Global| May 01 2015

Global| May 01 2015U.K. Manufacturing PMI Drops Sharply

Summary

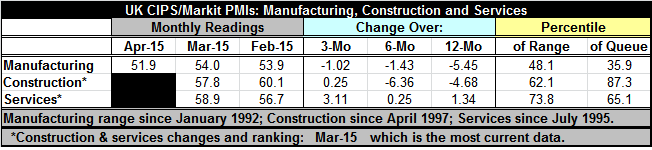

Only the U.K. manufacturing index is available for April. That indicator fell sharply to 51.9 in April from 54.02 in March. This is the manufacturing sector's sharpest one-month drop since February 2013 when it fell by more than three [...]

Only the U.K. manufacturing index is available for April. That indicator fell sharply to 51.9 in April from 54.02 in March. This is the manufacturing sector's sharpest one-month drop since February 2013 when it fell by more than three points in one month.

Only the U.K. manufacturing index is available for April. That indicator fell sharply to 51.9 in April from 54.02 in March. This is the manufacturing sector's sharpest one-month drop since February 2013 when it fell by more than three points in one month.

The manufacturing drop was unexpected; the large drop obviously was unexpected. The construction and services sectors have been embroiled in a slide for some months. However, services, like manufacturing, was showing some sign of revival. The services sector made a local peak at 60.5 in August of last year and then fell to 55.8 in December; since then, the services sector has been gaining. That pattern of recovery was accompanied by a similar rebound in manufacturing. Those patterns made it look like revival was in train. Wrong! That revival, at least in manufacturing, has just turned sour. This manufacturing report takes the notion of ongoing recovery off the table and leaves us in quandary about how the U.K. economy is going to behave.

The percentile standing statistics bear out how weak the recovery has been. The manufacturing PMI sits only in the 35th percentile of its historic queue of values in April, a very weak reading. Construction- through March- sits in the 87th percentile of its queue, a relatively strong position. The service sectors which is rising and posted a strong increase in March still only sits in the 65th percentile of its queue, a very modest position.

On balance, the U.K. economy is still struggling. The PMI gauges show little evidence of strength except for construction which is the smallest sector. Manufacturing is hurt in part because of the U.K. proximity to Europe and the euro area where the euro has been very weak along with growth.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief