Global| May 05 2014

Global| May 05 2014Sweden Struggles

Summary

Industrial production (excluding construction) in Sweden fell by 3.8% in March with manufacturing production falling by 3.9%. Each of those drops follows a rise about 2% in February, but in each case those increases were preceded by a [...]

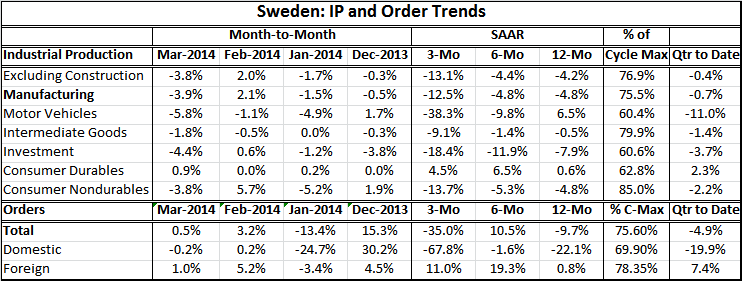

Industrial production (excluding construction) in Sweden fell by 3.8% in March with manufacturing production falling by 3.9%. Each of those drops follows a rise about 2% in February, but in each case those increases were preceded by a substantial drop in January. As a result, manufacturing and industrial production ex-construction are falling at rates of 12% to 13% over three months in addition to dropping by rates of 4.5% to 5% over six month and by rates of 4% to 5% over 12 months.

Industrial production (excluding construction) in Sweden fell by 3.8% in March with manufacturing production falling by 3.9%. Each of those drops follows a rise about 2% in February, but in each case those increases were preceded by a substantial drop in January. As a result, manufacturing and industrial production ex-construction are falling at rates of 12% to 13% over three months in addition to dropping by rates of 4.5% to 5% over six month and by rates of 4% to 5% over 12 months.

Motor vehicle production dropped sharply in each of the last three months and is plunging at a 38% annual rate over three months. Intermediate goods production is becoming increasingly weak with a 9.1% decline at an annual rate over three months, a 1.4% rate of decline over six months, and a 0.5% rate of decline over 12 months. Investment demand is falling hard with an 18.4% annual rate of decline over three months, a nearly 12% rate of decline over six months and a nearly 8% annual rate of decline over 12 months. Consumer durables buck the trends with a positive growth rate of 4.5% over three months, 6.5% over six months and 0.6% over 12 months. Consumer nondurables falls into the declining pattern with the drop in output of a 13.7% annual rate over three months, 5.3% over six months and 4.8% over 12 months. This is an extremely weak matrix of growth rates. Growth is weak in just about all categories and declining at a steady pace over most of the horizons as well with only consumer durables as an exception.

In addition, the forward-looking order series shows more bad news. Overall orders rose in two of the last three months. They are still declining at a 35% annual rate over three months; they rose at a 10.5% rate over six months but also are down at a 9.7% pace over 12 months. The problems stem chiefly from domestic orders that fell in March after a small rise in February and a huge decline in January.

Domestic orders are falling at a 67% annual rate over three months, then dropping at 1.6% annual rate over six months and a 22% annual rate over 12 months. As you can see in the chart, there has been a recent outsized drop in orders; there has been a history of one-time spikes in this series. January was one of these periodic spikes. Nonetheless, what the chart shows is a broader pattern of domestic orders being weak and on a weakening trend until just very recently when there was some hint that domestic order might be stabilizing. The outsized drop in these orders in January changed that. Now it's hard to tell what the trend will be in the coming months.

Foreign orders are doing better. There was a 1% gain in March and a rise of 5.2% in February after a 3.4% drop in January. As a result, foreign orders are climbing at an 11% annual rate over three months and a 19% annual rate over six months. Over 12 months they are increasing by only 0.8%.

Sweden's recovery continues to be weak. The industrial production index excluding construction is still only about 77% of its last cycle peak. Manufacturing is about 25% short of its last cycle peak. Motor vehicles output is 40% short of its past cycle peak. Consumer nondurables output is the strongest sector in this regard, being only 15% short of its past cycle peak. Consumer durables are still about 37% short of their past cycle peak. Total orders are about 25% short of their past cycle peak with domestic orders 31% shy and foreign orders only 22% shy.

Cast in terms of quarterly growth rates, the weakness in industrial production seems less. Since these are data for March, the current report completes the first quarter. In the first quarter on these data, industrial production excluding construction is falling by just a 0.4% annual rate with manufacturing production down at a 0.7% annual rate. Motor vehicle production is off at an 11% annual rate; intermediate goods are off at just a 1.4% annual rate. Investment output is off at a 3.7% annual rate with consumer durable goods production up at a 2.3% pace. Nondurables output is down at 2.2% pace. The picture for orders is still pretty grim with total orders down at a nearly 5% annual rate in the quarter and domestic orders down at a nearly 20% annual rate. Foreign orders are up at a 7.4% annual rate.

The January outsized drop in domestic orders makes the trend hard to pin down; January simply dominates all other months. However, the bulk of the trends Swedish industrial production and orders are substantially negative. The one bright spot is in foreign orders which seem to show some life. Sweden may find its economy's help but the context of the growth in the countries around it. However, the domestic economy in Sweden still seems to be struggling. Industrial production is weak across the board with the exception of consumer durables. That will not be enough to drive growth; it will need help.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief