Global| Oct 20 2016

Global| Oct 20 2016The German PPI Is Restless...for Good Reason

Summary

The German PPI has been on the move up. But a funny thing happened in September on that journey; the PPI backtracked and fell. This setback has also blunted the pace of the PPI rise and even the path of the ex-energy PPI. That gauge [...]

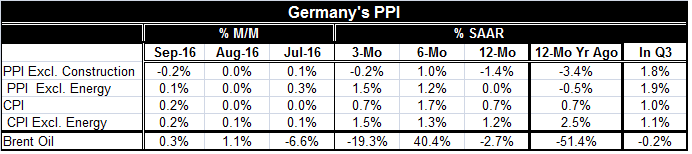

The German PPI has been on the move up. But a funny thing happened in September on that journey; the PPI backtracked and fell. This setback has also blunted the pace of the PPI rise and even the path of the ex-energy PPI. That gauge had surpassed a 2% per year pace over three-months and now is back below that threshold. Still, oil prices are rising and more PPI pressure in the months ahead is probably the safer bet than looking for declines. But the outlook for oil prices as well as inflation remains clouded by any number of complex, interlocking and mutually inconsistent factors. Let's take a look.

The German PPI has been on the move up. But a funny thing happened in September on that journey; the PPI backtracked and fell. This setback has also blunted the pace of the PPI rise and even the path of the ex-energy PPI. That gauge had surpassed a 2% per year pace over three-months and now is back below that threshold. Still, oil prices are rising and more PPI pressure in the months ahead is probably the safer bet than looking for declines. But the outlook for oil prices as well as inflation remains clouded by any number of complex, interlocking and mutually inconsistent factors. Let's take a look.

The OPEC deal and Middle East tensions

Oil is a very important variable to the outlook for the PPI. OPEC's output restricting deal including importantly OPEC, Russia and the behavior of Iran will all continue to be important ingredients in obtaining the path for oil prices that OPEC seeks. The current chaos in Mosul and ongoing conflict in Syria continue to muddy the waters of cooperation where various participants in the Middle East conflict are at odds with one another in various ways despite trying to forge and agreement on oil to boost oil prices, a common goal.

OPEC and friends?

One enhancement to cooperation is the recently concluded Saudi bond float which raised a whopping $17.5 billion for the Kingdom and certainly will help to buy it time as it tries to re-gear its economy to the new realities in the oil market as well as to influence those realities. Oil producers from Russia to Saudi Arabia have been making changes in their economies to reflect the new lower oil-price realities. Iran conversely is still looking to boost its output as sanctions have been dropped and it is now trying to recoup production capabilities that had been allowed to slip.

Oil and the PPI

Oil is import to the PPI where it bears a relatively large weight. And oil has the ability to influence other prices as well. But in recent years the knock-on effects from oil have been blunted substantially. Still, the German data show that the PPI excluding energy is accelerating and the ex-energy measure is on the verge of making its first year-on-year gain since 2013.

The PPI and the CPI

The PPI and the CPI

The chart shows the year-on-year ex-energy PPI vs. the ex-energy CPI. The CPI (formally the EU HICP gauge) is what the ECB will be looking at on an EMU-wide basis to judge its policy effectiveness. But here we show the two national measures for Germany. It is clear that the PPI is much more volatile than the CPI. While the PPI's relatively wilder swings seem to influence the path of the CPI, that influence is mild and occurs with a lag.

Oil watching

We have been through numerous episodes of oil-price-watching in the past since OPEC was formed. The one thing we do know about oil is how unpredictable it can be. Prices can spurt and then they can reverse and plunge. They can rise and sit on a high plateau for a long time then suddenly erode. The expression in the oil industry is that the 'cure for high oil prices is high oil prices' and the same is true for low oil prices. That pithy expression works, because the demand for oil and oil products is relatively inelastic in the short run. When prices shift demand does not change at first. But given time, demand becomes more elastic. Consumers eventually can and do take steps to deal with higher or lower oil prices and those steps eventually affect demand and that eventually gets back to affect the oil prices. Such progressions usually take time.

New technologies affect the oil output balancing act

The new ingredient in oil is the alternative technologies being used in the U.S. to develop new and formerly beyond-reach oil reserves. As these reserves are tapped, the normal upward pressures on oil prices from global demand growth are undercut. Right now global demand is weak, another factor keeping oil prices off balance and making it harder for OPEC 'and friends' to cut and to stick to a deal. Moreover, the higher that oil prices get in this situation, the more new supply will be coming from the U.S. Higher prices will now cut with two edges instead of just one. That reality will require a finer balancing act by OPEC to control prices.

Oil prices are 'not really' inflationary...but

Oil also is only a short-term factor for inflation. It can make inflation LOOK LIKE it is rising when it is only producing a relative price effect for an important price level component. But right now central banks around the world are doing all they can to conjure higher prices (inflation). The Bank of Japan is swimming against the strong current of declining population trends to try to gain upward price pressures and to restore a normal-functioning economy. The ECB has been below its price objective for far too long; its credibility has been damaged. Europe is under pressure on several fronts. It needs to show some progress.

Economic stress breeds discontent

Along with its inflation miss, growth in the EMU has been subpar and bad enough that anti-austerity movements in several countries have gained a great deal of traction. This has been exacerbated by events in the Middle East and the influx of migrants. The way the EU has instructed its members to deal with them has not been in line with all nations' policies and has created even more friction. Europe is aware that the underlying malaise that bought about Brexit exists beyond the borders of the U.K. and that a number of current EU and EMU nations have substantial factions that are unhappy with how they are treated by the EU or by the EMU process.

Inflation as a sign of progress?

Inflation may not be a panacea, but it is now the hot topic. Even getting some oil-induced not-lasting headline inflation could help to take some policy pressure off Europe and the ECB. The ECB desperately needs a victory. Of course, depending on how the oil price effect develops, it could also engender new challenges. The Germans will be quick to want a policy turnaround of inflation normalizes at all.

Oil and the PPI: worth watching

For all these reasons, oil and the PPI are important things to watch in the coming weeks and months. They may not either be targeted policy variables, but they will have some impact on things that matter to policymakers. As explained above, oil also ties together some important economic and geopolitical themes involving strange bedfellows. So far, geopolitics have not bled over into the economic sphere (beyond the sanctions placed on Russia for its seizure of Crimea), but that does not mean it can't or won't happen. With pressure and tensions rising in the EMU, presidential elections on tap in the U.S., and weak growth lingering everywhere as trade deals fizzle, the PPI and oil will be two of the more important 'games in town.'

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief