Global| Oct 25 2007

Global| Oct 25 2007U.S. Durable Goods Orders Down Big for Second Month

by:Tom Moeller

|in:Economy in Brief

Summary

Durables goods orders fell sharply in September by 1.7% following a 5.3% drop during in August. That was revised slightly deeper from the initial report. Much of series' volatility is due to orders in the transportation sector. [...]

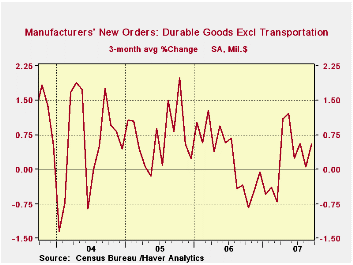

Durables goods orders fell sharply in September by 1.7% following a 5.3% drop during in August. That was revised slightly deeper from the initial report. Much of series' volatility is due to orders in the transportation sector. Excluding transportation (which still can be volatile), orders rose a slight 0.3% after an unrevised 1.8% decline during August.

The very short term trend in the non-transportation series shows some improvement, but that is due to a 3.3% jump back in July for which the latest two months' results can be viewed as a payback. But before that jump the longer term trend in orders growth was down, as was the trend in overall orders for durable goods.

Weakness in orders for electrical equipment, appliances and components most assuredly reflects weakness in the consumer sector. That also is true of computers where the latest three month growth recovered to a bare 1.6%, up from negative growth in the prior two periods and down from the peak in orders growth of 15.3% early his year.

To a limited degree, orders for nondefense capital goods less the very volatile aircraft component are holding up. These orders rose 0.4% last month after a 0.1% August decline. Three month growth of 0.4% is up from negative growth just recently and is a big recovery from the excessive declines between 1% and 2% early this year.

Machinery orders led that relative strength and rose 4.3% last month and the three month average growth is 5.5%. Orders for primary metals rose 1.6% and the average rise over the last three months also is an average 1.6%, up from negative growth earlier

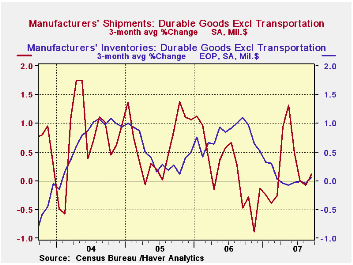

Growth in shipments, however have weakened even more. Overall shipments growth is down to -0.0% on average over the last three months and less transportation it's +0.1%. That's versus growth rates over 1% earlier this year.

Inventories are lean. Average growth over the last three months totals only 0.1% versus average growth rates in excess of 1% late last year.

Unfilled orders also have picked somewhat to a recent average growth rate of 0.9% but that' down from 14.1% during all of 2006.

| NAICS Classification | September | August | Y/Y | 2006 | 2005 | 2004 |

|---|---|---|---|---|---|---|

| Durable Goods Orders | -1.7% | -5.3% | -6.6% | 6.3% | 9.9% | 5.3% |

| Excluding Transportation | 0.3% | -1.8% | 0.1% | 7.6% | 8.8% | 7.9% |

| Nondefense Capital Goods | 4.4% | -10.2% | -11.4% | 10.6% | 17.1% | 5.7% |

| Excluding Aircraft | 0.4% | -0.1% | .2% | 8.5% | 11.1% | 3.2% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief