Global| Feb 01 2010

Global| Feb 01 2010U.S. Pending Home Sales Improve

by:Tom Moeller

|in:Economy in Brief

Summary

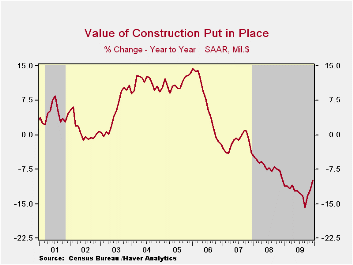

Construction activity moved lower, again. During December construction outlays fell 1.2% after a 1.2% November shortfall that was double the initial estimate. The latest decline was double the Consensus estimate. The worst of the [...]

Construction

activity moved lower, again. During December construction outlays fell

1.2% after a 1.2% November shortfall that was double the initial

estimate. The latest decline was double the Consensus estimate. The

worst of the news, however, was that for the full year the 12.2%

shortfall in activity was nearly double the 2008 rate of decline and

the third consecutive yearly drop.

Construction

activity moved lower, again. During December construction outlays fell

1.2% after a 1.2% November shortfall that was double the initial

estimate. The latest decline was double the Consensus estimate. The

worst of the news, however, was that for the full year the 12.2%

shortfall in activity was nearly double the 2008 rate of decline and

the third consecutive yearly drop.

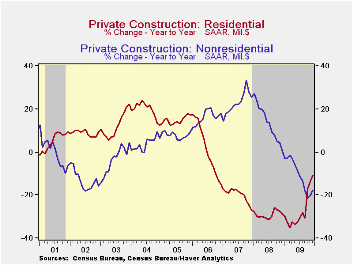

The December decline in residential building activity matched its November rate and pulled spending down again by nearly one-third y/y. Moreover, the latest level was nearly two-thirds below the 2006 high. Single-family construction activity has shown positive growth for the last seven months; however, the monthly gains have been steadily receding and overall activity was down one-half for the year. That was fourth consecutive year of lower residential building activity and it's off three-quarters from the 2006 peak. Multi-family construction activity fell nearly one-third for the year and it is off nearly two-thirds from the 2007 peak. The source of relative strength came from residential improvements which fell just 2.2% for 2009 and was off just one-quarter from the 2007 peak.

Nonresidential building activity fell another 1.8% during December and was off 11.2% for the year. Since the 2008 peak, activity has fallen by 26.9%. Spending in the food & beverage industry fell by one-third for the year. Expenditures in the lodging industry were off a similar amount. Commercial building overall fell by two-thirds y/y while office building dropped similarly. Relatively moderate were the declines in the education (-9.8% y/y), religious (-10.6% y/y) and health care (-5.1% y/y) sectors.

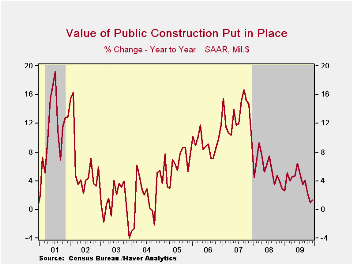

In the public sector, construction rose 3.7% for the year, despite lower tax revenues. Building activity on highways & streets rose 3.3% for the year as the focus on infrastructure rebuilding grew. Public spending on health care facilities increased a strong 14.7% y/y but building in the education sector rose just 1.5% for the full year.

The construction put-in-place figures are available in Haver's USECON database.

| Construction (%) | December | November | October | Y/Y | 2009 | 2008 | 2007 |

|---|---|---|---|---|---|---|---|

| Total | -1.2 | -1.2 | 1.5 | -9.9 | -12.2 | -6.9 | -1.6 |

| Private | -1.2 | -1.1 | 4.7 | -14.9 | -18.5 | -11.1 | -5.7 |

| Residential | -2.8 | -1.4 | 11.8 | -10.9 | -27.8 | -29.1 | -19.7 |

| Nonresidential | 0.2 | -0.9 | -3.6 | -17.7 | -10.6 | 13.2 | 23.1 |

| Public | -1.2 | -1.2 | -0.9 | 1.3 | 3.7 | 5.6 | 13.1 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.