Global| Mar 11 2015

Global| Mar 11 2015U.K. IP Prevaricates as Does Policy

Summary

On a day when Bank of England Governor Mark Carney has said that it would be foolish to cut interest rates to combat low inflation, the U.K. has also produced a sharp weakening in its industrial sector. Manufacturing output is lower [...]

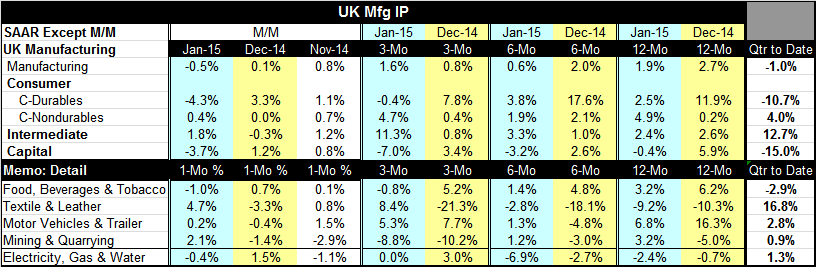

On a day when Bank of England Governor Mark Carney has said that it would be foolish to cut interest rates to combat low inflation, the U.K. has also produced a sharp weakening in its industrial sector. Manufacturing output is lower by 0.5% just one month after cutting its gain to razor-thin 0.1% gain. In the quarter to date (January over the Q4 average), the manufacturing IP growth rate is at a minus one percent. Consumer durables output is off in the quarter at a 10% annual rate. Capital goods output is off at a 15% annual rate. These plunges are offset by consumer nondurables where output is up at a 4% pace and intermediate goods where output is up strongly at a 12.7% pace. Still, it's not a very encouraging profile.

On a day when Bank of England Governor Mark Carney has said that it would be foolish to cut interest rates to combat low inflation, the U.K. has also produced a sharp weakening in its industrial sector. Manufacturing output is lower by 0.5% just one month after cutting its gain to razor-thin 0.1% gain. In the quarter to date (January over the Q4 average), the manufacturing IP growth rate is at a minus one percent. Consumer durables output is off in the quarter at a 10% annual rate. Capital goods output is off at a 15% annual rate. These plunges are offset by consumer nondurables where output is up at a 4% pace and intermediate goods where output is up strongly at a 12.7% pace. Still, it's not a very encouraging profile.

Sequential growth rates are more ambiguous with manufacturing output slowing over six months then speeding up over three months but to a pace still lower than its 12-month pace. Intermediate goods show a sequential increase in growth rates while capital goods show a sequential deterioration. Consumer durables and nondurables show unclear patterns.

The U.K., like the U.S., is fighting off the effects of a falling euro. The imposition of QE in the EMU and its clear weakened state makes ECB policy clear as a bell. Meanwhile, Mark Carney has signaled that the U.K. will not engage in race to bottom on interest rates or exchange rates. But that does not mean that they don't matter. The U.K. is losing competiveness to the EMU nations and it does a lot of trade in the region and competes with those nations' exports in third markets. The dropping euro does put pressure on the U.K. economy as well as on the U.S. economy.

The selected detail on IP sectors shows little evidence of a revival in output trends by industry. We are still not fully convinced that the EMU QE program will bear fruit; there may not be much pick-up in growth in Europe to compensate U.K. exporters for their loss in competiveness due to the euro drop vs. sterling.

Incoming news from China shows a slowing of industrial output and in retail sales. Japan reported weaker core machinery orders. Yesterday the OECD's leading indicators were consistent with continuing growth but showed no hint of acceleration. Yet, in global markets yesterday U.S. stocks sold off after the release of some minor economic reports that were actually on the weak side. What is going on with markets?

Markets are wary of the future, yet all but `certain' about part of it. They can see that central banks are running out of tricks and thinking of getting back to normalcy. The ECB came late to the QE party so it is having its QE moment and impact on markets now even though its program comes with rates so low we can doubt the program's ability to gain traction. Mark Carney at the BOE has just declared that further rate drops are not the answer. In the U.S., the Fed members are shifting toward raising rates despite some clear ongoing flaws in the U.S. growth story. My view of yesterday's market selloff is that it simply reflects that the ECB started QE and that has drilled home the different policy paths in the U.S. and Europe.

There is a view that the Fed is headed- inexorably- to a rate hike so why wait until the actual date is clarified? While various Fed member statements seem to make that true, there is the little problem of the Fed having had cumulative inflation below 2% for all past horizons of 10 years and less and with inflation `expected to be' below 2% for the next two years ahead on the Fed's own central tendency basis. Yet, the Fed seems to be able to `believe' that it can know this year - even with oil prices collapsing- that inflation can soon be on a sustainable path to 2%. And this belief will be the trigger for a policy rate rise. Really! I am not making this up!

This is the fly in the monetary policy ointment. The Fed's own criterion for hiking rates is not being met and probably can't be met on the time horizon most have for a Fed rate hike this year. Central bankers are getting very nervous about the endless stimulus, but they do not seem to have been able to find a way out. It's as though they have entered a maze that they can't get out of. Continued sluggish growth will not do it. Will a dropping unemployment rate caused by labor market drop-outs do it? That is probably the most relevant question. But it's not part of the Fed's criterion and other central banks aren't being even that forthcoming about what it will take for them to turn rates around.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief