Global| Jun 02 2005

Global| Jun 02 2005U.S. Factory Inventory Growth Slowed

by:Tom Moeller

|in:Economy in Brief

Summary

Factory inventories rose just 0.1% in April following an upwardly revised 0.7% gain in March. These gains lowered the three month growth in inventories to 5.8%, nearly half the high rate of accumulation set last summer. These figures [...]

Factory inventories rose just 0.1% in April following an upwardly revised 0.7% gain in March. These gains lowered the three month growth in inventories to 5.8%, nearly half the high rate of accumulation set last summer.

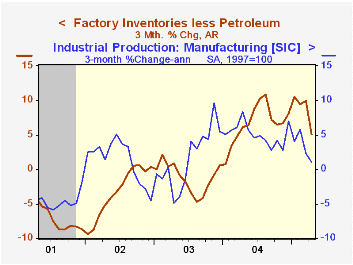

These figures have been bloated by the surge in oil prices. Less petroleum, factory inventories rose 0.1% (8.1% y/y) in April and the three month rate of accumulation slowed to 5.1% versus 10.9% in August.

A slower rate of inventory accumulation has been notable in the furniture industry where three month growth fell to 2.8% from a high of 28.4%. Accumulation of electrical equipment about halved to 9.6% and the level of computer inventories has declined versus a double digit rate of accumulation last summer. The slowdown in other industries has been widespread.

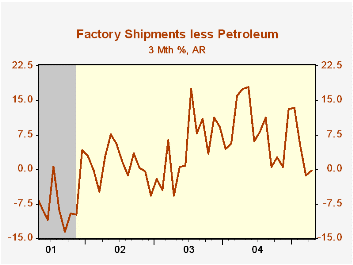

Factory shipments rose a firm 0.7% but here again the trend has weakened. Three month growth fell to 3.1% from a high of 20.4%. Less petroleum recent growth in shipments has been negative versus 17% growth a year ago.

Orders to the factory sector rose 0.9%, juiced by a 1.9% rise in durable goods orders which was unrevised from the advance report.

Unfilled orders were unchanged and the ratio of unfilled orders to shipments fell to a new low.

Do Technological Improvements in the Manufacturing Sector Raise or Lower Employment? from the Federal Reserve Bank of Philadelphia can be found here.

| Factory Survey (NAICS) | April | March | Y/Y | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|

| Inventories | 0.1% | 0.7% | 8.6% | 7.5% | -1.3% | -1.8% |

| New Orders | 0.9% | 0.7% | 6.8% | 10.9% | 3.7% | -1.9% |

| Shipments | 0.7% | 1.6% | 7.8% | 10.5% | 2.6% | -2.0% |

| Unfilled Orders | 0.0% | -0.2% | 6.3% | 9.1% | 4.2% | -6.1% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief