Global| Oct 18 2019

Global| Oct 18 2019The EMU Current Account Surplus Expands

Summary

The EMU current account expanded to 26.6 billion euros in August from 21.6 billion euros in July. The trade surplus expanded, the balance on manufacturing trade moved to a larger surplus and the balance on nonmanufacturing trade also [...]

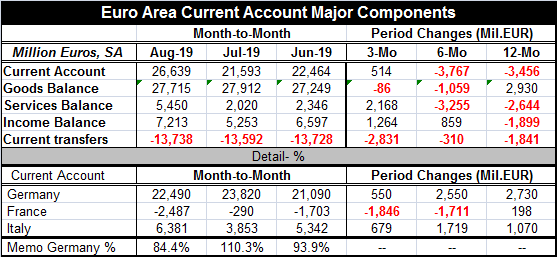

The EMU current account expanded to 26.6 billion euros in August from 21.6 billion euros in July. The trade surplus expanded, the balance on manufacturing trade moved to a larger surplus and the balance on nonmanufacturing trade also produced a larger surplus. The improvement was more or less across the board.

The EMU current account expanded to 26.6 billion euros in August from 21.6 billion euros in July. The trade surplus expanded, the balance on manufacturing trade moved to a larger surplus and the balance on nonmanufacturing trade also produced a larger surplus. The improvement was more or less across the board.

The balance on services also moved to a large surplus, jumping to 5.45 billion euros in August from 2.0 billion euros in July. The balance on income rose to 7.2 billion euros in August from 5.25 billion euros in July. The balance on current transfers, a persistent outflow item, logged a larger outflow at -13.7 billion euros in August from -13.6 billion euros in July. Over 12 months all the accounts have moved to show a larger deficit or smaller surplus with the exception of the trade account where the surplus has risen by nearly 3.0 billion euros over 12 months. The German, French and Italian current account surpluses each increased over 12 months.

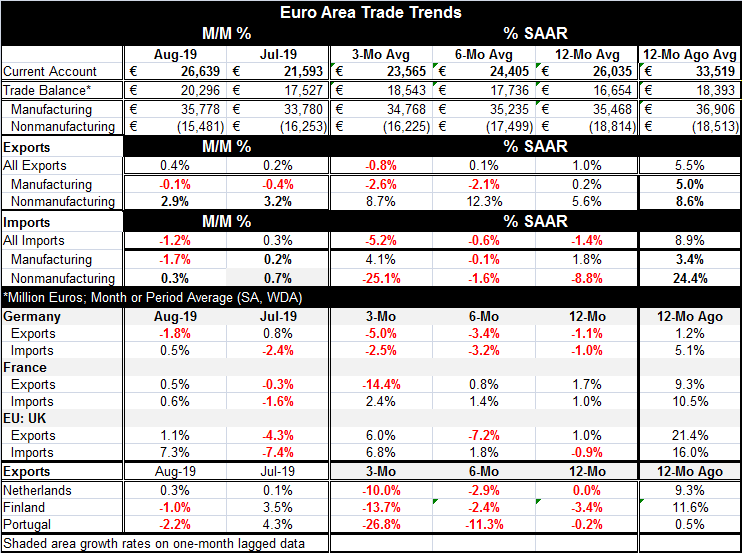

Overall EMU exports are weak and decelerating. They bumped up by small amounts in each of the last two months but grow by only 1% over 12 months, at a razor-thin thin 0.1% over six months then fall at a 0.8% annualized rate over three months. Overall imports decline on all three horizons and fall faster at a -5.2% pace over three months than they do (-1.4%) over 12 months, but there is no sequential pattern yet; there is persistent import deterioration. Still, the overall export and import patterns both are consistent with deterioration and faster drop in imports is generating a larger trade and current account surplus.

Breaking this down between manufactured and nonmanufactured goods complicates the story to some extent. Manufactured exports show persistent and sequential weakness with outright decline logged over six months and three months. Manufactured imports show a larger gain than exports over 12 months (1.8% vs. 0.2%) then imports edge lower over six months and spring back to grow at a 4.1% pace over three months.

The nonmanufacturing flows that encompass commodities (and especially energy) where prices can be much more volatile show exports growing at a positive pace over all horizons with no clear sequential pattern but with three-month growth higher than 12-month growth. For imports, nonmanufacturing flows show decline on all horizons without a sequential pattern but with much more weakness over three months than over 12 months. This is the opposite ‘tendency’ than for exports.

For nonmanufacturing tendencies are the opposite from the nonmanufacturing tendencies and that is true for both exports and imports. And for exports and imports, the tendencies are reversed with manufacturing exports tending to weakness and with manufacturing imports tending to strength.

For these reasons, it is not possible to sort out the final direction of EMU trade flows. There is still a lot in flux. Despite weaker conditions in the EMU, the manufacturing flows which we would like to think of as the more fundamental and less fickle flows show that imports are still firming. That flies in the face of trends for weaker domestic conditions. Why is domestic demand (for imports) firming? Meanwhile, exports are weakening in line with ongoing concerns about weaker global growth. German exports, French exports, Dutch exports, Finish exports and Portuguese exports all show tendencies to weakness on growth rates from 12- to three-months. Only the U.K., which is under a different currency regime, shows some three-month strength in exports.

China today reported out its weakest GDP result since 1992 as growth came in a 6%. This was a bit slower than expected. While the United and China are still negotiating and may have the basis for a first step of an agreement in the making, nothing is done on that bilateral stage until there is a signed document; the two-sides have been reported as close or as having a deal in the past, a deal that proved elusive.

This month the EMU trade and current account trends are particularly baffling and strike the most adversarial cross currents possible. We expect both flows, exports and imports, to slip into a weakening mode as global growth is headed that way and as the European bloc does not appear to be bucking that trend. There are still some shocks possible from Brexit, but the Brexit situation is looking like it is closer to a deal. But even there, there is no deal until there is a signed deal and that is going to depend on the U.K. parliament that has shot down so many Brexit deals in the past it must be due for a new ‘hunting license.’ Does it matter that this time Boris Johnson is on the side trying to get the deal approved? We’ll see.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief