Global| Oct 16 2009

Global| Oct 16 2009U.S. Factory Production Climbs ForThird Month While Plant Utilization Reaches Seven-Month High

by:Tom Moeller

|in:Economy in Brief

Summary

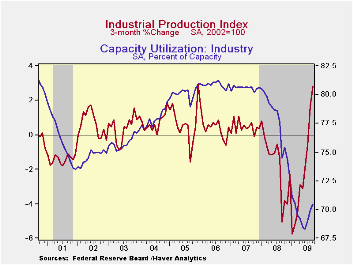

Industrial production is hardly overheating, but the nation's industrial plant is starting to hum again. Output rose a surprising 0.7% during September after gains of 1.2% and 0.8% during the prior two months. An uptick of a meager [...]

Industrial production is hardly overheating, but the nation's

industrial plant is starting to hum again. Output rose a surprising

0.7% during September after gains of 1.2% and 0.8% during the prior two

months. An uptick of a meager 0.1% had been the Consensus expectation,

based on the decline in factory sector employment last month.  The

productivity of those still working thus soared. The recent output

recovery follows a decline of 14.5% during the 21 months of recession

beginning in January of 2008.

The

productivity of those still working thus soared. The recent output

recovery follows a decline of 14.5% during the 21 months of recession

beginning in January of 2008.

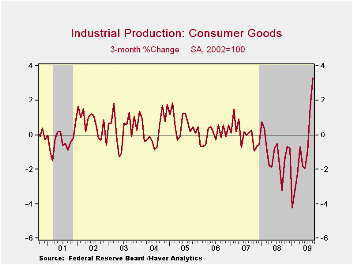

Output of consumer goods rose a firm 1.1% for the third month

of increase following a 10.1% drop during the recession. Production of

autos led the increase with a 7.3% rise, after two months of decline

and a recession loss of 38.5%. Furniture & appliance output

rose a lesser 0.3% which was the second in the last three months. Working the other way, the output of computers, video & audio

equipment showed no sign of recovery, posting a 1.4% (-16.5% y/y)

decline. Outside of the auto and high-tech sectors output ticked 0.3%

higher (-5.3% y/y) during September for the third consecutive monthly

gain. That's against the 12.8% decline during the prior 21 months.

Working the other way, the output of computers, video & audio

equipment showed no sign of recovery, posting a 1.4% (-16.5% y/y)

decline. Outside of the auto and high-tech sectors output ticked 0.3%

higher (-5.3% y/y) during September for the third consecutive monthly

gain. That's against the 12.8% decline during the prior 21 months.

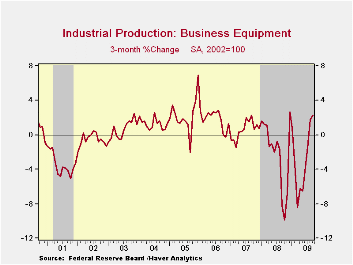

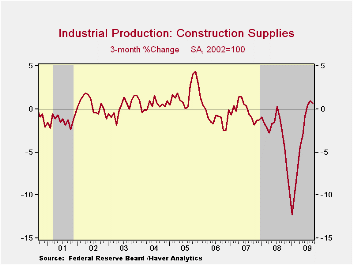

Apparel output rose for third consecutive month of strong gain and the 2.2% increase cut the y/y decline to 11.4%. The output of business equipment rose 0.2% (-8.0% y/y) but the output of construction supplies continued 0.4% (-16.8% y/y) lower after four months of relative stability. Construction supplies output fell 23.4% during this recession.

Excess industrial capacity diminished during September for the

third consecutive month. In the factory sector alone, the rise to 67.5%

also was the third consecutive monthly gain but it nevertheless left

the figure near its lowest of the postwar period. Across industries,

utilization remained the smallest since WWII.

Excess industrial capacity diminished during September for the

third consecutive month. In the factory sector alone, the rise to 67.5%

also was the third consecutive monthly gain but it nevertheless left

the figure near its lowest of the postwar period. Across industries,

utilization remained the smallest since WWII.

