Global| May 27 2004

Global| May 27 2004Steadying GDP Trends in Brazil, Philippines; Investment Grows

Summary

US financial markets are on alert during the middle of the first month of each quarter as companies report profits, a period that investors and traders refer to informally as "earnings season". Similarly, the second half of the middle [...]

US financial markets are on alert during the middle of the first month of each quarter as companies report profits, a period that investors and traders refer to informally as "earnings season". Similarly, the second half of the middle month of each quarter could be dubbed "GDP season", as country after country publishes its prior quarter growth performance.

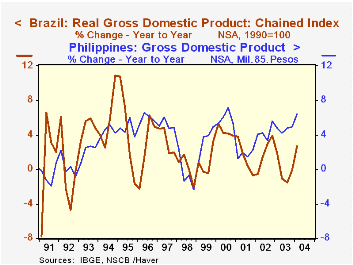

Today, Brazil and the Philippines released their first quarter results. Brazil's growth edged higher, to 1.6% quarter-on-quarter from 1.4% in the final period of 2003. This lifted the year-on-year rate to 2.7% after three quarters of contraction. Notably, as with the UK and Spain's data discussed here yesterday, investment is playing a roll in the improving trend in demand in Brazil. Investment growth was slower in Q1, at 2.3% compared with Q4's 4.0%. But these two gains, plus a similar one in the prior period, mark a distinct turnaround from a previous stretch of outright declines. Over longer periods, such as two and four years, overall growth in Brazil seems to be settling into a pace around 2%, not as high as some years, but less volatile.

Growth in the Philippines, by contrast, has been fairly steady over the last couple of years at rates higher than 5%. Even in the recession-plagued year of 2001, Philippine GDP did not contract year-over-year, and moreover, during the Asian crisis in 1997-98 there was only a modest and brief reduction in economic activity. Steady growth in the consumer sector, which constitutes about three-quarters of the Philippine economy (more than in many countries), is a source of stability. In the latest quarter, total GDP growth was 1.9%, down from Q4's 2.5%; however, the Q1 rate is hardly "low", and it included a firming of private consumption from 1.5% to 1.6%. Investment is more erratic here than elsewhere, and it rose 7.1% in Q1 after falling 2.9% in Q4.

The gains in investment in many varied countries, which have been evident in most of the recently issued Q1 reports, suggest that low world interest rates are helping support world economic activity.

| GDP & Select Components, % Changes | Qtr/Qtr (Seasonally Adjusted)Year/ Year | 4th Qtr/4th Qtr||||||

|---|---|---|---|---|---|---|---|

| 1st Qtr 2004 |

4th Qtr 2003 | 3rd Qtr 2003 | 2003 | 2002 | 2001 | ||

| Brazil - Chain Index, 1990=100 | 1.6 | 1.4 | 0.5 | 2.7 | -0.1 | 3.9 | -0.7 |

| - Investment | 2.3 | 4.0 | 3.2 | 2.2 | -5.0 | 4.1 | -8.2 |

| Philippines - 1985 Pesos | 1.9 | 2.5 | 1.1 | 6.4 | 5.0 | 5.6 | 2.3 |

| - Fixed Capital Formation | 7.1 | -2.9 | 1.6 | 4.8 | 1.2 | 5.8 | -15.5 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief