Global| Sep 19 2019

Global| Sep 19 2019U.K. Retail Sales Weaken in August- But What About the Outlook?

Summary

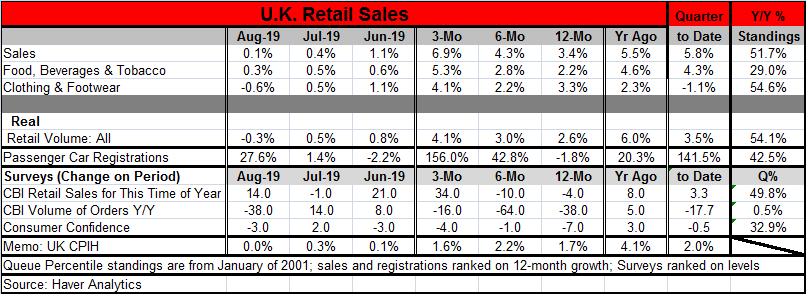

U.K. nominal retail sales ticked up 0.1% in August while sales volume fell by 0.3%. The slowing was unexpected, but sales growth is still solidly in place. Nominal sales are up by 3.4% over 12 months and sales over six months are [...]

U.K. nominal retail sales ticked up 0.1% in August while sales volume fell by 0.3%. The slowing was unexpected, but sales growth is still solidly in place. Nominal sales are up by 3.4% over 12 months and sales over six months are faster and sales growth over three months are faster still. Nominal sales are accelerating despite the weak result in August. Real sales (or sales volume) are up by 2.6% over 12 months and sales accelerate over six months and again over three months. Not all monthly slowing in sales lead to a broader slowdown although the future is still speculative.

U.K. nominal retail sales ticked up 0.1% in August while sales volume fell by 0.3%. The slowing was unexpected, but sales growth is still solidly in place. Nominal sales are up by 3.4% over 12 months and sales over six months are faster and sales growth over three months are faster still. Nominal sales are accelerating despite the weak result in August. Real sales (or sales volume) are up by 2.6% over 12 months and sales accelerate over six months and again over three months. Not all monthly slowing in sales lead to a broader slowdown although the future is still speculative.

As of August, sales are two months into the third quarter. The two-month average for sales grows compared to the Q2 base (quarter-to-date growth rate) is at a 5.8% annualized rate for nominal sales; the pace is at a very solid 3.5% for sales volume in the quarter-to-date. Both are quite solid and acceptable.

Separately, passenger car registrations have suddenly advanced strongly, gaining 27.6% month-to-month, at a 156% annualize rate over three months and at a 141.5% rate in the quarter-to-date. These astonishing growth rates are despite registrations falling by 1.8% compared to 12-months ago. August one year ago also had a spike and a somewhat larger spike in registrations. That is the reason for erosion in the year-to-year change. We should brace for a likely contraction in registrations next month. The chart below makes these factors clearer than any verbal description of them could be. It also shows that registrations actually have been in a declining phase since 2016 and that ‘spikes' don't change that trend.

Separately, passenger car registrations have suddenly advanced strongly, gaining 27.6% month-to-month, at a 156% annualize rate over three months and at a 141.5% rate in the quarter-to-date. These astonishing growth rates are despite registrations falling by 1.8% compared to 12-months ago. August one year ago also had a spike and a somewhat larger spike in registrations. That is the reason for erosion in the year-to-year change. We should brace for a likely contraction in registrations next month. The chart below makes these factors clearer than any verbal description of them could be. It also shows that registrations actually have been in a declining phase since 2016 and that ‘spikes' don't change that trend.

Nominal retail sales ranked on 12-month growth rates back to 2001 stand at their 51st percentile. Clothing sales stand in their 54th percentile with food, beverages & tobacco purchases much weaker in their 29th percentile. Sales volumes rank in their 54th percentile putting nominal and real sales growth rates in roughly the same relative positions, just above their respective median values (medians occur at a ranking at the 50th percentile).

Retail sales on their own appear to be fine, healthy not strong or weak, and logging acceptably firm growth rates.

But that upbeat message is not so for all retail indicators. The CBI reading on sales for ‘time of year' (essentially seasonally adjusted sales) improved month-to-month to a 49.8 percentile standing which is only the thinnest margin below its median standing. However, the change in the volume of orders month-to-month in the same survey fell sharply to a -38.0 reading in August, more than unravelling the +14.0 gain in July. Its year-on year change also showed a -38.0 point deterioration. This survey metric is ranked on its index level and that that registers one of the weakest results ever with a 0.5 percentile standing. That reading is the lowest reading on this timeline although back in December 2008 there was a weaker reading. This time the weakness is a probable reaction to Brexit as firms imported madly to build stocks in the event of a Brexit gone wrong and in the wake of that it would be expected that orders would regress sharply. However, consumer confidence also back-stepped in August and the level of the consumer confidence in August has a weak 32.9 percentile standing- a standing in the bottom one third of its historic queue of observations.

On balance, retail trends seem acceptable. But the survey from the CBI and the consumer confidence readings suggest that there may still be trouble ahead for the British consumer.

BOE, Brexit and growth

The Bank of England met and released its policy statement today, also holding policy steady but warning of the evils of a hard Brexit. The BOE spoke to the weakness that a hard Brexit would engender and noted that interest rates would likely be lower longer as a result and that the pound sterling would be weaker as well. However, we know that depending on the magnitudes of these things that they may not go hand in hand. The BOE cut rates in the wake of the Brexit vote and that cut destabilized the pound whose drop caused inflation to rise and overshoot and led to future BOE rate increases. So the BOE's statement about the currency and interest rate situation has some assumptions about how severe sterling's reaction might be. We need to remember that the leg bone is connected to the knee bone and that what happens to one often affects the other.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief