Global| Mar 12 2019

Global| Mar 12 2019U.K. IP Struggles to Advance

Summary

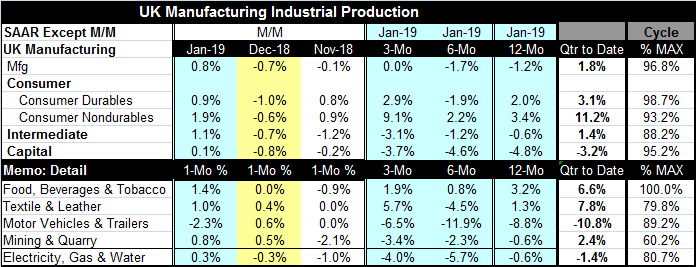

Manufacturing output in the U.K. rose by 0.8% in January after a 0.7% decrease in December and a 0.1% slip in November. On balance, these shifts leave IP with no growth over the last three months. That is an improvement on its six- [...]

Manufacturing output in the U.K. rose by 0.8% in January after a 0.7% decrease in December and a 0.1% slip in November. On balance, these shifts leave IP with no growth over the last three months. That is an improvement on its six-month rate of -1.7% and on its 12-month rate of -1.2%. Still, the reversal of weakness is wholly due to the improvement in one single month, January. And one month does not determine a reliable trend of any sort.

Manufacturing output in the U.K. rose by 0.8% in January after a 0.7% decrease in December and a 0.1% slip in November. On balance, these shifts leave IP with no growth over the last three months. That is an improvement on its six-month rate of -1.7% and on its 12-month rate of -1.2%. Still, the reversal of weakness is wholly due to the improvement in one single month, January. And one month does not determine a reliable trend of any sort.

Growth

Looked at by sector, we see some very different and distinct results. Consumer durable goods and nondurable goods show growth of 2% to 3.5% over 12 months while intermediate goods output declines over 12 months and capital goods output plunged by nearly 5% over 12 months.

Momentum

Momentum is different by sector as well. Capital goods output that is very weak over 12 months finds its pace of decline slightly attenuated over six months and again over three months. However, intermediate goods, with a small decline over 12 months, declines faster over six months and faster still over three months. Consumer nondurables output builds momentum from 12-months to three-months albeit somewhat erratically. Consumer durables does somewhat the same as nondurables but with less vigor overall.

Brexit

Clearly, firms are planning for and handicapping what business will be like under the as yet not formulated Brexit deal. On the face of these rules, capital equipment producers seem a bit more concerned and may have taken steps to shift output to Europe in order to minimize the business disruption under Brexit. On the face of it, consumer goods producers would appear to be less affected and may feel that they produce more for the domestic market or for non-European customers and members of the commonwealth.

The New Deal

Theresa May has just finished her latest and probably her last round of negotiations to try to establish a deal that Parliament can accept or might approve. And while she has portrayed her new deal as a watershed and delivering what Parliament has asked for, upon bringing the deal home to her top lawyer, he still did not see the new deal as one that avoided the potential permanent trap in the EU customs union – one key element that the U.K. has sought to ditch by exiting the EU. However, the new deal does seem to be an improvement. But is it enough? The Irish Prime Minister also sees the newly minted deal as insufficient. With so much bargaining and back and forth, it is no wonder that British business is having a hard time sorting out its future and sticking to its own knitting.

Where manufacturing stands

Still, manufacturing is less than 4% shy of its last cycle peak. Consumer durables and nondurables are at more than 90% of their respective past peaks. Capital goods output, despite its recent declines, is at 95% of its cycle peak. Intermediate goods output is at a lower at 88% of its cycle peak. U.K. producers are not straining capacity and yet still seem to have reasonably strong levels of output. By industry, food, drink and tobacco is one that is at its cycle peak. Motor vehicles sit at the threshold of the 90th percentile of their cycle peak. Textiles and leather as well as utilities are lower, near their respective 80th percentiles nearly 20% below their respective cycle best. Mining and quarrying are at a much lower 60th percentile of their past cyclical peak- showing lots of slack.

The end game

However, January, despite all the uncertainties and weak growth in surrounding Europe, has been rebound month for consumer goods, intermediate goods and in a very small way even capital goods. All industries in the table except motor vehicles also show a gain in January. And on a quarter-to-date basis, most sectors and industries are advancing. But it is still true that no one knows what the future will look like. And with the severance date for leaving Brexit on this month’s calendar, that is a pretty scary situation.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief