Global| Oct 22 2019

Global| Oct 22 2019U.K. Industrial Trends Survey CBI- Implications for Brexit?

Summary

The Brexit process has been taking a toll on the performance of industrial orders in the United Kingdom. But the situation is only getting progressively worse and the worsening is becoming more extreme. Net orders fell to a -37 [...]

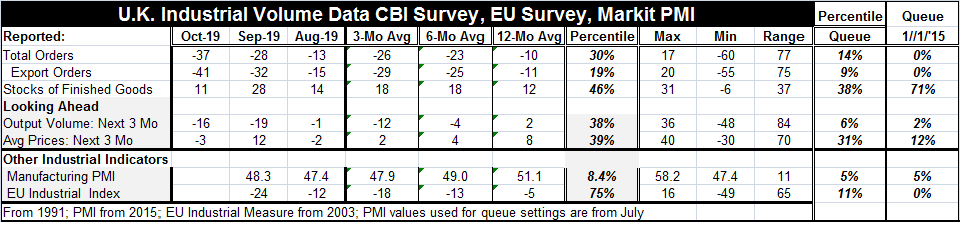

The Brexit process has been taking a toll on the performance of industrial orders in the United Kingdom. But the situation is only getting progressively worse and the worsening is becoming more extreme. Net orders fell to a -37 reading in October from an already weak -28 in September which itself was sharply weaker than the -13 reading in August. Export orders have followed that same progression lower.

The Brexit process has been taking a toll on the performance of industrial orders in the United Kingdom. But the situation is only getting progressively worse and the worsening is becoming more extreme. Net orders fell to a -37 reading in October from an already weak -28 in September which itself was sharply weaker than the -13 reading in August. Export orders have followed that same progression lower.

The percentile queue standings of the two series are also very similar. On data back to 1991, total orders have been weaker only 14% of the time and export orders have been weaker only 9% of the time. Ranked since 2015, each is on its low of the approximately last four and one half years.

Finished stocks of goods have been somewhat erratic, but they remain as a positive net balance (which means that inventories are still being built by more firms than are drawing them down). The October standing of 11 is in the 38th percentile of its recent queue of data; it is in its 71st percentile since January 2015. On balance, the inventory level ranks high relative to its historic values at least in comparison to the ranking of orders that is now so much weaker. Granted inventories, at a 38th percentile standing, are still below their long-term median value (which occurs at a ranking of 50%); but even the 38th percentile standing over the full cycle of data back to 1991 is high relative to orders at a 14th percentile standing and it speaks of an inventory imbalance.

The look ahead at output volume as expected over the next three months shows a reading of -16 which is not very upbeat, but it is an improvement from -19 in September. Both of those are sharp deteriorations from -1 in August. The 12- to six- to three-month averages have been steadily eroding. Expected output volume, however, has been weaker historically only 6% of the time. Since January 2015, it has been lower only 2% of the time. Clearly, the outlook is poor.

Prices are weak and their progression from 12- to six- to three-month averages also tracks a steady deterioration. This month the -3 reading is a drop from 12 in September and it represents only a slight weakening from the -2 reading in August. The three-month ahead outlook for prices has been weaker only 31% of the time since 1991 and it has been weaker only 12% of the time since January 2015. Clearly, the outlook for prices is weak. While the ECB is fighting deflation in Europe, the inflation situation in the U.K. has been a bit more equivocal. Still, U.K. firms do not think inflation will be an issue for the U.K. even as the end-game for Brexit beckons. So far, the pound sterling has been rising and that will tend to make the low-inflation bet work if sterling remains firm.

The bottom of the table has two slightly less timely readings from Markit and from the EU Commission. Both of these series are updated through September and both as of September show the ‘same sort' of weakness that the CBI survey shows as of October. Both of these aggregate barometers show very weak performance since 1991 and as weak or weaker performances in relative terms since January 2015.

On balance, Brexit remains an issue for U.K. firms. Even if a rock-hard Brexit is avoided, it looks as though a relatively hard Brexit jolt is in the works as the U.K. will be learning to compete with Europe from outside the protective tariff wall imposed by the EU (apparently everywhere but Ireland, anyway). The Brexit deal is not as Stevie Wonder might say ‘signed, sealed and delivered' but it is taking shape and it now seems that we can see what it offers. Still, surprises are not out of the question. Boris Johnson is still using his swagger, bravado and bombast to try to coax and bully votes for his vision which is still centered on an exit by Halloween. But that could be delayed. It could be much delayed. And there could yet be a nationwide election as Bo-Jo is threatening to call one if his program is not adopted quickly. And IF that happens, then there is also the possibility of another referendum vote on Brexit itself. To distort Shakespeare: “To Brexit or not to Brexit…is that still a question?”

If it's not broke...why Brexit?

As an American watching all this from afar, I must say I view it as something odd. (Not that any European should think that the shenanigans going on in the U.S. over impeachment are impeccably ordered and solemn or easy to understand). But Brexit is an important issue. It was ‘sold' to the electorate as something quite different than it is or will be. The very deal will create some sort of rift in the U.K. over the treatment of Northern Ireland which should be an old wound that no one wants to reopen. And since the original Brexit vote was so close, I have a hard time seeing it as a ‘clear mandate' as many assert. I think they do that as a political rhetorical device rather than out of conviction.

Why not try to clarify your mandate?

‘The people' have not really spoken. They have muttered and been flummoxed and stumbled to a close result on a referendum in which many were bamboozled by what we (in America) now call ‘fake news.' As far as I know, there was no Russian interference…Still, the idea should be that Brexit has been so well discussed in public and that many of the key issues have now been exposed to the light of day instead of having been swept into a lump under the rug and dressed up. Further, some of the Brexit dislocation already has been suffered. That should make it easier for U.K. citizens to make an informed choice. Given all the problems in getting a Brexit deal together and through parliament as well as agreed by the EU (a set of tasks not yet accomplished, by the way!), shouldn't the people be allowed to vote on it again? Doesn't that really make the most sense? How do you think the people in Northern Ireland (yes, a small number) would vote knowing what they know now? In fact, people could at the same time be polled for the KIND of departure they want (if they want one at all). This might not be reasonable at other times but now since parliament has not been able to agree to a set of acceptable conditions for months on end, why not ask THE PEOPLE what they want? Is that just too-obvious a question to a disinterested outsider to be understood by an insider with ‘skin in the game?'

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief