Global| Jan 09 2009

Global| Jan 09 2009U.S. Payrolls Slashed 524,000; Past Data Lowered; 7.2% Jobless Rate Highest Since 1993

by:Tom Moeller

|in:Economy in Brief

Summary

It wasn't bad enough that December nonfarm payrolls were cut 524,000, but downward revisions to prior months left payrolls for the twelve months off 1.9% from one year earlier. That was the weakest performance since the sharp [...]

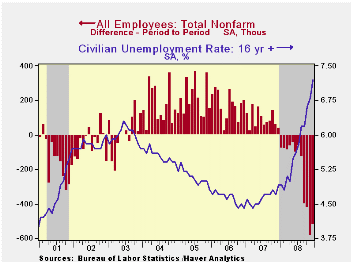

It wasn't bad enough that December nonfarm payrolls were cut 524,000, but downward revisions to prior months left payrolls for the twelve months off 1.9% from one year earlier. That was the weakest performance since the sharp recession of 1982. The latest decline followed cuts of 584,000 and 423,000 during the prior two months resulting in a three-month decline of 1.1%, the worst since the "credit crunch" recession of 1981 according to the Bureau of Labor Statistics. The latest decline exceeded Consensus expectations for a 495,000 drop.

The unemployment rate jumped again, last month to 7.2% which was its highest level since January 1993. The increase exceeded Consensus expectations for a rise to 7.0%. Household sector employment fell 806,000 (-2.0% y/y) for the worst twelve month performance since 1958. The labor force fell 173,000 but it was still up 0.4% y/y. Regardless, the number of potential workers who were not in labor force but wanted a job, i.e. the "discouraged worker," rose by 17.6% y/y. The number of those who were unemployed last month rose 632,000. The figure was up 3.6 million, or 47.3% December-to-December.

The average duration of unemployment rose to 19.7 weeks after falling during November. The latest was near the highest since the early 1980s. The number of those unemployed for more than 27 weeks surged by 17.4% m/m and it nearly doubled year-to-year.

During 4Q, aggregate hours worked, which is employment times the length of the average workweek, fell at a 3.9% annual rate from 3Q. During the last thirty years there has been a 73% correlation between the growth in aggregate hours worked and real GDP growth. The change in worker productivity should result, as it usually does during a recession, in even weaker 4Q GDP growth.

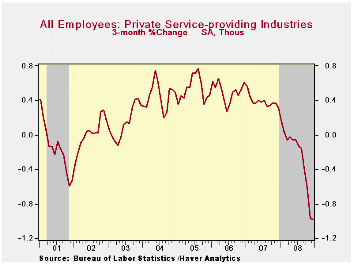

The private service sector has weakened as in no other period during the last 60 years. Over the last three months, 916,000 jobs were shed, or 1.0% of the total. During that period 339,000 jobs were lost from the professional & business services sector and 69,000 were laid off from the financial services sector. Leisure and hospitality jobs were lost by 119,000 and 234,000 were cut from the retail sector. About the only sector to show growth in jobs was health services where jobs rose 112,200 during the last three months. Even jobs in education fell 1,200 during that period.

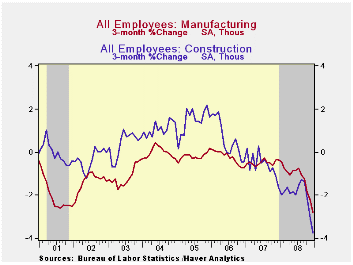

Factory sector jobs were cut by 149,000 last month which was the largest one-month decline since 2001 and the y/y change of -5.7% was the weakest since 2002. Cutbacks have accelerated recently, however, and the three-month change of -376,000, or -2.8%, was the weakest since 1981.

Construction sector employment continued lower, last month by 101,000. That rivaled the largest one-month drop since 1981. The three-month change amounted to -265,000, or 3.7%.

Comparing Current Payroll Employment Changes with Past Recessions from the Federal Reserve Bank of Cleveland is available here.

In the government sector hiring did continue last month. However, the modest 7,000 rise in payrolls followed declines in two of the prior three months. Payrolls are essentially flat since July. That pulled the y/y gain down to 0.8% from a high this past July of 1.5%. The slowdown is most dramatic in local government hiring. At 0.6%, year-to-year growth is off from a 1.7% rate this summer. It mostly reflects a slowdown in education hiring which has been negative in four of the last five months.

The length of the average workweek fell to 33.3 hours, down from 33.7 hours during the first nine months of this year and it was the shortest workweek on record.

Continuing to suggest declines in employment was the one month diffusion index, which measures the breadth of job gain or loss (50 is the break-even level). It fell to its lowest level of this cycle (25.4%). The three-month index also was at its cycle low at 24.1% and the three-month figure for the factory sector was even weaker at 14.3%.

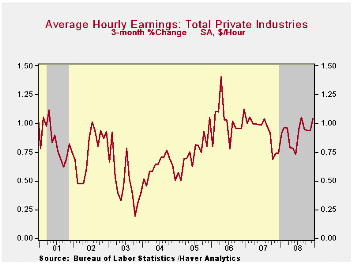

Average hourly earnings rose 0.3% versus an expectation for a 0.2% increase. Earnings the factory sector fell 0.1% (+2.9% y/y) and private services wages rose 0.3% (3.9% y/y).

The U.S. Economic Outlook: The Aftermath of Leverage from Kansas City Fed President Thomas M. Hoenig can be found here.

| Employment: 000s | December | November | October | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|---|

| Payroll Employment | -524 | -584 | -423 | -1.9% | -0.3% | 1.1% | 1.8% |

| Previous | -- | -533 | -320 | -- | -- | -- | -- |

| Manufacturing | -149 | -104 | -123 | -5.7% | -3.1% | -1.9% | -0.5% |

| Construction | -101 | -85 | -79 | -8.5% | -5.8% | -1.0% | 4.9% |

| Service Producing | -273 | -402 | -222 | -1.1% | 0.4% | 1.6% | 1.8% |

| Average Weekly Hours | 33.3 | 33.5 | 33.5 | 33.8 (Dec. '07) | 33.6 | 33.8 | 33.9 |

| Average Hourly Earnings | 0.3% | 0.4% | 0.3% | 3.7% | 3.6% | 4.0% | 3.9% |

| Unemployment Rate | 7.2% | 6.8% | 6.6% | 4.9% (Dec. '07) | 5.8% | 4.6% | 4.6% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief