Global| Aug 15 2019

Global| Aug 15 2019U.K. Retail Sales Continue to Stand Up

Summary

Despite the risks, U.K. retail sales continue to expand Despite ongoing concerns over Brexit, a plunging pound sterling, and inflation that has risen above the BOE target, U.K. retail spending is holding up. There has even been some [...]

Despite the risks, U.K. retail sales continue to expand

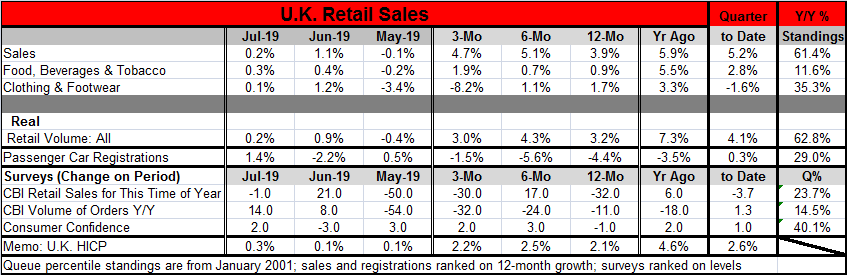

Despite ongoing concerns over Brexit, a plunging pound sterling, and inflation that has risen above the BOE target, U.K. retail spending is holding up. There has even been some marginal improvement in consumer confidence. Sales rose by 0.2% in July after spiking by 1.1% in June. Retail sales volume gained 0.2% in July after a 0.9% gain in June.

Despite the risks, U.K. retail sales continue to expand

Despite ongoing concerns over Brexit, a plunging pound sterling, and inflation that has risen above the BOE target, U.K. retail spending is holding up. There has even been some marginal improvement in consumer confidence. Sales rose by 0.2% in July after spiking by 1.1% in June. Retail sales volume gained 0.2% in July after a 0.9% gain in June.

Sequential growth rates slow

More broadly, the pace of retail sales is slowing even though it is growing. Sales slowed their pace over three months dropping to a pace of 4.7% from 5.1% over six months. But that is still faster than the 3.9% sales rise over 12 months. In real terms, the slowing is more apparent as the three-month pace at 3% is slower than the six-month pace of 4.3% and slightly slower than the 12-month pace of 3.2%.

Car registrations show weakness

Passenger car registrations that rose on the month by 1.4% still show declines over three months, six months, and 12 months. But registrations are not in a decelerating pattern; the three-month pace of decline is less weak than either the six-month pace or the 12-month pace.

Retail survey shows weakening

The CBI survey for sales evaluated expectations for 'this time of year' finds sales weaker over three months and 12 months. The volume of orders, while higher in July, is showing drops and progressively deeper drops from 12-month to six-months and from six-months to three-months. Even so, consumer confidence has showed a slight recent revival.

QTD sales are rising

The early quarter-to-date reading shows nominal sales up at a 5.2% pace with sales volumes up at a 4.1% pace. Sales are continuing to expand at a very solid pace early in Q3, compared to their average level in Q2.

Sales are moderately firm

When we rank year-over-year sales growth rates in July among all growth rates back to 2001, the pace of nominal sales ranks at its 61st percentile; the sales volume growth rate ranks at its 62nd percentile. The median for sales growth occurs at a 50th percentile ranking. For both of these series, sales rank above their respective medians although neither is especially strong. We can look as the sales pace as moderately firm.

The path ahead

U.K. retail sales are holding up. The U.K. economy has been performing with some irregularity and the Brexit exit date is coming into focus with a deadline at October 31. The U.K. has a relatively new Prime Minister in Boris Johnson who has been proclaiming his desire for a hard Brexit, trying to get the EU to renegotiate Brexit terms with him. But the EU has not engaged him on this matter. Instead, as parliament gets ready to meet, the focus has shifted to domestic opposition by many parliament members to a hard Brexit. Johnson has been acting as though he was in control and would get his way on the matter. However, now that his 'honeymoon' transition is over it appears that he too will face substantial opposition to his vision. Just as Theresa May was unable to bridge the gap between those preferring to leave at any cost and those wanting to keep ties to the EU, Boris Johnson is finding that being in the driver's seat does not necessarily improve the vision through the windshield or enable him to make the twists and turns through traffic he would like to make if left to do so on his own. He must play the well-known political game of 'Mother may I.' Johnson may find that he has some considerable domestic deal-making to do instead of simply trying to bluff and bully the EU and bluster the press.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief