Global| Jul 27 2009

Global| Jul 27 2009Tight Money Isn’t Funny: EMU Money Growth Continues To Decelerate

Summary

BANKS, MONEY, CREDIT- A number of reports are in the news today about banking sector issues in lending. With the EMU money and credit measures just out it’s an appropriate time to survey the background for lending. The German Zew [...]

BANKS,

MONEY, CREDIT- A number of reports are in the news today

about banking sector issues in lending. With the EMU money and credit

measures just out it’s an appropriate time to survey the background for

lending. The German Zew survey of lending institutions in Germany finds

that larger companies are having the harder time getting credit. Mutual

and cooperative style banks in Germany have been feeding credit more

easily to smaller institutions there.

BANKS,

MONEY, CREDIT- A number of reports are in the news today

about banking sector issues in lending. With the EMU money and credit

measures just out it’s an appropriate time to survey the background for

lending. The German Zew survey of lending institutions in Germany finds

that larger companies are having the harder time getting credit. Mutual

and cooperative style banks in Germany have been feeding credit more

easily to smaller institutions there.

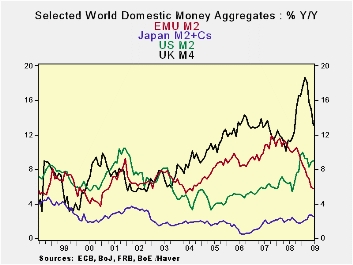

Outside EMU liquidity is expanding - The table and charts at the top of this presentation reveal several the trends. While UK money supply has boomed and busted, its rate of monetary expansion remains the highest among this group of countries and is still barely below its previous recent peak pace in 2006. The US M2 pace spurted in 2008 and has since been locked in an erratic declining growth rate phase. Japan’s money growth hit its low point in 2006 and has since been in a very gradual accelerating trend that recently seems to have flattened out its growth. Japan is still the weakest trend, however.

Special circumstances- In the UK there is a push on to funnel credit to smaller businesses and that seems to be working. In Japan there may be demand side pressures at work as the corporate services price index fell sharply hinting at another round of deflation in Japan. If that takes hold lending in Japan will suffer but mostly from demand side weakness.

ECB is tighter: Europe shows money supply growth peaking in later 2007/early 2008 then steadily decelerating. This is for a period when the rest of the countries were pushing out liquidity at a faster pace. Despite its rate cuts, ECB liquidity in the hands of the public has been consistently squeezed. Europe has its lowest money supply growth since 2004, but it was last persistently weaker than this back in 2001. Despite all its rhetoric about easing and easy money, the ECB has been tightening its monetary grip in quantity terms.

Various horizons: The sequential growth rates for money supply and for credit (in EMU) in the table above make the point. Only EMU has one year money and credit growth so much weaker than the annual rates over two years and three years. For the US, UK and Japan over the recent one year money growth is stronger compared to those earlier horizons. But over six months and three months the US and the UK are seeing weaker money growth than over the longer the periods as is EMU (same goes for credit in EMU). Only Japan is showing stronger money growth more recently.

Real balances: Real balances turn the tables on many of these trends. In terms of real balances Europe’s growth in money is as strong - or stronger - than in the US and the UK over the less than one year horizons. Japan’s growth is the strongest of all over three-and –six months. But the better growth in real balances in Europe is not having the desired impact on credit as residential ‘real’ credit growth has slowed to a crawl while overall loan growth is shrinking in real terms.

Risks still loom: Despite the fact that some lending spreads are back to more of a normal configuration the banking sector is having lingering troubles. We know that housing credit issues like foreclosures usually lag the cycle. Traditionally banks are still involved in dealing with credit hangovers even as the economy improves. But in this instance the degree of economic and credit improvement is not even in train. We are talking about less weakness and better economic signals not of economic growth- at least not yet. While there are some signs of economic and financial stabilization the credit quality and lending scene has continued to deteriorate. So even as we get more optimistic over the results of recent economic indictors we must remain cognizant- as the central banks do – that the banking sector is still in the midst of its big chill. Financial stocks may have recovered from their deathbed valuations and a few banks may have posted large corporate earnings for a quarter, but for the sector at large, substantial risks still loom and some cases the adverse pressures are getting worse.

| Look at Global and Euro Liquidity Trends | |||||||

|---|---|---|---|---|---|---|---|

| Saar-all | Euro Measures (E13): Money & Credit | G-10 Major Markets: Money | Memo | ||||

| €€-Supply M2 | Credit: Resid | Loans | $US M2 | ££UK M4 | ¥¥Jpn M2+Cds | OIL:WTI | |

| 3-MO | 2.9% | 1.0% | 0.0% | 1.7% | -3.7% | 3.3% | 355.2% |

| 6-MO | 2.9% | 1.2% | 0.4% | 5.4% | 6.1% | 3.7% | 162.7% |

| 12-MO | 5.8% | 4.1% | 1.8% | 9.0% | 13.1% | 2.5% | -47.7% |

| 2Yr | 8.1% | 7.7% | 5.8% | 7.6% | 12.3% | 2.3% | 1.8% |

| 3Yr | 8.7% | 8.9% | 7.4% | 7.0% | 12.5% | 2.1% | -0.6% |

| Real Balances: deflated by Own CPI. Oil deflated by US CPI | |||||||

| 3-MO | 2.0% | 0.2% | -0.9% | -1.6% | -5.8% | 5.4% | 340.6% |

| 6-MO | 2.5% | 0.9% | 0.1% | 2.6% | 3.7% | 5.4% | 155.7% |

| 12-MO | 5.9% | 4.2% | 2.0% | 10.3% | 11.1% | 4.1% | -47.1% |

| 2Yr | 6.1% | 5.7% | 3.8% | 5.8% | 9.2% | 2.1% | 0.1% |

| 3Yr | 6.7% | 6.9% | 5.4% | 4.9% | 9.5% | 2.1% | -2.6% |

| Japan CPI for June is an estimate; it uses the May value to produce the real balance figure. | |||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief