Global| May 15 2018

Global| May 15 2018U.S. Inventories Are Flat in March But Positive Momentum Still Seems in Train

Summary

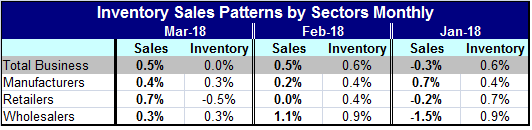

Inventories, whose growth had outpaced sales in previous months, were back to zero growth in March. Meanwhile, the pace of sales overall held at a 0.5% gain in March, the same pace as in February. Over three months we see that the [...]

Inventories, whose growth had outpaced sales in previous months, were back to zero growth in March. Meanwhile, the pace of sales overall held at a 0.5% gain in March, the same pace as in February.

Inventories, whose growth had outpaced sales in previous months, were back to zero growth in March. Meanwhile, the pace of sales overall held at a 0.5% gain in March, the same pace as in February.

Over three months we see that the excess of sales growth has slipped into a deficit relative to sales; inventory growth is outpacing sales. This is a new development and one that does not hold up in the monthly data. Inventory-to-sales ratios, expressed as a percentile standing over the past five years, find that the current inventory-to-sales ratio has only a 50.7 percentile standing- right on top of its historic median which occurs at a 50 percentile standing.

Inventories according to the I-to-S standings are not excessive either overall or on a sector basis. They are moderate to lean.

Inventory growth slowed to flat in March after several months of overstepping the pace of sales growth. But now that is reversed in March. In retailing, sales rose strongly enough in March that inventory levels actually fell. The inventory-to-sales ratio in retailing is now below its median of the last five years, paving the way of inventory rebuilding to occur, especially with the step up in the pace of sales.

The one negative in the report is that trends for sales show that sales over three months have diverged and slowed from the pace of six-month and 12-month. For wholesaling, sales over three months are actually falling. Monthly data place the reason for the three-month sales slowdown as a decline in January for most sectors. Since then, sales have inched back up. For the time being, sales trends are slightly weaker than they have been, but monthly trends suggest that the drop off may have been arrested. Inventory-to-sales ratios are moderate and pose no reason for further inventory entrenchment. Sales in retailing importantly have picked up in monthly data, rising by 0.7% in March and showing a further but slower rise in April (however, that is a bit outside the scope of this report). Still, the news is that sales generally continue to grow and that inventory-to-sales ratios are lean. Wholesaling is the exception. Inventories likely will continue to grow.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief