Global| Dec 02 2008

Global| Dec 02 2008U.S. Gasoline Prices Lowest Since 2005

by:Tom Moeller

|in:Economy in Brief

Summary

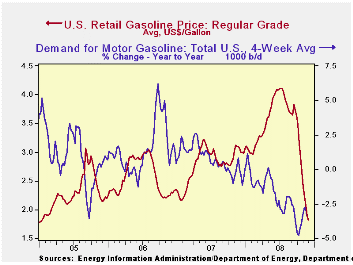

Last week, the pump price for a gallon of regular gasoline was at its lowest level since early 2005 according to the U.S. Department of Energy survey. At $1.81 per gallon prices fell roughly 60 cents per gallon during just the last [...]

Last week, the pump price for a gallon of regular gasoline was at its lowest level since early 2005 according to the U.S. Department of Energy survey. At $1.81 per gallon prices fell roughly 60 cents per gallon during just the last four weeks and they have now fallen $2.30 per gallon, or by 56%, since their peak early this past July. The latest decline was accompanied by a drop in the average price for all grades of gasoline to $1.87 per gallon.

Yesterday, the spot market price for a gallon of regular gasoline fell another four cents from last week's average to $1.14. In futures trading the December contract closed down further at $1.11 per gallon.

Weekly gasoline prices can be found in Haver's WEEKLY database. Daily prices are in the DAILY database.

The U.S. Department of Energy reported that the demand

for gasoline fell by 3.3% y/y. The rate of decline has

bottomed out recently but the decline is still the fastest since

late-1995 (the latest four weeks versus the same four weeks last year).

The demand for all petroleum products also fell

6.6% y/y.

These DOE figures are available in Haver's OILWKLY database.

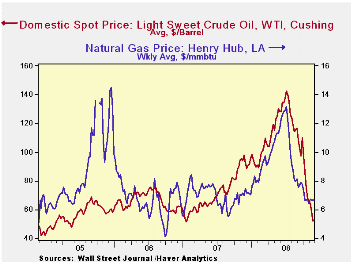

The price for a barrel of West Texas Intermediate crude oil last week ticked up to an average $52.50 per barrel, down by two-thirds since the peak in July of $145.66. In futures trading yesterday, the two-month price for crude oil was even lower at $49.28 per barrel.

Last week, prices for natural gas were stable at $6.66 per mmbtu (-10.4% y/y). The latest average price was nearly one-half below the high for natural gas prices in early-July of $13.19/mmbtu.

Federal Reserve Policies in the Financial Crisis is yesterday's speech by Fed Chairman Ben S. Bernanke and it can be found here.

| Weekly Prices | 12/01/08 | 11/24/08 | Y/Y | 2007 | 2006 | 2005 |

|---|---|---|---|---|---|---|

| Retail Regular Gasoline ($ per Gallon) | 1.81 | 1.89 | -40.8% | 2.80 | 2.57 | 2.27 |

| Light Sweet Crude Oil, WTI ($ per bbl.) | 52.50 | 52.34 | -43.2% | 72.25 | 66.12 | 56.60 |

by Tom Moeller December 2, 2008

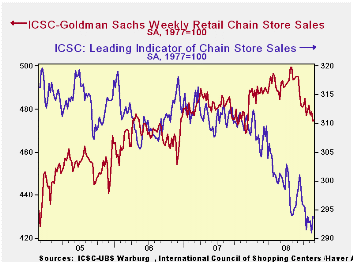

Chain store sales during Thanksgiving week posted all of a 0.1% rise versus the prior week, according to the International Council of Shopping Centers-Goldman Sachs Index. The uptick followed declines near 1% during two of the prior three weeks and it left sales during the month of November down 0.4% from October. The decline last month was the third in the last four. (The uptick in the y/y gain to +1.3% reflected weakness in the 2007 period.)

The level of sales during the latest week remained near the lowest since December of last year.

During the last ten years there has been a 59% correlation between the y/y change in chain store sales and the change in nonauto retail sales less gasoline.

The ICSC-Goldman Sachs retail chain-store sales index is constructed using the same-store sales (stores open for one year) reported by 78 stores of seven retailers: Dayton Hudson, Federated, Kmart, May, J.C. Penney, Sears and Wal-Mart.

The weekly leading indicator of chain store sales from ICSC-Goldman Sachs jumped 1.0% after a 0.7$ decline during the prior week. The indicator remained down 4.9% from the year-ago level and it was near it's lowest level since 1996.

The chain store sales figures are available in Haver's SURVEYW database.

| ICSC-UBS (SA, 1977=100) | 11/29/08 | 11/22/08 | Y/Y | 2007 | 2006 | 2005 |

|---|---|---|---|---|---|---|

| Total Weekly Chain Store Sales | 474.7 | 474.4 | 1.3% | 2.8% | 3.3% | 3.6% |

by Louise Curley December 2, 2008

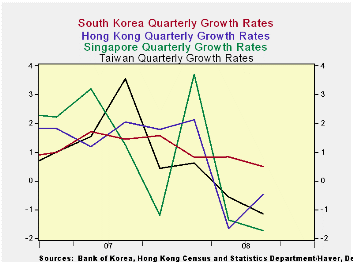

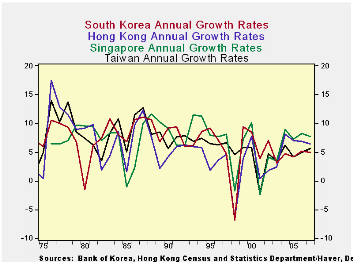

GDP Growth in Asia is clearly decelerating. South Korea, one of the last Asian countries to release their third quarter GDP report, did so today. GDP in Korea increased 0.51% in the third quarter, down from 0.83% in the second quarter and 0.82% in the first.Although there is a clear deceleration in growth over the past year and a half, South Korea has managed to keep increasing output. For the year so far, growth in GDP has averaged an increase of 4.6%, not far from the 5.0% increase in 2007. However, also released today were data on exports and imports for November. Both exports and imports dropped sharply in November, with exports down almost 19% and imports down 17% from October. The November decline in exports should affect fourth quarter GDP adversely.

While the South Korean economy has managed to grow in each of the first three quarters of this year, those of Hong Kong, Singapore and Taiwan, the other three nations along with South Korea formerly known as the Asian Tigers, have begun to decline. In the third quarter real GDP in Hong Kong was 1.56% below the second quarter, in Singapore, 1.74% below and in Taiwan, 1.14% below, as shown in the first chart.

| Change in GDP (%) | Q3 08 | Q2 08 | Q1 08 | 2007 | 2006 | 2005 | 2004 |

|---|---|---|---|---|---|---|---|

| South Korea (Q/Q) | 0.51 | 0.83 | 0.82 | 4.97 | 5.13 | 4.20 | 4.73 |

| Hong Kong (Q/Q) | -1.56 | 1.67 | 2.12 | 6.37 | 9.91 | 6.77 | 8.15 |

| Singapore (Q/Q) | -1.74 | -1.37 | 3.72 | 7.74 | 8.22 | 7.26 | 9.00 |

| Taiwan (Q/Q) | -1.14 | -0.56 | 0.63 | 5.61 | 4.94 | 4.16 | 6.15 |

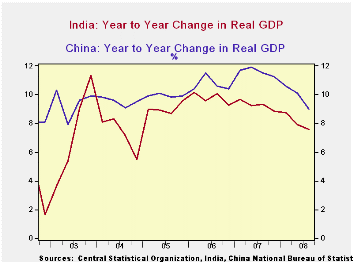

| China (Y/Y) | 9.0 | 10.0 | 10.6 | 11.1 | 10.7 | 8.9 | 9.5 |

| India (Y/Y) | 8.76 | 7.92 | 7.60 | 9.25 | 9.76 | 9.07 | 7.20 |

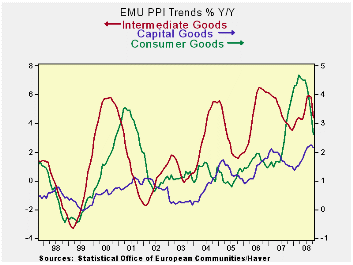

by Robert Brusca December 2, 2008

The Euro Area PPI dropped by 0.8% in October after dropping by

0.3% in September. This drop reduced the total ex-Construction

inflation rate to 6.3% Yr/Yr. Inflation

has dropped to a 4.1% pace over six months and is falling at a 5.8%

pace over three months. Ex-energy

inflation at the PPI level also fell in October. Its pace has dropped

to 3.2% over 12 months 2% over six months and minus one percent over

three months. Germany ,

Italy and the UK each saw ex-energy inflation declining in October.

Three month ex-energy inflation is also well-behaved across these three

countries, falling for two of them and flat over three months in

Germany . PPI inflation

remains quite elevated over 12 months for headline as well for

ex-energy inflation in the Zone as well as in these three key

countries. But with the economy so weak the inflation overshoot is

rightly being ignored. Prospects remain for inflation to fall further.

Economies are weakening and spot oil has fallen below $48/bbl.

| Euro Area and UK PPI Trends | ||||||

|---|---|---|---|---|---|---|

| M/M | SAAR | |||||

| Euro Area 15 | Oct-08 | Sep-08 | 3-Mo | 6-MO | Yr/Yr | Y/Y Yr Ago |

| Harmonized PPI ex Construction | -0.8% | -0.3% | -5.8% | 4.1% | 6.3% | 3.3% |

| Excl Energy | -0.4% | 0.0% | -1.0% | 2.0% | 3.2% | 3.2% |

| Capital Goods | 0.0% | 0.1% | 1.2% | 2.0% | 2.2% | 1.5% |

| Consumer Goods | -0.1% | -0.1% | -0.1% | 1.0% | 2.6% | 3.4% |

| Intermediate & Capital Goods | -0.6% | 0.0% | -1.6% | 2.5% | 3.6% | 3.0% |

| Energy | -2.0% | -1.0% | -18.9% | 9.9% | 15.8% | 4.3% |

| MFG | -1.5% | -0.5% | -9.9% | 0.1% | 3.5% | 3.9% |

| Germany | 0.0% | 0.3% | -1.2% | 7.3% | 7.8% | 1.7% |

| Germany Ex Energy | -0.3% | 0.1% | 0.0% | 2.7% | 2.9% | 2.4% |

| Italy | -1.5% | -0.5% | -7.7% | 2.0% | 5.2% | 3.7% |

| Italy Ex Energy | -0.7% | -0.1% | -2.3% | 0.8% | 3.0% | 3.2% |

| UK | -4.2% | -1.0% | -26.7% | -0.8% | 11.4% | 5.9% |

| UK Ex Energy | -0.5% | 0.3% | -0.7% | 5.6% | 7.0% | 3.8% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief