Global| Dec 16 2005

Global| Dec 16 2005U.S. Current Account Deficit Improved Slightly

by:Tom Moeller

|in:Economy in Brief

Summary

The US current account deficit improved slightly last quarter to $195.8B but it was from a 2Q deficit that was revised deeper. Also lessening the economic significance of the improvement, it was entirely due to a narrower unilateral [...]

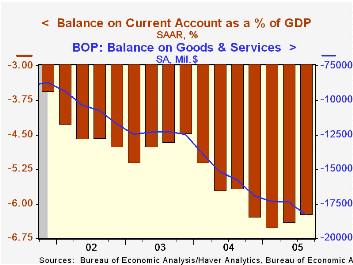

The US current account deficit improved slightly last quarter to $195.8B but it was from a 2Q deficit that was revised deeper. Also lessening the economic significance of the improvement, it was entirely due to a narrower unilateral transfers deficit caused by private transfers associated with hurricanes and homeland security.

The 3Q current account deficit amounted to 6.2% of GDP and is averaging 6.4% this year versus 5.7% in 2004. Consensus expectations had been for a deepening of the 3Q deficit to $204.6B.

The deficit in merchandise trade deteriorated to a record $197.9B from $186.9B in 2Q. Exports grew just 0.8% (10.0% y/y), held back by the damage to Gulf Coast port facilities caused by Hurricane Katrina. Imports, meanwhile, rose 3.1% (13.6% y/y) in large part due to the 17% surge in value of petroleum products.

The surplus on services improved for the fourth consecutive quarter to $15.1B and rose versus a surplus of $10.3B a year ago. Exports of services grew 1.9% (11.7% y/y and imports were roughly flat q/q (6.8% y/y).

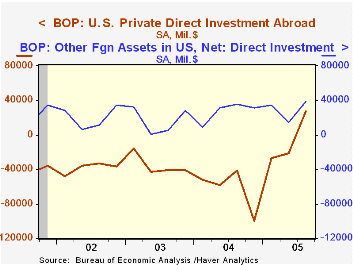

From the capital account, net US foreign direct investment abroad was positive for the first time since 1982 while foreign direct investment in the US surged to its highest since 2001.

| US Int'l Balance of Payments | 3Q '05 | 2Q '05 | Y/Y | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|

| Current Account Deficit | $195.8B | $197.8B | $167.0B | $668.1B | $519.7B | $475.2B |

| Goods/Services/Income Deficit | $182.3B | $175.1B | $151.2B | $587.1B | $448.5B | $411.2B |

| Exports | 2.6% | 3.6% | 13.9% | 14.9% | 6.8% | -3.7% |

| Imports | 3.0% | 3.0% | 15.8% | 18.1% | 7.3% | 1.6% |

| Unilateral Transfers Deficit | $13.5B | $22.6B | $20.5B | $80.9B | $71.2B | $64.0B |

by Tom Moeller December 16, 2005

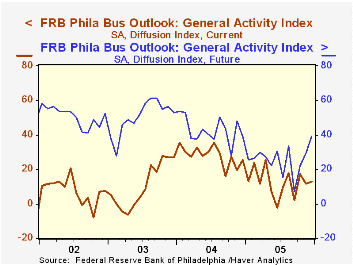

The December Index of General Business Conditions in the manufacturing sector from the Philadelphia Fed rose slightly to 12.6 from 11.5 the prior month. Consensus expectations had been for improvement to 14.0.

During the last ten years there has been a 68% correlation between the level of the Philadelphia Fed Business Conditions Index and three month growth in factory sector industrial production. There has been a 50% correlation with q/q growth in real GDP.

The sub index measuring new orders fell sharply as did the shipments index though both remained positive. The index covering the number of employees and delivery times also fell. These declines were offset by increases in unfilled orders and inventories. During the last ten years there has been a 64% correlation between the employment index and the three month growth in factory payrolls.

The business conditions index reflects a separate survey question, not the sub indexes.

The separate index of expected business conditions in six months improved a sharp 10 points to 39.0 and was at its best level in a year. Expectations for employment also jumped to the highest level since January but capital spending intentions fell.

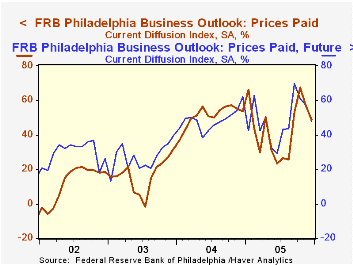

The prices paid index fell for the second month to a still high reading of 49.0. During the last ten years there has been a 75% correlation between the prices paid index and the three month growth in the intermediate goods PPI. The correlation with the finished goods PPI has been 50% and with the CPI it's been 43%.

The Philadelphia Fed index is based on a survey of 250 regional manufacturing firms, but these firms sell nationally and internationally. How Well Do Diffusion Indexes Capture Business Cycles? A Spectral Analysis from the Federal Reserve Bank of Richmond is available here.

The latest Business Outlook survey from the Philadelphia Federal Reserve Bank can be found here.

| Philadelphia Fed Business Outlook | Dec | Nov | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|

| General Activity Index | 12.6 | 11.5 | 12.5 | 28.1 | 10.6 |

| Prices Paid Index | 49.0 | 56.8 | 43.6 | 51.3 | 16.8 |

by Carol Stone December 16, 2005

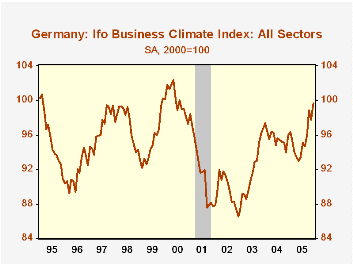

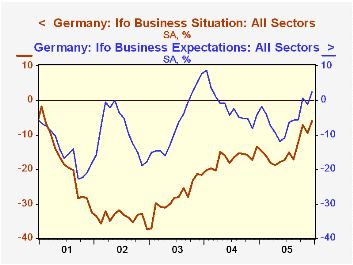

Business is looking better in Germany. Just three days ago, Louise Curley discussed the ZEW Investor Survey, which showed a surprising gain. Now we have the parallel business confidence data compiled by Ifo, a German economic research institute, from a survey of 7,000 business firms in manufacturing, construction and trade. This survey, too, as the ZEW, turned in a favorable performance for December, better than market expectations. The "Business Climate Index" is 99.6 (2000=100), with the component "Business Situation" and Business Expectations also both at 99.6. All three indicators improved from 97.8 in November. The improvement was shared by all major industry segments in the survey, manufacturing, construction, wholesale and retail trade.

Accompanying these indexes are diffusion measures showing the balance of better and worse conditions. These diffusion gauges have generally been negative, that is, more business managers continue to experience deterioration than growth. Still, there is considerably less deterioration than in the recent past. The overall business climate gauge is -1.7% in December, its best level since August 2000 and up from -14.9% last May. Current conditions are -6.0%, the best since January 2001 and much better than April's -18.7%. Expectations are +2.6. This last, reflecting business leaders' persistent hopes for better times, has frequently been positive, most recently in late 2003 and early 2004.

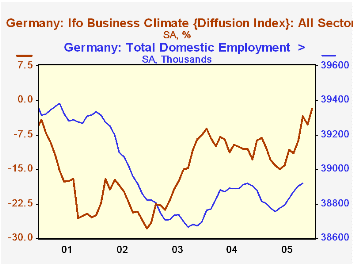

These improvements seem stronger than some views expressed recently -- prompted perhaps by the riots in neighboring France, by recent political uncertainty and by high energy costs -- that Germany is mired in a distressing economic morass. But the upturns in these confidence measures began about mid-year and survived all those negative weights on the economy. Offsetting these factors has been the weaker euro and commensurate advance in German competitiveness. Further, even employment has been increasing. Since bottoming in April, employment has risen 164,000 and the locally defined unemployment rate has eased from 12.0% in March to 11.5% in November, still high but well below the peak. Thus, the German economy looks better, and this week investors in the ZEW survey and business leaders in the Ifo poll have agreed with that perspective.

| Ifo Indexes, 2000=100, SA | Dec 2005 | Nov 2005 | Oct 2005 | Year Ago | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|---|

| Business Climate | 99.6 | 97.8 | 98.8 | 96.0 | 95.7 | 91.7 | 89.4 |

| Diffusion % | -1.7 | -5.3 | -3.4 | -8.8 | -9.6 | -17.5 | -22.0 |

| Business Situation | 99.6 | 97.8 | 98.9 | 95.8 | 94.0 | 88.3 | 85.3 |

| Diffusion % | -6.0 | -9.5 | -7.3 | -13.4 | -17.0 | -27.9 | -34.0 |

| Business Expectations | 99.6 | 97.8 | 98.6 | 96.3 | 97.4 | 95.1 | 93.8 |

| Diffusion % | +2.6 | -1.1 | +0.6 | -4.1 | -1.8 | -6.5 | -9.1 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief