Global| Oct 22 2007

Global| Oct 22 2007U.S. Loan Delinquencies & Foreclosures Soar

by:Tom Moeller

|in:Economy in Brief

Summary

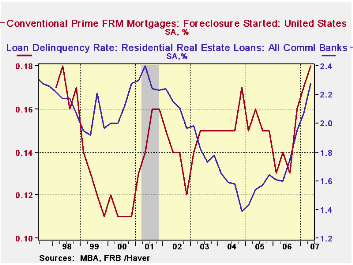

Through the second quarter of this year, delinquent payments on loans at commercial banks in the U.S. has soared to the highest level since 2004. The rate on residential loans is up to the highest since the recession year 2001. The [...]

Through the second quarter of this year, delinquent payments on loans at commercial banks in the U.S. has soared to the highest level since 2004. The rate on residential loans is up to the highest since the recession year 2001.

The data are reported quarterly by the U.S. Federal Reserve Board and are available in Haver's USECON database. The numbers for 2Q 07 will be reported in the next few weeks.

Loan delinquency rates are also available from the Mortgage Bankers Association. They too show an increase. All mortgages past due by 30 days number 3.02% of all mortgages versus a low of 2.77% at the end of 2004.

These data are available in Haver's MBAMTG database.

The rise in the loan delinquencies has prompted a huge increase in mortgage foreclosure rates.

While these rates are still low, foreclosure rates on all mortgages in the U.S. have risen to 0.65% from their quarterly low of 0.40% in 2004. For prime fixed rate mortgages foreclosures have risen to 0.18% from the low of 0.12% in 2002.

The more dramatic increase has been for adjustable rate mortgages. For conventional adjustable rate mortgages (ARMs) the rise the foreclosure rate is noticeable, but to a still very low level of 0.62% from the low of 0.16% in 2004.

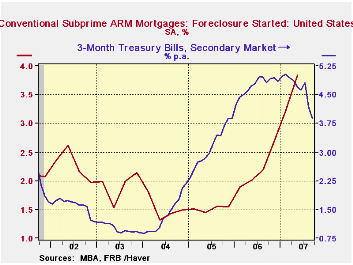

For subprime mortgages, however, the rise in foreclosures has been more dramatic to 2.72% and more than doubled the lowest quarterly rate of 2004. And foreclosure rates on subprime ARMs has about tripled from the quarterly low of 1.32% in 2004. These have clearly followed the past increase in short term interest rates and the latest easing of that rise will (hopefully) lessen the pressure in the mortgage market.Recent Financial Developments and the U.S. Economic Outlook from the Federal Reserve Bank of San Francisco can be found here.

| Delinquency Rate | 2Q 07 | 1Q 07 | 2006 | 2005 | 2004 |

|---|---|---|---|---|---|

| Real Estate Loans | 1.99% | 1.77% | 1.48% | 1.38% | 1.44% |

| Residential | 2.28% | 2.07% | 1.73% | 1.54% | 1.55% |

| Commercial | 1.59% | 1.39% | 1.11% | 1.07% | 1.20% |

| Foreclosure Rate | |||||

| All Mortgages | 0.65% | 0.58% | 1.84% | 1.64% | 1.73% |

| Conventional ARM Mortgages | 0.62% | 0.53% | 0.30% | 0.19% | 0.18% |

| Subprime ARM Mortgages | 3.84% | 3.23% | 2.20% | 1.52% | 1.52% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief