Global| Sep 25 2019

Global| Sep 25 2019U.K. Distributive Trade Survey Shows Mixed Weakness

Summary

There are two layers to the distributive trade retail and wholesale survey. The first is the report on both sectors for September; the second is the report for expectations in October. The September results for retail sales volumes: [...]

There are two layers to the distributive trade retail and wholesale survey. The first is the report on both sectors for September; the second is the report for expectations in October.

There are two layers to the distributive trade retail and wholesale survey. The first is the report on both sectors for September; the second is the report for expectations in October.

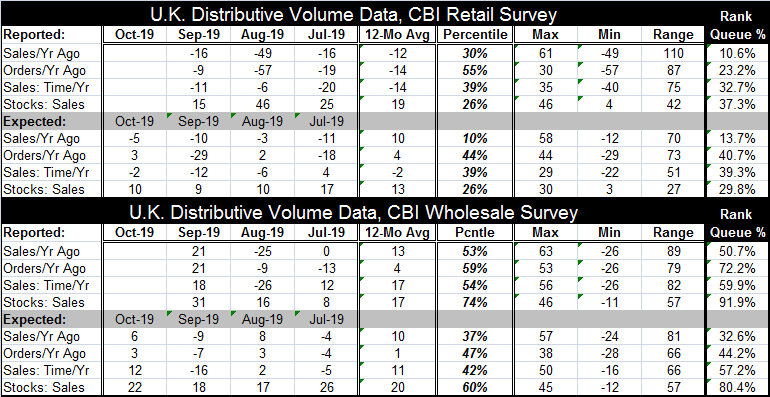

The September results for retail sales volumes: The report is still negative, but it is less draconian than its results were in August. The net sales reading vs. one year ago is at -16 in September instead of -49 in August. It is back to its level in July; the historic queue standing of the current value is in the bottom 10th percentile of all sales results since 1996. Retail orders also improved on the month to a still weak -9 from -57 and that reading has a low 23rd percentile standing. However, it is better than its 12-month average. Sales for 'time of year,' a seasonally adjusted concept, are worse at -11 down from -6 and at a 32.7 percentile standing, but again they are better than their 12-month average. Stocks, however, are lower at a 15 level in September down from 46 in August with a below median 37.3 percentile standing.

Contrarily, the September results for wholesaling volumes show outright improvements in the wholesale survey. Sparing the blow-by-blow details for wholesaling, sales, orders, and sales for 'time of year' all are improved from August and all have net positive readings. All the percentile standings for wholesaling are above their respective medians (values above 50%). However, the dark side for wholesaling is the strong (31 in September vs. 16 in August) rise in inventories and the 91.9 percentile standing of this reading. Wholesaling seems to have developed some excess inventories in September.

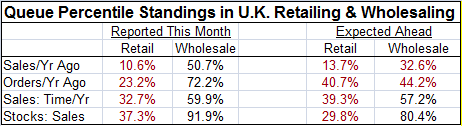

Looking to October and setting stocks aside for retailing and wholesaling, most queue standings are below their respective medians. Retailing has weaker readings than wholesaling. As to stocks, wholesaling once again reports out a high stock reading while retailing posts a positive stock reading but one with a low queue standing. All the wholesale outlook values are net positives and except for sales compared to one year ago; all wholesale readings surpass their 12-month averages. Retailing's October outlook shows negative readings for sales compared to a year ago and a negative for sales by 'time of year' and all reading are below their 12-month averages except for sales by time of year where the reading stands at its 12-month average.

Since wholesaling feeds the retail sector, it seems strange for wholesaling to be doing better as retailing struggles. But wholesalers have always been more optimistic on sales for time of year than retailers. For example, since 2013 retailers assessment of sales for time of year has averaged -1 while wholesalers have averaged a reading of 27. But the queue standing calculations are not affected by such things and they continue to show a more upbeat wholesale sales sector in September as well as for the outlook. However, wholesalers have what seems to be a developing inventory problem that could bring the two series assessments closer together. It may also be that wholesalers have simply stockpiled goods in anticipation of some Brexit transition problems. For now I would be negative on retailing and guarded on the outlook for wholesaling. And of course, there is always the risk of unexpected damage from a bad Brexit deal.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief