Global| Jun 24 2009

Global| Jun 24 2009U.S. Durable Goods Orders Surprisingly Strong For A Second Month

by:Tom Moeller

|in:Economy in Brief

Summary

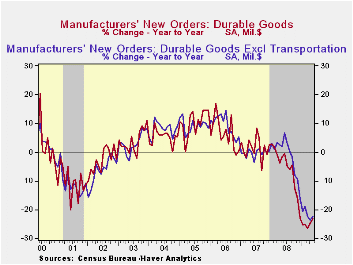

The factory sector is showing some life recently and may be emerging from the moribund state of the last year. The May report of durable goods orders indicated a 1.8% jump following a little-revised 1.8% April gain. The latest [...]

The factory

sector is showing some life recently and may be emerging from the

moribund state of the last year. The May report of durable goods orders

indicated a 1.8% jump following a little-revised 1.8% April gain. The

latest increase easily outpaced Consensus expectations for a

0.8% decline and during the last three months orders have risen at a

5.3% annual rate. That follows a 5.8% decline during all of

last year.

The factory

sector is showing some life recently and may be emerging from the

moribund state of the last year. The May report of durable goods orders

indicated a 1.8% jump following a little-revised 1.8% April gain. The

latest increase easily outpaced Consensus expectations for a

0.8% decline and during the last three months orders have risen at a

5.3% annual rate. That follows a 5.8% decline during all of

last year.

A 3.6% rise (-25.8% y/y) in transportation equipment orders led last month's increase in total durables bookings. That followed a 6.2% rise during April. Higher orders for commercial aircraft led the gain with a 68.1% (-47.7% y/y) surge. Conversely, orders for motor vehicles & parts fell 8.1% (-29.3% y/y) as the auto companies continued to suffer the effects of weak sales. Machinery orders also posted a notable 7.7% increase (-26.9% y/y) after slight uptick in April but electrical equipment orders fell 1.1% (-27.0% y/y) after little change during April. Orders for primary metals rose slightly for the second month but were off by nearly one-half from the year-ago level. Orders for computers & electronic products reversed most of their April decline as computer orders rose 9.4% (-20.2% y/y) but orders for communications equipment slipped m/m and have moved sideways this year.

The capital goods sector may have begun to show life.

Orders for nondefense capital goods recovered an April decline with a

4.8% gain due to the jump in aircraft orders noted above. Nondefense

orders excluding aircraft also firmed but by just enough to return to

the level of last February. During the last ten years there has been an

80% correlation between the y/y change in nondefense capital goods

orders and the change in equipment & software spending in the

GDP accounts. The correlation of the GDP figure with capital goods

shipments is, as one would expect, a larger 92%.

The capital goods sector may have begun to show life.

Orders for nondefense capital goods recovered an April decline with a

4.8% gain due to the jump in aircraft orders noted above. Nondefense

orders excluding aircraft also firmed but by just enough to return to

the level of last February. During the last ten years there has been an

80% correlation between the y/y change in nondefense capital goods

orders and the change in equipment & software spending in the

GDP accounts. The correlation of the GDP figure with capital goods

shipments is, as one would expect, a larger 92%.

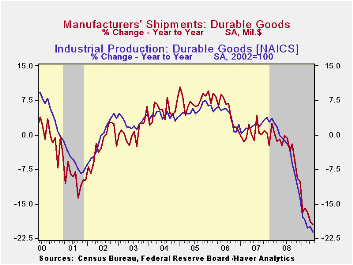

As might be expected, the improvement in orders has yet to show up in higher shipments. Shipments of durable goods fell 2.1% last month (-19.5% y/y) and have fallen in each month since February of last year. That y/y decline in shipments has been accompanied by a 21.1% y/y drop in industrial production of durable goods. During the last ten years, there has been an 80% correlation between the change in shipments of durable goods and the change in durables industrial production.

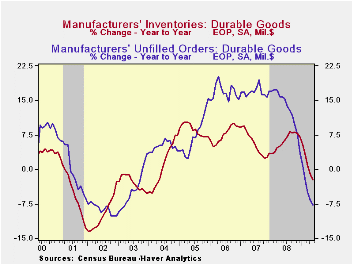

Inventories of durable goods fell for the fifth

consecutive month. The 0.8% decline followed a 1.1% April decline that

was deeper than reported initially. On a three-month basis decumulation

of durable goods inventories has been at a near-record 13.5% rate.

Quick decumulation of inventories has been notably across industries.

Backlogs in order books have fallen in each of the last eight months

and during the last year by 7.7%, a rate of decline which is the

sharpest since 2003.

Inventories of durable goods fell for the fifth

consecutive month. The 0.8% decline followed a 1.1% April decline that

was deeper than reported initially. On a three-month basis decumulation

of durable goods inventories has been at a near-record 13.5% rate.

Quick decumulation of inventories has been notably across industries.

Backlogs in order books have fallen in each of the last eight months

and during the last year by 7.7%, a rate of decline which is the

sharpest since 2003.

The durable goods figures are available in Haver's USECON database.

Taming the Credit Cycle by Limiting High-Risk Lending from the Federal Reserve Bank of Dallas is available here.

| NAICS Classification (%) | May | April | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|

| Durable Goods Orders | 1.8 | 1.8 | -23.3 | -5.8 | 1.4 | 6.2 |

| Excluding Transportation | 1.1 | 0.4 | -22.4 | -1.2 | -0.3 | 9.1 |

| Nondefense Capital Goods | 10.0 | -2.9 | -26.9 | -6.8 | 3.5 | 9.4 |

| Excluding Aircraft | 4.8 | -2.9 | -21.8 | -0.3 | -2.7 | 10.7 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief