Global| Jan 20 2006

Global| Jan 20 2006U.S. Consumer Sentiment Rose Further

by:Tom Moeller

|in:Economy in Brief

Summary

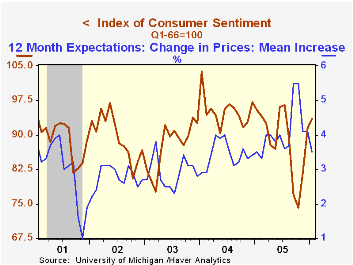

The University of Michigan reported that consumer sentiment in January rose another 2.1% to 93.4. The rise was the third off the October low which has totaled 25.9% and the gain surpassed Consensus expectations for an increase to [...]

The University of Michigan reported that consumer sentiment in January rose another 2.1% to 93.4. The rise was the third off the October low which has totaled 25.9% and the gain surpassed Consensus expectations for an increase to 92.5.

During the last ten years there has been a 76% correlation between the level of consumer sentiment and the y/y change in real consumer spending.

The current conditions index rose 2.7% as the reading of buying conditions for large household goods rose sharply back to last year's high, though the reading of personal finances fell slightly (-4.1% y/y). Consumers' assessment of gov't economic policy (-12.2% y/y) improved to the highest level since October.

Consumers' expectations increased a moderate 1.6% following the 15.2% December spurt. Expected business conditions during the next year and during the net five years rose but expectations for personal finances gave back most of a December surge.

The mean expected inflation rate for the next twelve months fell to 3.5% from 4.1% and was below the 5.5% expected in October & September.

The University of Michigan survey is not seasonally adjusted.The mid-month survey is based on telephone interviews with 250 households nationwide on personal finances and business and buying conditions. The survey is expanded to a total of 500 interviews at month end.

| University of Michigan | Jan | Dec | Y/Y | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|

| Consumer Sentiment | 93.4 | 91.5 | -2.2% | 88.6 | 95.2 | 87.6 |

| Current Conditions | 112.0 | 109.1 | 1.0% | 105.9 | 105.6 | 97.2 |

| Expectations | 81.5 | 80.2 | -4.9% | 77.4 | 88.5 | 81.4 |

by Tom Moeller January 20, 2006

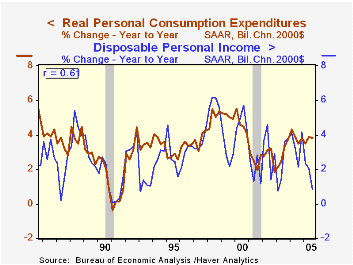

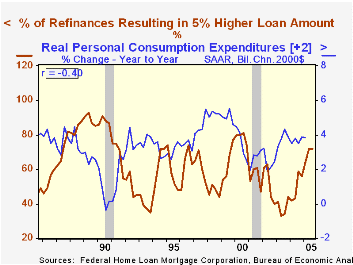

Worry that some potential bursting of the "bubble" in housing market valuations at least in part rests on the idea that homeowners are borrowing against those "inflated" values to support current spending.

In fact, real spending growth of 3.8% over the last year vastly exceeded the growth in real disposable income of 0.8%; prima fascia evidence of unaffordable profligate spending? And Freddie Mac (FMAC) reported that in 3Q05, mortgage "cash out" refinancing activity rose to the highest level (72%) since 2000. An increased percentage of homeowners increased their loan amounts by 5%.

Over the last twenty years, however, it didn't take some real estate bubble to generate these conditions. Today's cash out refinancing may be nothing other than what previously was termed a second mortgage. And this pejorative terminology was used when economic times were about to weaken.

Since 1985, the correlation between the level of cash out refinancing and the change in real consumer spending has been a statistically significant negative 40%. The correlation with spending on durables has been an even higher -57%. A piece of that spending surely was supported by the second mortgage, but the more likely rationale for spending growth has been income.

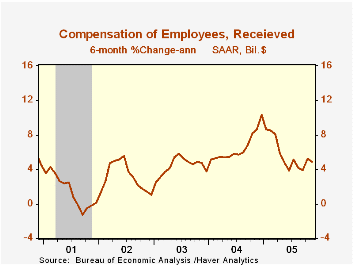

Real compensation growth has suffered due to the latest rise in inflation and also the comparison to what was heady growth late in 2004. Most recent growth in compensation, however, has been encouraging as improved job creation has held nominal compensation growth at 5%, and inflation pressure has abated somewhat.

Will that be enough to forestall a crash in spending tied to burst housing market valuations? For many, no, but for most the future decision to spend will depend on the fundamentals of income and employment.

House of Cards from the Federal Reserve Bank of Richmond can be found here.

Cash-Out Refinancing: Check It Out Carefully from the Federal Reserve Bank of St. Louis is available here.

Has the Housing Boom Increased Mortgage Risk? from the Federal Reserve Bank of Dallas can be found here.

| Freddie-Mac Cash Out Refinance Activity | 3Q05 | 2Q05 | 3Q04 | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|

| 5% Higher Loan Amount | 72% | 72% | 59% | 50% | 38% | 52% |

| Median Appreciation of Refinanced Property | 23% | 23% | 17% | 11% | 7% | 16% |

by Carol Stone January 20, 2006

Consumers in several countries are maintaining a rather firm spending pace, judged by new data on retail sales and purchases of goods. In fact, in Holland, the last few months have seen a smart rebound from a weak performance in 2003 and 2004. At the same time, some spending in France and New Zealand has tapered down recently.

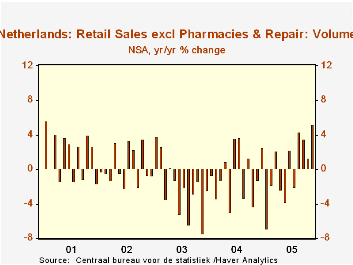

In the Netherlands, weakness plagued retail sales through the middle of 2005. A usual vacation-related drop in August did not materialize this year, though. So by November, the latest figures reported just this morning by the Central Bureau of Statistics show sales volume up 5.1% from a year earlier. The so-called headline portion excludes pharmacies and repair services; this subset was up 5.2%.

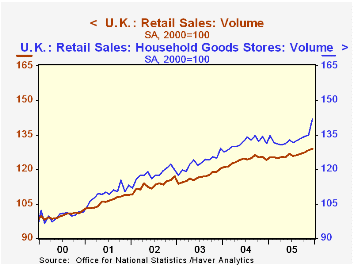

A good gain was also apparent in the UK. In December, the ONS reported today, December sales rose 0.5% from November, putting the month 4.8% ahead of a year earlier, the best 12-month performance since November 2004. As seen in the second chart here, household goods are a contributing factor, although other store groups enjoyed sales expansions since about mid-2005.

In New Zealand, retail sales have been flat overall for the past three months ending November, but prior to that time, they trended higher pretty consistently at about 0.5%/month from the middle of 2004.The very latest pattern reflected a wide swing in demand for motor vehicles, which was strong in August and November, but fell steeply in between.In the months when car sales were up, other spending paused. This is a change for New Zealand retailers; these auto and non-auto sales have generally moved together, not in opposition.

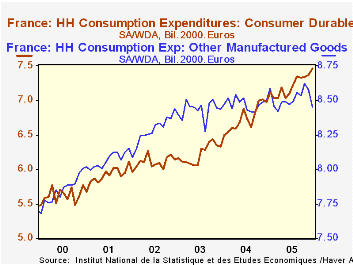

Finally in France, sales have also slowed in recent months. And as in New Zealand, this reflects a reallocation of purchases.The measure we have is purchases of manufactured goods, and it does not represent all of retail sales. What we see is a firm advance in durable goods, led by automobiles.As people have made those big-ticket purchases, they have pulled back on electronics, which had previously been growing. Purchases of “other manufactured goods” and “textiles and leather” have been erratic but largely flat for the last three years.

We are somewhat surprised by the increases that are evident in all these countries since 2003. Anecdotal evidence has suggested that consumers have been restrained perhaps by poor labor market conditions or rising energy costs, but in these particular countries, hard data indicate that people have still been able to expand their purchases, with durable goods in particular being in good demand.

| Retail Sales | Latest Level | Dec 2005 | Nov 2005 | Oct 2005 | Year Ago | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|---|---|

| Netherlands: | ||||||||

| Total (2000=100) | 101 | -- | 5.1** | 1.2** | -- | -- | -0.6 | -2.2 |

| Headline* | 101 | -- | 5.2** | 1.3** | -- | -- | -0.6 | -2.1 |

| France: | ||||||||

| Manufactured Goods (Bil.2000.Euros) | 19.7 | -1.0 | 0.7 | 0.1 | 1.4 | 2.5 | 3.3 | 1.9 |

| Durable Goods (Bil.2000.Euros) | 7.5 | 1.2 | 0.4 | 0.2 | 6.9 | 7.0 | 8.4 | 2.0 |

| Other Manufactured Goods (Bil.2000.Euros) | 8.5 | -1.5 | -0.6 | 1.1 | -0.5 | 0.4 | 0.5 | 1.8 |

| UK: | ||||||||

| Total (2000=100) | 129.0 | 0.5 | 0.9 | 0.4 | 4.8 | 1.9 | 6.0 | 3.2 |

| New Zealand: | ||||||||

| Total (Bil.NZ$) | 5.0 | -- | 0.9 | -0.3 | 5.6 | -- | 7.9 | 5.3 |

| Ex Auto Items (Bil.NZ$) | 3.6 | -- | -0.1 | 1.0 | 6.1 | -- | 7.4 | 5.6 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief