Global| Nov 19 2020

Global| Nov 19 2020U.K. Manufacturers Lose Hope

Summary

Some people live for hope. Others see hope as an opiate to get through the day. In reality, 'hope' is the quintessential 'four-letter word' because if it is improperly calibrated, it can be used for manipulation. But if it is fairly [...]

Some people live for hope. Others see hope as an opiate to get through the day. In reality, 'hope' is the quintessential 'four-letter word' because if it is improperly calibrated, it can be used for manipulation. But if it is fairly formed, it can have a powerful supportive impact. The key about the nature of hope is its truthfulness. And that is something we really never know. So that is the real problem with hope, we never know if it is a good or a bad four-letter word.

Some people live for hope. Others see hope as an opiate to get through the day. In reality, 'hope' is the quintessential 'four-letter word' because if it is improperly calibrated, it can be used for manipulation. But if it is fairly formed, it can have a powerful supportive impact. The key about the nature of hope is its truthfulness. And that is something we really never know. So that is the real problem with hope, we never know if it is a good or a bad four-letter word.

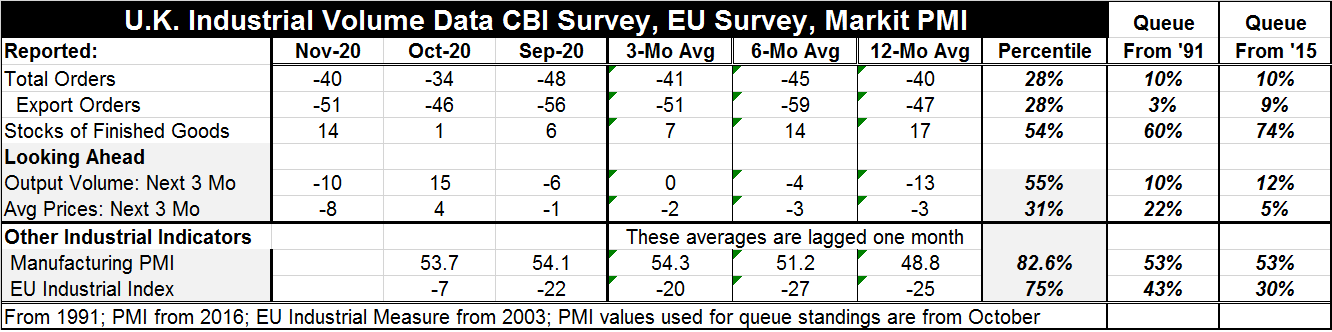

The Confederation of British Industry survey has one measure related to hope and that is its series on output expectations for the next three months. In this survey, when I speak of hope I am using this survey metric which I assume is more or less fairly formed because, although firms may seem to have an incentive to paint a brighter picture of the future than what really exists, in fact, that would be a dangerous thing to do. Firms need to plan for the future and operate in the environment that presents itself. Excessive optimism can be costly to a business. 'Hope' must be benchmarked to reasonable expectations by business. In this case, British firms have had a setback in their assessment of hope.

The volume of output expectations is set back to a reading of -10 in November. The reading was last this weak in August of this year. But it, of course, reached its low point in April at a value of -67 as the first wave of virus appeared. However, the outlook was at a +8 in February and a +4 in January before the virus struck. These positive values were the first two 'plus' readings in five months at the time as August through December 2019 produced a string of adverse expectations. These developments and this 'timing' make it harder to evaluate the U.K. data.

The U.K. case is complicated to evaluate because the economy has been reeling under the uncertainty of a Brexit deal (and still has uncertainly over a trade deal) on top of the impact of the virus which is spreading again. Both Brexit and virus are undergoing a sort of rebound or second round impact. If we compare the current output expectations reading to the January-February period before the virus struck, we see degradation in expectations. But if we compare the current reading to the average outlook reading in the five months from August to December 2019 (well before the virus), we compare the current -10 metric to a value of -9. It appears in this context not changed very much at all.

The current situation...

Total orders have negative readings for 20 months in a row. Over that period there are only six readings worse that the current reading in November; all those are from April to September of this year has the virus interrupted activity. So except for a slightly better October reading, the post-April readings on current orders are still the worst among the last 20 months - all of which had negative responses to the outlook. That makes November a still dismal reading and might make it look like it is more of virus effect because of its extreme weakness.

Export orders

Export orders have the same string of weakness as orders and as that reading fell to -51 in November; it has had only five worse readings over the same last 20 months and they are May through September of this year. Foreign demand is being hit on about the same cycle as in the home market, which is not surprising given the virus is the cause of this economic mischief.

Price expectations

Prices whose expectations have been 'weak' over the last 20 months have actually seen declines in only about half of those months. But the current reading of -8 on price expectations is the weakest in those 20-months except for April, May and June of this year, when the virus was most intense.

Brexit needs

The picture that is developed from this process finds the U.K. still struggling. There remain uncertainties about what post-Brexit life will be like because there is no trade deal with the EU… yet. The EU desperately wants fishing rights in U.K. waters, so the U.K. is not without a bargaining chip of some importance. But as yet there is no deal. Nissan has been warning Britain that for it to continue to operate there it needs a trade deal with the EU to give it preferred market access. Brexit uncertainty is an important factor in this survey.

The virus

However, the virus also is spreading again. The number of cases is up to one million four hundred thousand (plus) as of November 18. That is up by 98% over one month and the month ago total was up by 87% from a month before that. Clearly, the U.K. infection has been spreading fast. The daily infection total is well above the earlier peak of April. In April, there was a spike-high at 7,860. This time there is a spike-high at 33,470, but that was on November 12; that has since settled down to a daily rate of 19,609 and the daily total has been steadily diminishing. Still, the daily total is above the levels of one month ago. However, then new cases were accelerating and now they are decelerating. Total deaths that were pretty flat from June to early-October are on the rise above the 40,000 mark around which data had clustered and now deaths are up to 53,274. The daily death toll may still be on an upswing; the data are not yet clear on that.

Virus and fear

Those metrics make it clear that the U.K. is still in the middle of an outbreak. It may be on cusp of getting control of it but as we have seen these things go in the past, even that will require some vigilance to keep the trends moving lower. The virus spreads virulently, but it does not kill so widely. But no one wants to get it so the spread frightens people and that tends to restrict economic activity especially when supplemented by a government order to curtail activity. The U.K. is in that spot.

Other eco-surveys say...

Other survey data such as the EU industrial index find the UK industrial sector was last stronger 18 months ago (current reading is October). There is a special deterioration in the rating in April, May and June. But the last reading higher than October was in April 2019. That suggests strongly that the weakness here transcends just the virus. Apart from a few recent months (August and September), the U.K. manufacturing PMI was last stronger in March 2019. And that precedes the virus by a good bit. The U.K. looks like it is dealing with double barreled trouble.

Summing up

Against its challenges, the U.K. economy has done remarkably well. But there is still a Brexit end game to conclude. And while I would give the U.K. economy very good marks for having muddled through its morass of difficulty as well as it has, it continues to face steep challenges ahead. It may be some time before the British economy is out of the woods on its difficulties.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief