Global| Aug 20 2019

Global| Aug 20 2019U.K. Orders: Considerable Recovery But Still Considerable Weakness

Summary

U.K. industrial orders, output and pricing show less weakness than the one-month lagged EU Commission metric or the Markit manufacturing metric. But ranked over a shorter span, since 2015, the U.K. data appear extremely weak and they [...]

U.K. industrial orders, output and pricing show less weakness than the one-month lagged EU Commission metric or the Markit manufacturing metric. But ranked over a shorter span, since 2015, the U.K. data appear extremely weak and they are more in line with the EU Commission's weak reading. Your take on reality, it seems, depends on where you stand.

U.K. industrial orders, output and pricing show less weakness than the one-month lagged EU Commission metric or the Markit manufacturing metric. But ranked over a shorter span, since 2015, the U.K. data appear extremely weak and they are more in line with the EU Commission's weak reading. Your take on reality, it seems, depends on where you stand.

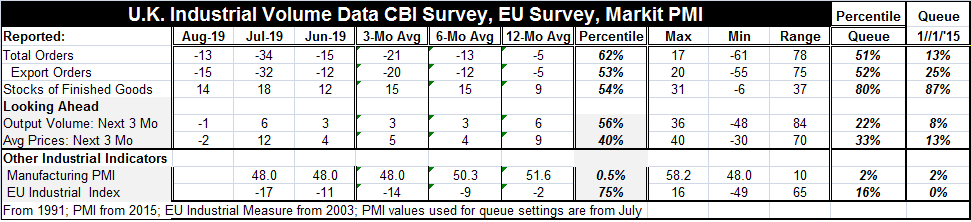

Total orders had fallen to a very weak -34 in July, but in August they are back up to -13, a bit better even than their June reading. At a 51st percentile queue standing on data back to 1991, the current reading is moderate. That reading is just above its historic median on data back to 1991. On the queue of data since January 2015, however, the ranking is in its lower 13th percentile. U.K. orders are moderate according to a longer term historic profile but weak in comparison with recent performance.

Export orders mirror those metrics and comparisons as export orders rebounded to -15 in August from -32 in July, but export orders are still below their June level. Their historic rank standings are in line with those of total orders but a bit stronger.

Stocks data are less volatile overall. But they have a high standing in their top 20th percentile or higher on both ranking periods. Stocks are above their 12-month average, while both order series have weakened in comparison with their respective orders series.

Output expectations have done a flop-flip. Expected output is now weaker in August than in July even as orders have become sharply less weak month-to-month. The July reading of 6 was a bounce and it had gotten the series back to its 12-month average, but in August expectations have fallen to generate a -1 expectations reading for three-months ahead. That volume expectation is weak on both of the historic timelines I use to rank the data. It leaves output expectations in the lower 22nd percentile or even weaker.

Prices expected three-months ahead fell sharply from the sharp rise to 12 in July to a much lower -2 reading in August. The minus two reading is the second negative value in four months, but one must go back to 2016 to find other negative readings and to February 2016 find a negative reading weaker than -2.

The U.K. survey picks up the economic weakness and concern about prices, even though the U.K. CPI measures have crept above its target pace of 2%.

Brexit is coming. Boris Johnson is here. And Johnson is trying every trick in the book to get some compromise out of the EU over Brexit. Johnson has tried threatening a hard Brexit, but his support at home evaporated as he sang that tune loudly making it an ineffective weapon to use against the EU. He has tried to further claim that the Irish backstop is unjust but has been unable to come up with a viable alternative. Right now Boris is looking like he is all bark and no bite, unless you allow for biting yourself.

Mark Carny at the BOE has already said that negative interest rates are not right for the U.K. economy. In any event, U.K. inflation is over the top of its target not below it. But there is no telling what a bungled Brexit could do.

The expectations embodied in the CBI Survey show a certain loss of optimism despite the rebound this month. The negative readings and the low rankings of current and expected assessments show a loss in momentum. Output expectations have been steadily slipping and stock levels have been creeping up. On the same timeline, price expectations have been fading. The U.K. is not a euro area member; it has its own currency. But the U.K. trades a great deal with Europe and Europe's economic conditions naturally have an impact on conditions in the U.K. European weakness, as well as fear of Brexit going wrong, are putting the U.K. in a difficult corner.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief