was a slightly less negative -0.2% last month and so far in 2006 has averaged -0.5%, the same as last year. Should the Decline in the Personal Saving Rate Be a Cause for Concern? from the Federal Reserve Bank of Kansas City is available here.

| Disposition of Personal Income | September | August | Y/Y | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|

| Personal Income | 0.5% | 0.4% | 6.8% | 5.2% | 6.2% | 3.2% |

| Personal Consumption | 0.1% | 0.2% | 5.5% | 6.5% | 6.6% | 4.8% |

| Savings Rate | -0.2% | -0.5% | -0.5% (Sept. '05) | -0.4% | 2.0% | 2.1% |

| PCE Chain Price Index | -0.3% | 0.3% | 2.0% | 2.9% | 2.6% | 2.0% |

| Less food & energy | 0.2% | 0.3% | 2.4% | 2.1% | 2.0% | 1.4% |

by Louise Curley October 30, 2006

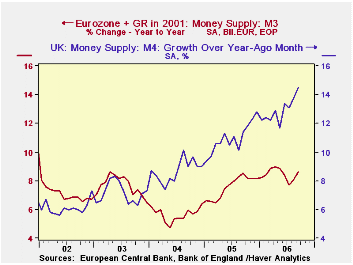

With the exception of the European Central Bank, which explicitly uses the money supply to gauge inflation, most central bankers have down played the role of money in forming monetary policy in recent years. In fact, in the United States, the Board of Governors of the Federal Reserve System discontinued publication of its money supply measure--M3-- on March 23, 2006, stating that M3 had not played a leading role in monetary policy process for many years.

There is some indication that more emphasis is beginning to be placed on the role of money in the economy by at least one central bank. In the United Kingdom, the Governor of the Bank of England (BOE), Mervyn King, recently referred to the rising money supply as a factor increasing inflationary pressures. Indeed, M4, the preferred measure of the money supply in the UK, has been rising at year- over- year levels in excess of 10% since May of 2005. The latest increase in September was 14.4%, the highest rate of increase since September, 1990. This in spite of the 25 basis point rise in the BOE's key interest rate to 4.75% on August 3rd. The year- over- year increases in the money supply in the UK and the Euro Zone are shown in the first chart.

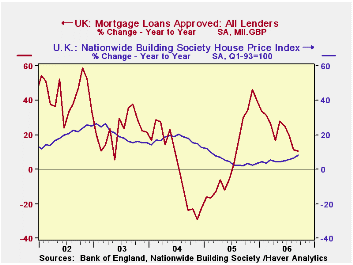

Plentiful and relatively easy money fuels investment in real assets and in the financial markets. If excessive, there is the danger of creating bubbles. Although the housing market in the UK has cooled off from the fevered activity of the last half of 2005, the August interest rate increase has failed to dampen renewed activity in the housing market as attested by the unexpected rise in mortgage approvals in September. Housing prices have also been gaining strength since early this year. In September the price of the average house was up 1.3% from August and 8.3% from September, 2005. The year- over- year changes in the value of mortgage approvals are shown in the second chart.

Should the Monetary Policy Committee of BOE announce an increase in its key interest rate when it next meets on November 9th, it is likely that the persistent rise in the money supply will have played a role in the decision.

| Sep 06 | Aug 06 | Sep 05 | M/M % | Y/Y % | 2005 % | 2004 % | 2003 % | |

|---|---|---|---|---|---|---|---|---|

| Money Supply | ||||||||

| UK M4 (Bil. Pounds) | 1,459 | 1,434.8 | 1,275.2 | 1.70 | 14.43 | 12.66 | 8.75 | 7.18 |

| Euro Zone M3 (Bil Euros) | 7,564.7 | 7,464.7 | 6,966.0 | 1.34 | 8.59 | 8.17 | 6.38 | 6.50 |

| UK Mortgage Approvals (Mil Pounds) | 30,254 | 29,457 | 27,314 | 2.70 | 10.76 | 6.17 | -1.21 | 22.78 |

| UK House Prices (Q1,1993=100) | 336.8 | 332.5 | 311.1 | 1.29 | 8.26 | 5.13 | 17.10 | 19.47 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief