Global| Sep 18 2019

Global| Sep 18 2019U.K. Inflation Is Even More Tempered

Summary

High inflation is one less thing that the Bank of England has to worry above as the U.K. CPIH was flat in August, dropping its year-over-year pace to 1.7%, its slowest annual gain since November 2016. The 'core' excluding food, [...]

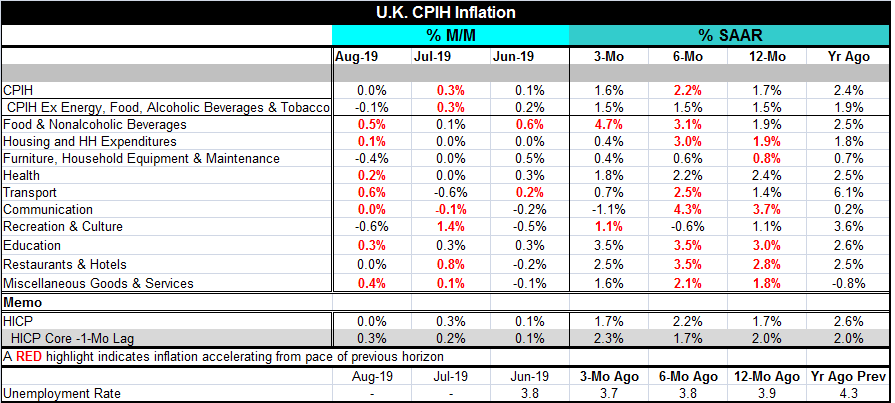

High inflation is one less thing that the Bank of England has to worry above as the U.K. CPIH was flat in August, dropping its year-over-year pace to 1.7%, its slowest annual gain since November 2016. The 'core' excluding food, alcohol and tobacco fell by 0.1% in August, dropping its 12-month pace to 1.5% and marking its smallest 12-month gain since August 2016.

High inflation is one less thing that the Bank of England has to worry above as the U.K. CPIH was flat in August, dropping its year-over-year pace to 1.7%, its slowest annual gain since November 2016. The 'core' excluding food, alcohol and tobacco fell by 0.1% in August, dropping its 12-month pace to 1.5% and marking its smallest 12-month gain since August 2016.

Even so month-to-month inflation accelerated in seven of ten major categories. Inflation had only accelerated in four categories in July and in two in June. Because the proportion of sectors with inflation acceleration has been muted recently, this month's breadth of pick up may not be meaningful. Still, it bears watching.

Over 12 months inflation decelerated compared to its 12-month pace of one year ago as the pace fell to 1.7% from 2.4%. The core fell to a 1.5% pace from a 1.9% pace. Still, by categories, price expansion accelerated on the comparisons in six of ten categories. These trends also accelerated in seven of ten categories over six months compared to 12 months as the overall rate moved up to 2.2% from 1.7%. But inflation subsequently went quiescent as the three-month pace fell to 1.6% and only two categories showed inflation picking up over three months compared to six months.

While the U.K. struggles to map out a less disruptive Brexit strategy, the plot of the EMU HICP vs. the U.K. CPIH shows how, despite having separate currencies, Europe and the U.K. share the same inflation cycles. Over the last five years the U.K. CPIH has risen at a compounded pace of 1.6% while the EMU HICP pace has increased at a 1.0% annual rate. Under shooting in the U.K. still exists since both the BOE and the ECB has the same 2% target, but since Brexit has weakened the pound sterling the overall inflation undershoot in the U.K. is less than it is in the EMU area.

The BOE is preparing to make policy in the midst of whatever follows in the wake of Brexit. Of course, this is unknown. The risk of a hard Brexit which is the most disruptive case is still high as Boris Johnson has continued to set that as the prime alternative if he cannot get the deal he wants from the EU. No one is quite sure how much this is a real threat or how much is a bluff, but if it does not work as a bluff to get a sweetened deal then Mr. Johnson will almost certainly have backed himself into a corner that would require him to force a hard Brexit like it or not. So there continues to be a great deal of political posturing and actions taken to try to thwart Mr. Johnson's shuttering of Parliament as to prelude to a hard Brexit. Just as adamantly Mr. Johnson continues to pursue a path to a hard Brexit while negotiating with EU officials. A few days ago Mr. Johnson was quoted as saying negotiations were going well and he was on his way to a new a deal. Today the EU warned of being headed to a damaging no deal Brexit saying that the U.K. had to do more than just complain about aspects of the deal negotiated by Theresa May that it did not like. In short, Boris needs to come up with an alternative plan, some real meat, instead of just his long standing beef.

For now the U.K. economy is still growing year-on-year although GDP took a setback in Q2 2019, falling by 0.8% (SAAR). Capital formation and housing have taken a big hit as uncertainty about what the future will look like has kept new investment largely on the sidelines. And the interaction between the U.K. and European economy brings more weakness to the fore as German growth is contracting with growth in EU up at only a 0.8% pace in the second quarter. The U.K. and Europe are in the grip of weakness and both have underperforming inflation. With a shock from Brexit that could sting both areas- and hit the U.K. harder- policy-making in Europe and in the U.K. remains more of an art than science especially with the region wrapped in the enigma of global economic policies. The good news for the BOE in all this is that inflation is muted since a hard Brexit seems to lay waiting in the wings. Having accelerating inflation now would but the BOE in the most difficult of circumstances since it likely would not want to be hiking rates ahead of whatever Brexit turns out to be.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief