Global| Apr 19 2007

Global| Apr 19 2007U.S. Leading Indicator Weak

Summary

However, the signal for recession is not only a weakening in the LEI but also in the coincident index of economic indicators (COIN). The COIN is weakening only by a very small amount and at a very moderate pace, in effect blunting the [...]

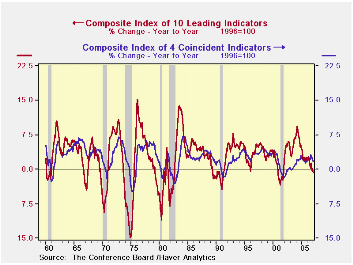

| · The LEI is weak and faltering. One very reliable signal from the LEI is its year/year growth rate. Since the early 1960s, with one exception, significant year/year declines have foreshadowed the onset of recession. The sole exception was in 1966. Although in January 1996 a minor year/year reading of -0.1% also was recorded. Currently the LEI is off by 0.8% year/year – a worrisome signal. |

|---|

| LEADING | COINCIDENT | LAGGING | |

| Month-to-month | |||

| Mar-07 | 0.1% | 0.1% | 0.1% |

| Feb-07 | -0.6% | 0.2% | 0.2% |

| Jan-07 | -0.3% | -0.1% | 0.0% |

| Dec-06 | 0.6% | 0.3% | 0.7% |

| SAAR | |||

| 3-Mos | -2.9% | 1.0% | 0.9% |

| 6-Mos | -0.3% | 1.8% | 4.0% |

| 12-Mos | -0.8% | 1.7% | 3.2% |

However, the signal for recession is not only a weakening in the LEI but also in the coincident index of economic indicators (COIN). The COIN is weakening only by a very small amount and at a very moderate pace, in effect blunting the weakening signal from the LEI itself…at least so far.

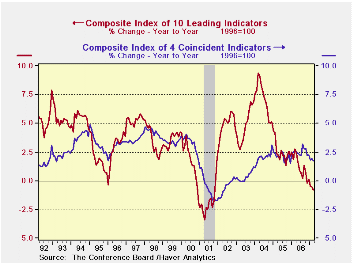

The blown up chart on the right allows closer inspection of the recent LEI and COIN trends. The ongoing and disturbing weakens in the LEI is clear, although its RATE OF DESCENT is not very pre-recession-like. The faltering in the COIN index after a spurt earlier in the year is also put in its less worrisome context, at least for the moment.

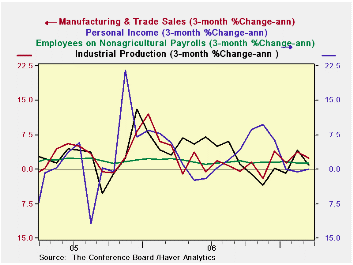

Moreover...if we look at short-term (3-month) growth rates of the COIN components, they still seem to be relatively firm. The coincident index does appear to be about to collapse. It seems still solid.

On balance what we have is evidence of ongoing weakness in the economy. The slippage of the year/year LEI growth rate, below zero and into negative territory, is very disturbing by itself given the reliability of that growth rate as a recession indicator. Yet the LEI itself is slipping at a very slow – almost slow-motion - speed compared to other pre-recession periods. More to the point, for recession to occur the coincident index must decline and the components of that index are showing no sign of doing that. The coincident index itself has undergone some slowing but the index is a product of its components and even three-month growth rates of its components still look quite solid.Verdict: worry but do not grieve for growth. A downturn still looks less than probable.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief