Global| Oct 19 2007

Global| Oct 19 2007U.S. Empire State Index Improved

by:Tom Moeller

|in:Economy in Brief

Summary

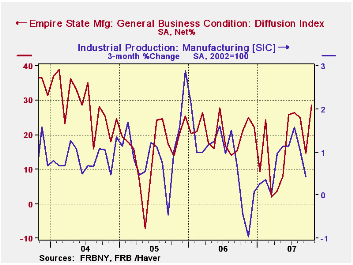

The October index of manufacturing activity in New York State reversed its September deterioration and rose 14.1 points to 28.75, its highest level since July 2004. The figures are reported by the Federal Reserve Bank of New York. [...]

The October index of manufacturing activity in New York State reversed its September deterioration and rose 14.1 points to 28.75, its highest level since July 2004. The figures are reported by the Federal Reserve Bank of New York.

Since the series' inception in 2001 there has been a 55% correlation between the index level and the three month change in U.S. factory sector industrial production.

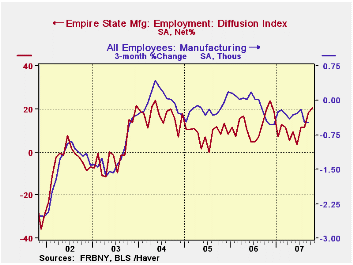

New orders and shipments improved, but employment improved markedly.

In the (perhaps too) short six year history of the NY employment index, there has been an 85% correlation between it and the three month growth in overall factory sector employment.

Like the Philadelphia Fed Index of General Business Conditions, the Empire State Business Conditions Index reflects answers to an independent survey question; it is not a weighted combination of the components.

Pricing pressure rose very slightly. Since 2001 there has been an 81% correlation between the index of prices paid and the three month change in the core intermediate materials PPI.

The Empire State index of expected business conditions in six months rose the highest level in two years.

The Empire State Manufacturing Survey is a monthly survey of manufacturers in New York State conducted by the Federal Reserve Bank of New York. Participants from across the state in a variety of industries respond to a questionnaire and report the change in a variety of indicators from the previous month. Respondents also state the likely direction of these same indicators six months ahead. April 2002 is the first report, although survey data date back to July 2001. For more on the Empire State Manufacturing Survey, including methodologies and the latest report, click here.Monetary Policy under Uncertainty is today's speech by Federal Reserve Board Chairman Ben S. Bernanke and it is available here.

| Empire State Manufacturing Survey | October | September | Oct. '06 | 2006 | 2005 | 2004 |

|---|---|---|---|---|---|---|

| General Business Conditions (diffusion index) | 28.75 | 14.70 | 21.19 | 20.33 | 15.62 | 28.70 |

| Prices Paid | 36.05 | 35.11 | 30.63 | 41.88 | 44.74 | 50.50 |

by Carol Stone October 19, 2007

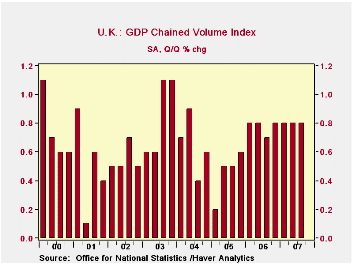

Overall Q3 GDP growth in the UK appears to make for boring reading, at 0.8% Qtr/Qtr for a fourth consecutive time and a sixth time out of the last seven quarters. But with the upheaval in world financial markets coming to a head right in the middle of Q3, we'll be grateful for a steady growth rate. At the same time, a quick look at the table indicates that it is only the total that is steady. Almost every major industrial sector altered its recent trends noticeably during the period to bring offsetting gains and losses.

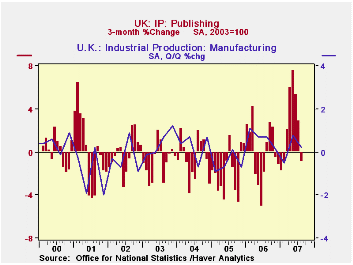

Manufacturing slowed to a 0.2% rise in Q3 from 0.8% in Q2. As with the economy as a whole, segments of manufacturing experienced a mixed performance, according to industrial production data through August, reported about 10 days ago. Food, some metals and transportation equipment appear to have declined in Q3; textiles, chemicals and electrical equipment are flattish, while wood products, furniture and machinery have all been expanding. We noted here three months ago in our discussion of Q2 data that the publishing industry was showing great strength then. That was borne out by later, more complete information showing 6.9% Qtr/Qtr growth in Q2; now, in Q3, that is fading, with output actually down noticeably in August.

Another source of strength in Q2 was mining. Output in that sector has apparently fallen in Q3, but only by 0.3%, according to today's ONS estimates. That is still a far cry from the 8% and 9% declines during 2005 and 2006 and reflects the continuing benefits of the new Buzzard oil field.

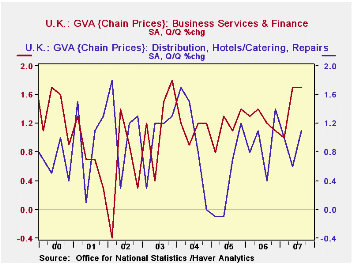

As for the service sectors, Robert Brusca highlighted yesterday the strengthening in retail sales, and that contributed to an estimated 1.1% advance in the distribution industries in Q3, nearly double Q2's 0.6%. Transport and communication also saw a pickup in growth, to 1.1% from 0.8% in Q2. Business services, an area of strong growth in many parts of the world, kept up its already high 1.7% Q2 gain through Q3 as well. The separate construction sector repeated its 0.8% growth in Q1 and Q2 through Q3.

| UK GDP, SA % Chg | Qtr/Qtr Year/Year2006 | 2005 | 2004 | ||||

|---|---|---|---|---|---|---|---|

| 3Q 2007 | 2Q 2007 | 3Q 2007 | 2Q 2007 | ||||

| Total | 0.8 | 0.8 | 3.3 | 3.1 | 2.8 | 1.9 | 3.2 |

| Mining* | -0.3 | 1.3 | -1.8 | -1.3 | -8.2 | -9.2 | -7.2 |

| Manufacturing | 0.2 | 0.8 | 0.6 | 1.1 | 1.3 | -1.2 | 2.0 |

| Services | 1.0 | 0.9 | 4.0 | 3.7 | 3.7 | 2.9 | 3.7 |

| Distribution, Hotels, Restaurants | 1.1 | 0.6 | 4.1 | 3.4 | 3.5 | 1.2 | 5.2 |

| Transportation & Communication | 1.1 | 0.8 | 5.8 | 5.4 | 3.8 | 4.3 | 2.5 |

| Business Services & Finance | 1.7 | 1.7 | 5.6 | 5.1 | 5.3 | 4.5 | 5.0 |

| *Includes oil & gas extraction | |||||||

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief