Global| Jun 22 2020

Global| Jun 22 2020U.K. Industrial Survey Shows Vague Hope

Summary

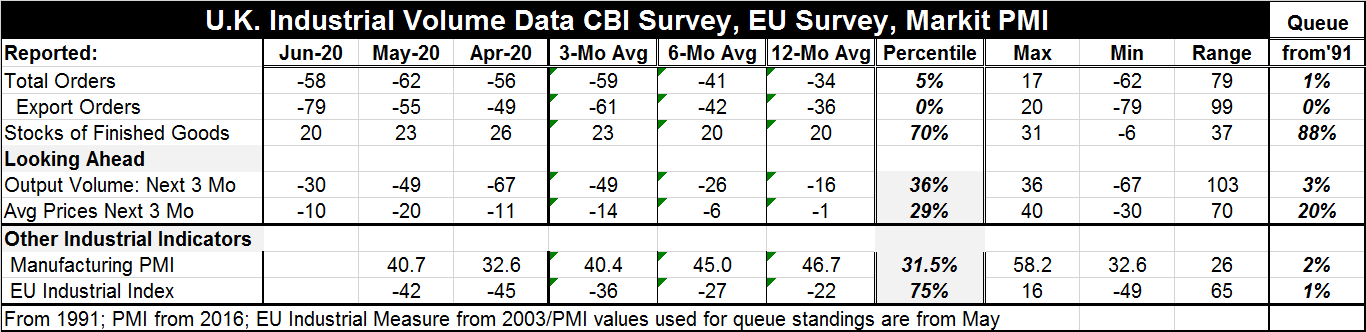

The U.K. CBI survey responses are still weak in June. Total orders are stronger than their May vales but slightly weaker than their April value. But export orders continue to fall and they are still falling hard. Export diffusion [...]

The U.K. CBI survey responses are still weak in June. Total orders are stronger than their May vales but slightly weaker than their April value. But export orders continue to fall and they are still falling hard. Export diffusion registered at -49 in April, fell to -55 in May and sits much lower at -79 in June. The June reading is the weakest on this timeline.

The U.K. CBI survey responses are still weak in June. Total orders are stronger than their May vales but slightly weaker than their April value. But export orders continue to fall and they are still falling hard. Export diffusion registered at -49 in April, fell to -55 in May and sits much lower at -79 in June. The June reading is the weakest on this timeline.

If there is some optimism in this report, it is in the forward-looking responses where the survey value improved in May and has improved again in June. Price expectations remain weak although they have lifted above their May value.

The month’s values show some reversal of fortune toward improvement except for export orders. However, the moving averages do not confirm an upturn since on that smoothed basis the turn is too fresh to register.

The queue percentile standings are uniformly low. For overall orders, the standing is in its bottom 1 percentile, rarely ever lower. As mentioned earlier, export orders are as weak as they have ever been on this timeline. Expected output volume in the next three months is numerically higher but is in its bottom 3 percentile. Expected prices are in their bottom 20th percentile. Breaking this pattern stocks are at their 88th percentile, a high standing that has pejorative ramifications since high inventories may mean that inventories are full - or overly full- and could be an impediment to new production.

The manufacturing PMI and the EU industrial index both are lagging metrics and both show a slight turn higher as of a month ago.

On balance, the U.K. manufacturing sector remains impaired. The readings are low and nothing is very reassuring. There is a numerical move higher that is a somewhat improved survey response, but in historic contract this improvement does not amount to much and amounts to nothing at all that is significant. There has been some increasing in the Baltic dry index despite the wakening in U.K. export orders. The Baltic index is a global trade barometer. If global trade really is improving, we would expect individual country measures to come along and improve as well. There is some hope for improvement globally, but not much of it stems from the new U.K. survey.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief