Global| Mar 26 2014

Global| Mar 26 2014The Con Game: Confidence Flattens at High Level in Germany; What about Elsewhere?

Summary

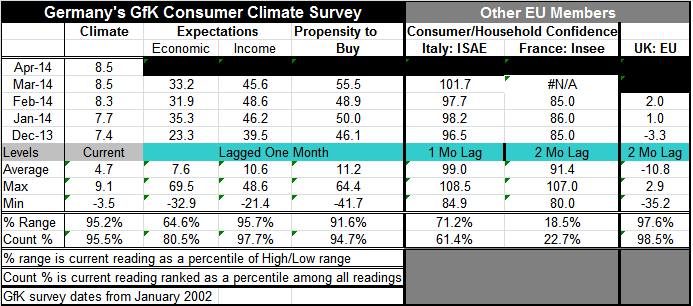

German economic climate for April in the GfK format has stalled out or paused at a relatively high value. Climate in Germany gets better than this less than 5% of the time. That makes this level an impressive standing. Economic [...]

German economic climate for April in the GfK format has stalled out or paused at a relatively high value. Climate in Germany gets better than this less than 5% of the time. That makes this level an impressive standing.

German economic climate for April in the GfK format has stalled out or paused at a relatively high value. Climate in Germany gets better than this less than 5% of the time. That makes this level an impressive standing.

Economic conditions lag by one month. While climate has been moving higher in juggernaut-fashion, expectations for economic conditions have been oscillating for several months. The current economic reading stands in the 80.5th percentile of its historic ranking which tells us it has been higher only about 20% of the time. The expectations reading for the economy is strong but is not as strong as the climate reading.

However, stronger than climate and stronger than the economy reading has been the expectation for income. Like economic expectations, the expectation for income has prevaricated over the past several months. Its current index stands high in the 97th percentile, but still off its cycle peak. This reading is stronger that its current level less than 3% of the time. Its strength is exceptional, but its trend is now less certain.

Also strong is the German propensity to buy. That index stands in the 94.7th percentile of its historic queue and is higher only about 5% of the time. Unlike income and economic expectations, the propensity to buy index is still surging to new heights after a one-month stumble in January.

GfK uses surveys to make these assessments and currently is looking for a still-strong reading in April as documented above. The GfK framework does not seem to have found a significant back tracking in its survey despite the situation in Ukraine.

Germany continues to greatly outpace other EMU members on the subject of confidence (and in many other areas as well). However, the UK, an EU member country whose data lag by two months, actually posts a confidence figure that surpasses the GfK climate reading in April. The UK reading for February stands in the 98.5th percentile of its historic queue, surpassing the German climate reading.

Moving to the two next largest economies in the EMU, France and Italy, we find the Italian measure in the 61st percentile of its historic queue while the French indicator of confidence is in the bottom quarter of its range in the 22nd percentile.

The French measure for February had a setback even at this low level. Contrarily, Italy's confidence spurted in February, rising from 97.7 to 101.7 to post its still-modest reading for February.

These metrics uncover old themes for the Monetary Union. Germany is leading the way ahead and has lapped its competition. Italy's strong rise in confidence reminds us that the rest of the Community is largely improving too, but improving to much more modest levels. France reminds us that there are `haves' and `have-nots' as its weak standing and failure to improve at even this low level of confidence is both vexing and disturbing. France fared better this month in terms of its PMI gauges which each crossed over the neutral line to register sector expansion. For its part, the UK is the stunning success story among countries that have stayed in the EU but out of the common currency arrangement. But the UK's success is unique.

This report is another in a series that acknowledges success in Germany and finds that German success has not bailed out the euro-Zone. We expect this theme will begin rub some of the edges raw once Europe has made a `fuller recovery' and finds that huge differences in member economic circumstances remain. The `progress' and `improvement' in living standards made by many peripheral Zone-member nations as the Zone was first formed were made on borrowed time and borrowed money and were not on firm footing. The anguish suffered in the financial crisis has not restored their lost competiveness to what it was when they joined the Zone. In short their hardest work still lies ahead. If peripheral countries think that they are going back to those times of the early Zone, they will be greatly and persistently disappointed.

For now we can talk of an uneven recovery or of Germany leading Europe out of the woods. But is it really leading it out of the frying pan into the fire? What will the peripheral nations of EMU do when it becomes clearer that they are not going to be pulled along much farther into a period of normalcy but that their restoration of normalcy is going to involve much more pain to restore the competitiveness gap they have opened with Germany and others since the single currency was launched? That is the real question for Europe. Some think Europe's future was burnished in the fires of the economic crisis from which it emerged in one piece. But while that was a very public media spectacle the second phase will be less headline making and more heartbreaking. This is the real difficult phase and euro area unity will be challenged by it in the years ahead.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.