The industrial production data are available in Haver's USECON database.

| INDUSTRIAL PRODUCTION (SA, %) | September | August | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|

| Total Output | 0.7 | 1.2 | -6.0 | -2.2 | 1.5 | 2.3 |

| Manufacturing | 0.8 | 1.2 | -7.8 | -3.2 | 1.4 | 2.5 |

| Consumer Goods | 1.1 | 1.5 | -1.8 | -2.6 | 0.9 | 0.4 |

| Business Equipment | 0.2 | 1.1 | -8.0 | -1.1 | 2.7 | 9.4 |

| Construction Supplies | -0.4 | 0.5 | -16.8 | -6.3 | -2.0 | 2.3 |

| Utilities | -0.7 | 1.9 | -2.1 | 0.3 | 3.4 | -0.6 |

| Capacity Utilization | 70.5 | 69.9 | 74.5 (Sept. '08) | 77.5 | 80.6 | 80.9 |

by Tom Moeller October 16, 2009

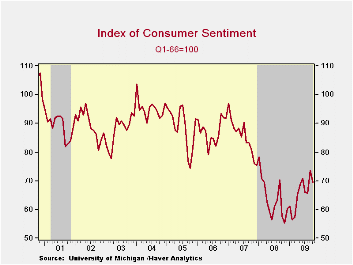

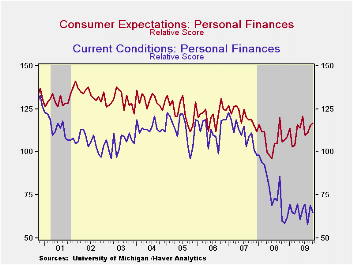

Consumer

sentiment sagged this month but retraced just half of the rise during

September. The University of Michigan's mid-month October reading of

consumer sentiment fell to 69.4 from a September reading of 73.5.

Despite the decline sentiment remained up by roughly one-quarter from

the low last Fall. Consensus expectations had been for no change this

month versus September. During the last ten years, there has been a 69%

correlation between the level of sentiment and the growth in real

consumer spending during the next five months.

Consumer

sentiment sagged this month but retraced just half of the rise during

September. The University of Michigan's mid-month October reading of

consumer sentiment fell to 69.4 from a September reading of 73.5.

Despite the decline sentiment remained up by roughly one-quarter from

the low last Fall. Consensus expectations had been for no change this

month versus September. During the last ten years, there has been a 69%

correlation between the level of sentiment and the growth in real

consumer spending during the next five months.

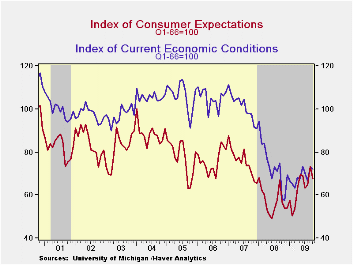

The

latest decline was led by a sharp 18.7% drop in expected business

conditions during the next five years which reversed much of the recent

improvement. Expected conditions during the next year fell just

modestly and the index remained more than double the February low.

Conversely, the expected change in personal finances improved and the

index was up nearly one-quarter from the low during 2008 with the

higher stock market.

The reading of current economic condition fell

just moderately as the reading of personal finances slipped m/m. It has

remained range-bound this year with higher unemployment. The reading of

buying conditions for large household goods held steady m/m but it is

up by one-third from the November low due to low prices.

Expected

price inflation during the next year amounted to 3.1%; up slightly from

September but down from a high of 7% during May of last year. A low of

0.3% inflation was expected by 25% of respondents but 5.0% inflation

was expected by another quarter. Inflation of 3.4% during the next 5-10

years was the mean expectation.

The opinion of

government policy, which may eventually influence economic

expectations, fell slightly from September and remained near

the lowest level since February.

The

latest decline was led by a sharp 18.7% drop in expected business

conditions during the next five years which reversed much of the recent

improvement. Expected conditions during the next year fell just

modestly and the index remained more than double the February low.

Conversely, the expected change in personal finances improved and the

index was up nearly one-quarter from the low during 2008 with the

higher stock market.

The reading of current economic condition fell

just moderately as the reading of personal finances slipped m/m. It has

remained range-bound this year with higher unemployment. The reading of

buying conditions for large household goods held steady m/m but it is

up by one-third from the November low due to low prices.

Expected

price inflation during the next year amounted to 3.1%; up slightly from

September but down from a high of 7% during May of last year. A low of

0.3% inflation was expected by 25% of respondents but 5.0% inflation

was expected by another quarter. Inflation of 3.4% during the next 5-10

years was the mean expectation.

The opinion of

government policy, which may eventually influence economic

expectations, fell slightly from September and remained near

the lowest level since February.  Thirty percent of

respondents thought that a poor job was being done by government. A

reduced 19% thought that a good job was being done. It had hit 30% in

April.

The University of Michigan survey data is not seasonally

adjusted. The reading is based on telephone interviews with about 500

households at month-end; the mid-month results are based on about 300

interviews. The summary indexes are in Haver's USECON database

with details in the proprietary UMSCA database.

Optimism

Amid Uncertainty from the Federal Reserve Bank of Dallas is

available

here.

Thirty percent of

respondents thought that a poor job was being done by government. A

reduced 19% thought that a good job was being done. It had hit 30% in

April.

The University of Michigan survey data is not seasonally

adjusted. The reading is based on telephone interviews with about 500

households at month-end; the mid-month results are based on about 300

interviews. The summary indexes are in Haver's USECON database

with details in the proprietary UMSCA database.

Optimism

Amid Uncertainty from the Federal Reserve Bank of Dallas is

available

here.

| University of Michigan | Mid-October | September | August | Oct y/y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|---|

| Consumer Sentiment | 69.4 | 73.5 | 65.7 | 20.5% | 63.8 | 85.6 | 87.3 |

| Current Conditions | 72.1 | 73.4 | 66.6 | 23.5 | 73.7 | 101.2 | 105.1 |

| Expectations | 67.6 | 73.5 | 65.0 | 18.6 | 57.3 | 75.6 | 75.9 |

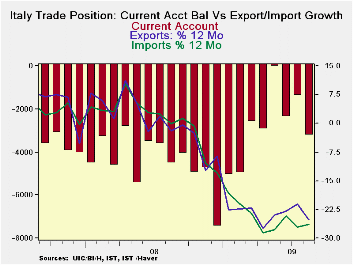

by Robert Brusca October 16, 2009

Italy’s exports and imports both dropped on the month with

exports dropping faster. As a result, the trade gap widened. But the

gap has improved from its worst level at end of 2008. True, the deficit

has expanded again from it best level in May of 2009, but both exports

and imports are on the mend. The export drop this month was

particularly large and therefore it is hard to put in context; it will

take several more months to figure out if this is a new trend of sorts,

or an oddity.

One problem is that Germany, too, had reported a sharp and

unexpected drop in exports. So the Italian drop may have something to

it. Even so it could be that the same rogue factor affected both of

them, it could be a coincidence, or it could be a fundamental weakening

in exports. It will take time to tell

Because of the relatively sharp drop this month, -15.9% for

exports Vs -8.8% for imports, the Yr/Yr trends are probably distorted.

But both export and import growth are down sharply across major

category components (see the table, at the bottom).

While all nations are banking on trade to become an engine of

growth, US demand seems to be slow in starting and most industrialized

economies are having a hard time getting into gear, too. It is in this

environment in which it is hard to see why up to this point exports

have responded so well in the cycle. One man’s export is another’s

import and ultimately is linked to domestic demand which remains

globally challenged: that is the part that is hard to figure out. Whose

export demands have been strong and will they stay that way?

| Italy's Trade Trends | |||||||

|---|---|---|---|---|---|---|---|

| m/mo % monthly rate | Period Specified saar | ||||||

| Seasonally Adjusted | Aug-09 | Jul-09 | Jun-09 | 3-MO | 6-Mo | 12-Mo | Yr-Ago |

| Current Account Bal | €€(3,237) | €€(1,382) | €€(2,378) | €€(2,332) | €€(2,099) | €€(3,656) | €€(3,927) |

| Goods Balance | €€(1,086) | €€814 | €€939 | €€222 | €€592 | €€163 | €€86 |

| Exports | -15.9% | 11.8% | -1.3% | -25.7% | -22.4% | -24.4% | -8.9% |

| Imports | -8.8% | 12.9% | 1.2% | 17.9% | -10.9% | -26.0% | -2.4% |

| Services Balance | €€ 352 | €€ (399) | €€ (788) | €€ (278) | €€ (585) | €€ (766) | €€ (458) |

| Exports | 10.4% | 5.8% | -0.4% | 83.3% | 41.6% | -0.7% | -2.9% |

| Imports | -1.7% | -0.8% | 3.3% | 3.0% | -15.6% | -12.1% | -3.3% |

| Not Seasonally Adjusted | All Yr/Yr | ||||||

| Exports | Aug-09 | Aug-08 | Aug-07 | Aug-06 | |||

| Food&Bev | -1.7% | -1.7% | 7.2% | 10.1% | |||

| Capital Gds | -24.9% | -8.2% | 15.9% | 12.5% | |||

| Transport | -23.9% | -7.9% | 9.0% | 14.9% | |||

| Consumer Gds | -14.1% | -11.5% | 8.0% | 8.3% | |||

| Other Gds | -44.2% | 4.3% | 4.5% | 20.0% | |||

| Imports | Aug-09 | Aug-08 | Aug-07 | Aug-06 | |||

| Food&Bev | -10.5% | -0.5% | 6.4% | 6.9% | |||

| Capital Gds | -22.4% | -10.5% | 13.1% | 6.0% | |||

| Transport | -21.9% | -6.2% | 11.6% | 5.6% | |||

| Consumer Gds | -8.5% | -5.7% | 8.3% | 9.1% | |||

| Other Gds | -42.6% | 9.7% | -0.1% | 33.4% | |||

| Balances in Mlns of euros | |||||||

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief