Global| Dec 10 2007

Global| Dec 10 2007U.S. Pending Home Sales Ticked Higher, Again

by:Tom Moeller

|in:Economy in Brief

Summary

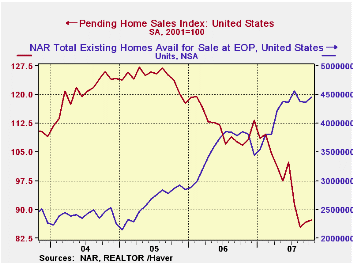

For October, the National Association of Realtors reported that the level of pending home sales ticked 0.6% higher after a modest 1.4% rise during the prior month. The level of sales still is 18.4% below October of last year and 23.0% [...]

For October, the National Association of Realtors reported that the level of pending home sales ticked 0.6% higher after a modest 1.4% rise during the prior month. The level of sales still is 18.4% below October of last year and 23.0% year to date. The last two months are the first back to back gains since early last year.

The latest monthly figure is about one third below the peak level during the Summer of 2005. The data date back only to 2001.

These figures are analogous to the new home sales data from the Commerce Dept. They measure existing home sales when the sales contract is signed, not at the time the sale is closed.

The Realtors also indicated in an earlier report that the

number of homes on the market and available for sale rose 1.9% in

October after two months of moderate decline. The rise was to a level

of 445,300 units, double the level at the low in early 2005.

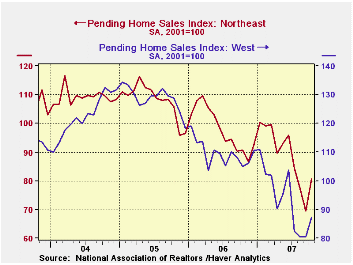

In the Northeast, pending home sales rose 6.0% m/m and recouped all of a September decline. The rise, however, followed two months a sharp drop so sales remained 20% lower than at the start of the year. Sales in the Western part of the nation also posted an 8.7% m/m rise but remained off 21% from the level early in the year.

Sales in the rest of the country were down in October. In the Midwest sales fell a slight 1.4% to remain 17% below early this year. In the South sales fell another 7.8% to a level that was 31% from the early year high.

The pending home sales data are available in Haver's PREALTOR database and the number of homes on the market are in the REALTOR database.

Housing Woes Weigh Heavily on the Economy from the Federal Reserve Bank of St. Louis can be found here.

| Pending Home Sales (2001=100) | October | September | Y/Y | 2006 | 2005 | 2004 |

|---|---|---|---|---|---|---|

| Total | 87.2 | 86.7 | -18.4% | 112.1 | 124.2 | 120.5 |

| Northeast | 80.6 | 69.5 | -11.1 | 98.0 | 108.0 | 109.2 |

| Midwest | 85.5 | 86.7 | -11.7 | 102.0 | 116.4 | 118.0 |

| South | 91.6 | 99.3 | -25.3 | 127.4 | 134.8 | 126.6 |

| West | 87.3 | 80.5 | -16.9 | 109.6 | 128.7 | 122.7 |

by Robert Brusca December 10, 2007

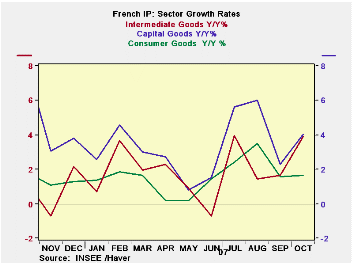

Industrial production in France was up strongly in October

showing a rise of 2.1%. In the past three months overall output is up

but without any real strong sector leadership. Auto sales are up

strongly in October. In the quarter to date output is up strongly over

its Q3 level expanding at an 8.1% annual rate. France follows the same

trend as Germany as its consumer goods output is lagging, falling by

2.1% so far in Q3. Capital goods output is up at a 6.9% annual rate in

Q4. Europe continues to show weak consumer demand/output and displays

an ongoing strong capital goods sector.

| French IP excluding Construction | ||||||

|---|---|---|---|---|---|---|

| Saar exept m/m | Oct-07 | Sep-07 | Aug-07 | 3-mo | 6-mo | 12-mo |

| IP total | 2.1% | -1.2% | 0.1% | 3.9% | 5.7% | 4.0% |

| Consumer goods | 0.4% | -1.5% | 0.9% | -1.1% | 3.3% | 1.6% |

| Capital goods | 1.0% | -1.0% | -0.1% | -0.3% | 7.0% | 4.0% |

| Intermediate goods | 1.9% | -0.9% | -0.6% | 1.6% | 3.5% | 3.9% |

| Memo | ||||||

| Auto | 6.9% | -4.0% | 1.3% | 16.5% | 6.9% | 5.7% |

by Robert Brusca December 10, 2007

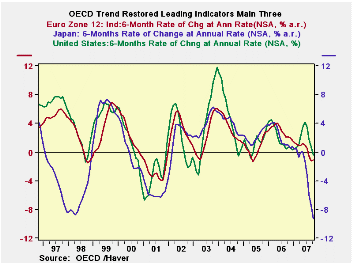

The MAIN OECD LEIs (leading economic Indicators, trend

adjusted) are dropping at a faster pace over the recent three months.

Japan’s drop is the sharpest. The OECD itself pushes emphasis on the

6-month changes in these indexes. On that basis the OECD, the OECD main

seven OECD Europe, Japan and the US all are declining. The US move is

the least negative. Japan’s is the most. Europe's slide is a bit less

than for the OECD overall.

Still the message from these OECD LEIs is very clear. The area

is slowing. The OECD itself flags Japan as a worrisome case and talks

of moderate slowing elsewhere. Clearly financial markets and central

bank events can have an influence on events in these various countries

and regions. The outlook remains in flux since these indicators have

worsened since last month.

| OECD Leading Indicators by Main regions/countries | ||||||

|---|---|---|---|---|---|---|

| Oct-07 | Sep-07 | Aug-07 | 3-Mo | 6-Mo | 12-Mo | |

| OECD | -0.3% | -0.4% | -0.7% | -5.1% | -2.0% | -0.1% |

| OECD Big 7 | -0.5% | -0.5% | -0.8% | -7.0% | -2.9% | -1.5% |

| OECD Europe | 0.0% | -0.3% | -0.5% | -3.1% | -1.5% | -0.8% |

| OECD Japan | -1.4% | -1.2% | -1.6% | -15.7% | -11.5% | -11.7% |

| OECD US | -0.5% | -0.4% | -0.7% | -6.0% | -0.7% | 1.6% |

by Robert Brusca December 10, 2007

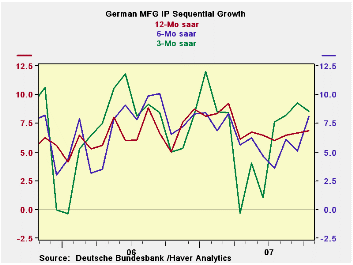

German IP edged lower in October in the face of a spurt in

orders for the month that was dominated by bulk orders. Still with the

-0.3% October result German IP is entering the new quarter on an up

note. Q/Q calculations are concerned with comparing the average level

of IP in the current quarter to the average level in the previous

quarter. The spurt for IP in August and small the rise in September

still leave the level of IP in October, after its fall, above the Q3

average. IP is growing at annual rate of 2.6% entering Q4. Consumer

goods output is much weaker, up at just a 0.4% pace in Q4. As has been

the case capital goods output is up a strong 14.3% at an annual rate.

Intermediate output is off at a 2.2% pace. Ex construction, IP is

rising at nearly a nine percent annual rate.

So Germany continues to be a bit of a conundrum. The trends in

the chart show that no direction is really dominant. The sectors are

moving in different directions, too. We know the strong euro is

creating problems; we are unsure how many. Germany remain a bit of an

enigma.

| Total German IP | ||||||

|---|---|---|---|---|---|---|

| Saar exept m/m | Oct-07 | Sep-07 | Aug-07 | 3-mo | 6-mo | 12-mo |

| IP total | -0.3% | 0.1% | 1.9% | 7.1% | 7.5% | 5.9% |

| Consumer goods | -1.3% | 0.1% | 4.2% | 12.0% | 0.4% | 3.0% |

| Capital goods | 2.1% | -0.5% | 1.6% | 13.4% | 13.4% | 10.4% |

| Intermediary goods | -1.0% | 0.2% | 1.5% | 2.9% | 6.9% | 5.6% |

| Memo | ||||||

| Construction | 0.2% | 0.7% | 2.0% | 12.6% | 4.3% | -0.8% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief